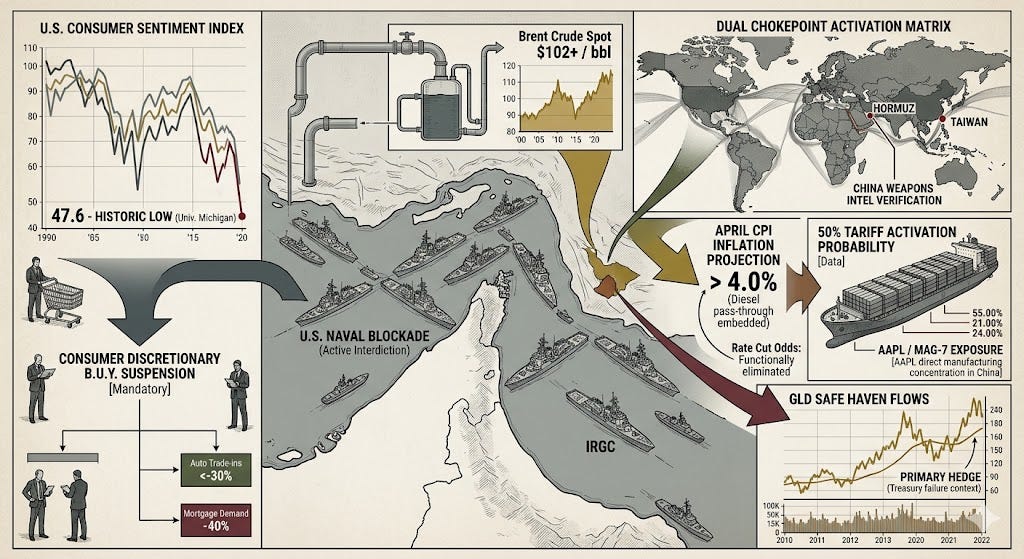

US Naval Blockade of Iran Shatters Ceasefire, Sends Oil Above $102 and Futures Reeling

China-Iran weapons intelligence triggers 50% tariff threat as consumer sentiment hits the worst reading in survey history.

The ceasefire collapsed over the weekend. The US announced a full naval blockade of Iranian ports starting Monday, sending Dow futures down 500 points and oil above $102. The US is now actively interdicting shipping rather than passively observing Iran’s crypto-toll system. Iran’s Revolutionary Guards threatened retaliation against Gulf ports. The UK refused to back the blockade. Trump simultaneously threatened 50% tariffs on China over intelligence indicating Chinese weapons shipments to Iran.

The world model’s central scenario framework held through the week: the 35-40% ceasefire collapse probability assigned last Friday materialized within 72 hours. The equity market’s full normalization (SPY IV at 15.4% on Friday) was exactly the mispricing identified in the prior brief. The Sunday night options data shows repricing already underway: SPY near-term IV has jumped to 28.1%, IWM to 40.6% (from 25.5%), and gold to 49.4% near-term. The two-regime split that defined last week — normalized equities vs. stressed credit — has partially converged, with equities now joining credit in pricing deterioration.

Three genuinely new developments require analysis: (1) the blockade itself, which is qualitatively different from the prior crypto-toll standoff; (2) the China-Iran weapons intelligence triggering a 50% tariff threat, linking the Iran conflict directly to the US-China trade relationship; and (3) consumer sentiment hitting a record low of 47.6, the worst reading in the survey’s multi-decade history.

The Blockade: From Toll Corridor to Active Interdiction

Under the toll regime, some oil flowed — reduced, expensive, but flowing. Under the blockade, the US Navy interdicts ships paying Iran to transit. This creates several new dynamics:

Direct confrontation risk with China. China had preferential Hormuz access via yuan payments. US interdiction of Chinese-flagged or Chinese-bound vessels paying Iranian tolls would constitute a naval confrontation between the world’s two largest militaries. The intelligence about Chinese weapons shipments to Iran gives the US justification to inspect Chinese vessels in the strait. China urged restraint — diplomatic language for “do not board our ships.”

Allied fracture is immediate. The UK explicitly declined to support the blockade. France is pursuing multilateral talks separately. NATO’s largest European members are not participating. This matters operationally (fewer assets available for enforcement) and diplomatically (Iran can frame this as unilateral US aggression rather than international consensus).

Oil price path shifts upward. The world model’s ceasefire-collapse scenario priced oil at $110-125. Brent has already crossed $102 on the announcement alone. If the blockade holds and Iran retaliates against Gulf ports as threatened, the $110-125 range becomes base case with $140+ as a tail. The physical-futures divergence identified Friday will likely widen further — physical crude was already at records while futures were at $97.

April CPI is now almost certain to exceed 4%. March printed 3.3% with only partial war-period capture. The blockade means April will capture $100+ oil for the full month, plus diesel passthrough already embedded at $5.29/gallon, plus additional supply compression. The 43% rate cut repricing from the ceasefire session is functionally dead. Prediction markets price April CPI >3.6% at 75% and an inflation surge above 4% for 2026 at 70% — both consistent with the framework and likely to move higher on Monday.

China Tariff Threat: The Iran-Trade Nexus

If implemented, 50% tariffs on Chinese goods would add approximately 0.5-1.0% to CPI over 6-12 months, stacking on top of the 16 existing CPI channels from the Iran conflict. Combined, this approaches the world model’s high-end H2 2026 estimate of 4.3% and could push it higher.

The Iran conflict and the US-China trade relationship are now formally linked. Every escalation in the Gulf creates a vector for trade escalation with China. This linkage did not exist a week ago. It raises the probability that the Taiwan chokepoint scenario (10-15% in the world model) becomes more than a monitoring item — if the US and China are in active diplomatic conflict over Iran, Taiwan’s risk environment changes.

AAPL is the most directly exposed Mag 7 name. Apple’s manufacturing concentration in China means 50% tariffs would either devastate iPhone margins or require unprecedented price increases. The probability of activation has increased materially.

Consumer Sentiment: The Worst Reading in History

The University of Michigan consumer sentiment index at 47.6 is the lowest reading in the survey’s multi-decade history. The prior record low was during the 2022 inflation shock. This reading captures pre-blockade consumer psychology; the blockade will likely push the next reading lower.

STZ’s guidance withdrawal, the 30.5% underwater auto trade-ins, mortgage demand at -40%, and now a record-low sentiment reading constitute a convergent dataset that any consumer discretionary position must overcome. The calibration document notes Consumer Discretionary BUY suspension is mandatory — this data reinforces that mandate.

The 47.6 reading also complicates the “bifurcated economy” framework. Business investment remains at all-time highs, but the consumer side of the economy is now objectively weaker than during any prior reading period. Recession probability at 40-45% may need upward revision if consumer spending data in coming weeks confirms the sentiment signal.

Developing Themes

Credit: Blockade Accelerates the Cascade Timeline

The credit cascade thesis (55-65% probability, 17+ data points) receives additional acceleration from the blockade. The mechanism: oil rising above $102 creates renewed mark-to-market losses for energy-exposed private credit portfolios at the exact moment March 31 NAV marks are reporting. HYG OI P/C now at 4.64 (up from 3.89 on Friday). The near-term IV dropped to 6.9%, which appears anomalous given the blockade, but the 1-month reading at 8.8% with 19.7% put skew shows stress has shifted from the immediate term to the next few weeks, consistent with NAV marks flowing into reporting. Localized credit event probability within 4 weeks: revised upward to 45-50%.

Options Market Regime Shift

The two-regime split from Friday has partially converged. SPY near-term IV jumped from 15.4% to 28.1% — the 14.7pp spread over HV is the most extreme richness since the pre-ceasefire escalation. QQQ similarly to 32.2%. IWM at 40.6% (21.1pp above HV) is pricing extreme near-term stress. Every US equity ETF is now in backwardation — the universal signature of imminent event pricing.

Internationally, EWJ at 35.2% near-term (down from 59.9% Friday) has partially normalized, likely reflecting yen strengthening on safe-haven flows that partially offset Japan’s energy import cost pressure. VGK at 24.1% (up from 23.9%) confirms persistent European stress. EEM at 36.0% near-term (up from 31.7%) shows emerging markets repricing sharply for blockade impact on oil-importing nations.

GLD at 49.4% near-term is extreme — gold is being repriced as the primary safe-haven given Treasuries’ poor performance during the crisis and mixed signals from dollar strength. TLT at 19.2% near-term (up from 12.4%) shows bonds repricing for inflation, consistent with rate cut odds collapsing.

Rate Path: Cut Thesis Demolished

The 43% rate cut probability from the ceasefire session is functionally eliminated by: (1) March CPI at 3.3%; (2) oil back above $102 on blockade; (3) FOMC minutes showing hike openness; (4) IMF no-cut assessment; (5) consumer inflation expectations surging in Michigan survey. The Warsh confirmation hearing scheduled for today (April 13) gains additional significance — his stance on the rate regime during the blockade will signal the FOMC’s likely response to April CPI.

Energy Security Driving Renewable Investment

CERAWeek executives indicated the Iran conflict could accelerate renewable investment from energy security motives rather than climate imperatives (Reuters, Tier 1). This is potentially more durable politically because national security arguments have bipartisan support. However, Trump’s 2027 budget proposal moves in the opposite direction — rescinding the EPA Endangerment Finding that is the legal foundation for greenhouse gas regulation. Net effect on renewables is ambiguous. FSLR and ENPH should be monitored for whether the energy security thesis or the regulatory headwind dominates.

Continuing Themes

Iran conflict: Ceasefire collapsed within 72 hours as predicted. Blockade represents escalation beyond prior status quo. World model scenarios require revision — ceasefire-collapse scenario (35-40%) has materialized; probability space now shifts to blockade persistence vs. negotiated de-escalation vs. further military escalation.

Physical-futures crude divergence: Persists and will widen. Physical crude was at records before the blockade; blockade intensifies the supply gap.

Defense accumulation: Window compressed further. LMT Q1 earnings imminent. Both blockade continuation and any negotiated settlement support defense spending ($1.5T budget + operational costs).

SCOTUS tariff ruling (stale, 18 days): Reduced salience maintained. The 50% China tariff threat operates through different legal authority. Original ruling’s 0.3-0.5% CPI impact increasingly marginal relative to 16+ active channels.

M2 expansion: Global M2 at new highs across six economies (Blockonomi, Tier 3). This is a countervailing expansionary force with 3-6 month lag. Maintains its role as a tail risk modifier — if credit cascade materializes, M2 expansion limits the downside duration.

This publication is for informational and educational purposes only and does not constitute financial, investment, or trading advice. The analysis, opinions, and commentary presented here should not be interpreted as a recommendation to buy, sell, or hold any security. Always conduct your own research and consult a qualified financial advisor before making investment decisions. Past performance does not guarantee future results.