Warsh Confirmed, Bonds Break 5.1%, and the Consumer Earnings Countdown Begins

The AI-driven equity euphoria that carried Nasdaq to new highs now faces a stagflationary reckoning as real wages turn negative for the first time in three years.

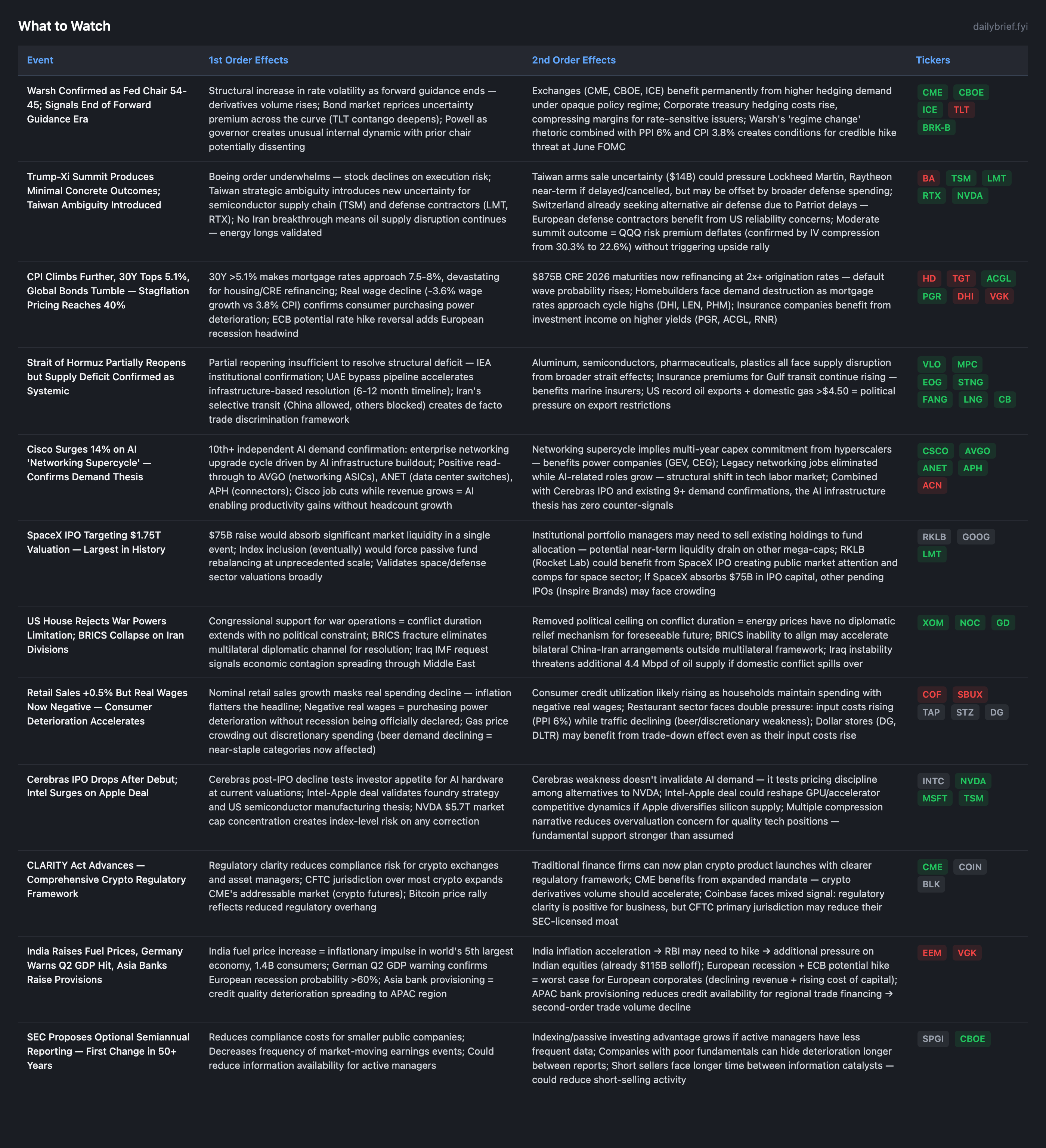

The week’s critical shift: Warsh is confirmed, Trump-Xi produced a dud, and the bond market is now pricing the Fed as behind the curve. The 30Y yield topped 5.1%, PPI printed 6% YoY, real wages turned negative for the first time in three years, and global bonds sold off sharply — while S&P 500 and Nasdaq hit new all-time highs on Cisco’s AI supercycle earnings before reversing Friday. The equity market’s AI-driven euphoria is now directly colliding with a stagflationary data regime.

The prior brief’s assessment that “SPY contango means the mechanical equity bid absorbs all shocks” lasted exactly one trading day. Friday’s selloff suggests the absorption capacity has limits when (a) the Trump-Xi summit fails to deliver Iran resolution, (b) Warsh confirmation introduces monetary policy uncertainty, and (c) 30Y >5.1% begins repricing equity duration. The world model’s “moderate outcome” probability for the summit (60-70%) was correct, but the market had priced more optimism than warranted.

Three prior brief assessments require updating: (1) credit repricing timeline extended again — HYG OI P/C declined to 4.09, further unwinding from the May 12 spike, and spreads remain at 2.82%; (2) QQQ IV compressed from 30.3% to 22.6%, confirming the summit premium is dissipating; (3) the consumer May 19-21 catalyst window is now 2-4 trading days away and every incremental data point (real wages negative, beer demand declining, gas >$4.50) strengthens the bearish configuration.

Warsh Confirmed: The Communication Regime Change Begins

Warsh’s confirmation (54-45) and FT reporting on his “keep quiet” communication philosophy represent the most important structural market regime change since the pandemic-era forward guidance expansion. His stated belief that “incantations do more harm than good” signals the end of dot plots, constant speechifying, and real-time guidance updates that market participants have used to reduce rate uncertainty.

The mechanism: less Fed communication → wider confidence intervals around policy path → larger moves on actual FOMC decisions → higher implied vol across rates complex → more hedging demand → more exchange volume. This is a permanent structural shift effective from his first FOMC (June 16-17).

Miran’s resignation creates an additional Board vacancy. With Warsh’s hawkish lean, the composition of future FOMC voters matters more. Collins’ explicit rate hike endorsement (from the prior brief) now has an institutional ally at the top.

Combined with the bond market pricing the Fed as behind the curve on inflation (CNBC), the first substantive Warsh action will carry outsized impact. If he signals openness to hiking — consistent with PPI 6%, CPI 3.8%, and his own hawkish reputation — the 2Y could move from 3.98% toward 4.25-4.50% rapidly. TLT’s persistent contango (10.9% near vs 14.3% at 12-month) prices this escalating uncertainty.

Trump-Xi Summit: Disappointing Moderate Outcome with Taiwan Tail Risk

The summit landed in our 60-70% probability bucket (moderate/photo-op), but with two unexpected wrinkles. First, Boeing’s 200-jet order that the market initially cheered was subsequently characterized as disappointing — stock fell. Second, Trump’s “I don’t talk about” Taiwan defense comment introduces strategic ambiguity that the market hasn’t fully processed.

The Taiwan comment matters for three reasons: (1) it potentially undermines the deterrence framework that has kept Taiwan Strait stable; (2) it puts a $14B arms sale into question (FT confirms Trump “undecided”); (3) it creates a new tail risk for TSM specifically and the semiconductor supply chain broadly. This doesn’t change established BUY theses on defense or semiconductors but adds a monitoring requirement on any further Taiwan rhetoric degradation.

On Iran, the summit produced only diplomatic pleasantries: China “wants Hormuz open,” Treasury Secretary Bessent “indicated China will help reopen the strait.” Per our analyst lessons (reinforced 12 times): discount vague diplomatic signals without operational specifics. China’s desire for open Hormuz is obvious from first principles — they import the most oil through it. A statement of desire without an enforcement mechanism is noise.

Trump threatening sanctions on Chinese companies buying Iranian oil is the single actionable development. If implemented, this would further constrain global oil supply and push crude higher while simultaneously creating US-China friction that contradicts the summit’s conciliatory optics.

Friday’s Market Reversal: AI Euphoria Meets Bond Market Reality

The sequence matters: Thursday, Cisco surged 14% and Nasdaq hit new ATH on AI supercycle narrative. Friday, equities reversed sharply as yields jumped and inflation data accumulated. This “rally on AI, sell on macro” pattern confirms the bifurcation thesis but also shows its limits. When yields rise fast enough (30Y >5.1%), even AI stocks face duration repricing.

The 40% stagflation probability priced by traders (CNBC) is a new quantitative reference point. Combined with the Kalshi market pricing 34% probability of a Fed rate hike by December 2026 (which aligns with our 30-40% estimate from prior briefs), the market’s macro pricing now converges with our framework.

Bessent’s “Substantial Disinflation Ahead” — Conflicting Signal

Treasury Secretary Bessent predicting energy-driven inflation will reverse contradicts the data environment (PPI 6%, CPI 3.8%, IEA structural deficit, refining output decline). This is either: (a) political messaging to manage expectations ahead of midterms, (b) based on private intelligence about imminent conflict resolution we can’t verify, or (c) genuinely delusional about the inflation pipeline. Given our analyst lesson on weighting source tiers (FT/Reuters/FRED > Bloomberg > CNBC/sell-side), and the abundant hard data contradicting this forecast, we weight it as political messaging rather than actionable intelligence.

Hormuz Systemic Supply Chain Disruption: Beyond Oil

WSJ/Morningstar/DigiTimes reporting that Hormuz disruptions now affect aluminum, semiconductors, pharmaceuticals, and plastics represents a broadening beyond energy that most market participants haven’t fully priced. Container shipping cancellations at record levels. Insurance premiums surging. Carriers suspending bookings. This is the largest shipping disruption since COVID.

The second-order effects: (1) pharmaceutical supply chains face 4-6 week delays → potential drug shortages in H2; (2) aluminum production constraints feed into auto/construction cost increases with multi-month lags; (3) semiconductor materials (gases, chemicals) transiting the region face shipping delays that could constrain fab output at the margin. The supply chain disruption adds a non-oil inflation channel that will appear in H2 CPI data regardless of oil price direction.

Air Carriers Diverge: Fuel-Exposed Airlines vs. Hedged

Air New Zealand warning of largest loss in four years from fuel costs creates a clear differentiation framework. Airlines with strong fuel hedging or pricing power (Lufthansa, Cathay gaining market share as Air India disrupted) outperform. US carriers face the same input pressure but have more pricing power domestically. This confirms our existing framework of margin compression in fuel-exposed businesses.

What to Watch

The options market is sending a striking signal heading into next week: SPY put skew has collapsed to just 8.1% at 1-week (down from 31.6% on May 12), meaning there is virtually no index-level protection for Monday’s Home Depot earnings. Meanwhile, VGK near-term IV at 48.4% — a full 33 percentage points above realized vol — represents the most extreme stress pricing across all 11 tracked ETFs. The credit market’s HYG put/call ratio has unwound from 6.93 to 4.09 without spreads widening, creating a binary test: either the consumer earnings window validates the protection or the thesis loses near-term probability entirely. Full options positioning analysis, portfolio playbook, and risk scenario framework below for subscribers.

This publication is for informational and educational purposes only and does not constitute financial, investment, or trading advice. The analysis, opinions, and commentary presented here should not be interpreted as a recommendation to buy, sell, or hold any security. Always conduct your own research and consult a qualified financial advisor before making investment decisions. Past performance does not guarantee future results.