US-Iran Peace Deal Sends Oil Below $100 as AI Hardware Cycle Hits Sixth Demand Confirmation

AMD's 20% earnings surge and Nvidia-Corning infrastructure partnership reinforce the semiconductor fortress even as energy positions face their first genuine threat in months

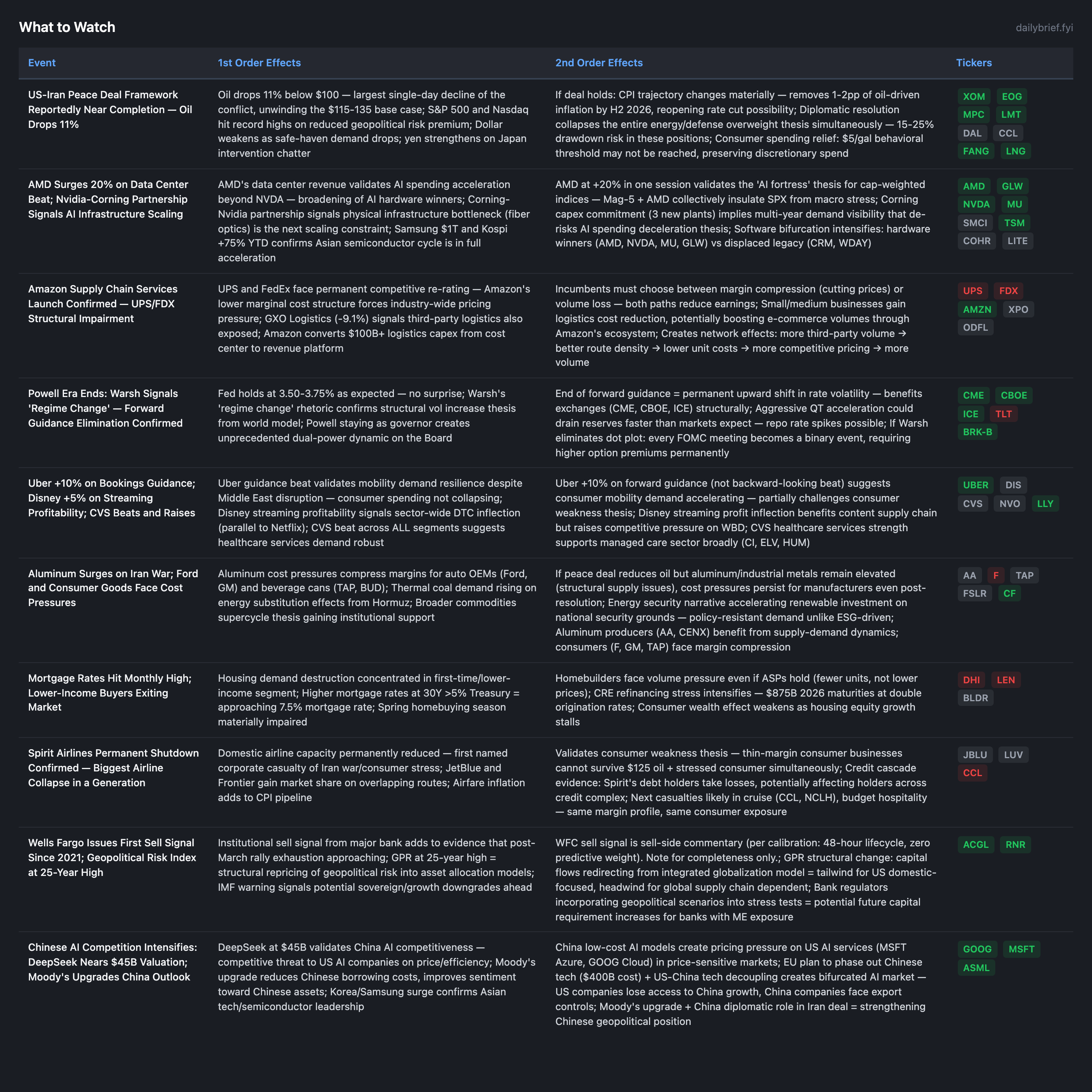

The macro landscape has shifted materially since the May 5 brief. The dominant development is a credible US-Iran peace deal framework (Reuters Tier 1, Pakistani confirmation, FT reporting) that sent oil down 11% below $100 and equity indices to new record highs. This represents the first genuine threat to the energy/defense overweight thesis that has underpinned positioning for months. Simultaneously, AMD’s 20% earnings surge, the Nvidia-Corning optical fiber partnership, and Samsung reaching $1T market cap provide the 6th independent semiconductor demand confirmation, further strengthening the AI fortress supporting cap-weighted indices.

The critical analytical question has inverted from May 5. Yesterday’s brief focused on downside catalysts (30Y at 5%, HSBC contagion, credit cascade). Today’s question: does the peace deal framework represent the 8-12% diplomatic resolution scenario materializing, or is this the 12th iteration of the “discount vague diplomatic signals” pattern that has produced 0-for-11 results? The answer determines whether energy positions unwind 15-25% or whether buying the dip in oil names is the correct response.

My assessment: the deal signals are qualitatively different from prior iterations (multiple independent sources, Chinese diplomatic pressure, Trump military pause, Pakistani confirmation, one-page framework detail), but the 48-hour ultimatum + active vessel strikes in the Strait mean the deal is binary and incomplete. I upgrade diplomatic resolution probability from 8-12% to 20-30% — meaningful enough to reduce position sizes in energy/defense but not sufficient to exit entirely.

Peace Deal Framework: Qualitatively Different from Prior Diplomatic Noise

This warrants full treatment because it potentially invalidates multiple core positions. Reuters (Tier 1) reports a one-page memorandum involving Iran’s nuclear enrichment moratorium and US sanctions lifting. Four independent signals support credibility:

Pakistani sources confirm (novel — third-party verification absent in prior 11 failed signals)

China called for Hormuz reopening in direct talks with Iran’s FM (unprecedented Chinese pressure)

Trump paused military escort operations (operational action, not rhetoric)

Iran FM met Chinese counterpart ahead of Trump-Xi summit (diplomatic choreography suggesting prepared outcome)

Against this: Trump simultaneously threatened “escalated bombing” with a 48-hour response window, and a CMA CGM container ship was struck in the Strait with crew injuries on the same day peace was being discussed. The contradiction is deliberate — maximum pressure plus diplomatic off-ramp is classic negotiation brinkmanship.

This signal scores higher than any prior iteration on specificity (one-page framework, nuclear moratorium, sanctions relief, multiple confirmations). It still lacks: chokepoint status verification, supply normalization mechanism, and binding commitments. I cannot dismiss it as prior noise — the probability has shifted.

Investment implication: Energy positions (EOG, FANG, XOM, MPC, VLO) face 15-25% drawdown risk if deal closes. The correct response given 20-30% resolution probability is to reduce position sizes by 20-30% (proportional to probability), not to exit entirely. The remaining 70% of positions are protected by: (a) even with a deal, oil takes months to normalize (per HFI Research on sustained supply shortages), (b) infrastructure damage ($58B) persists regardless of ceasefire, and (c) 10 of 11 prior signals failed.

AMD +20%: AI Hardware Cycle Broadening Beyond NVDA

AMD’s data center revenue beat crushed estimates by a sufficient margin to produce a 20% single-day move — the largest earnings-driven move in AI hardware this quarter. Goldman upgraded to buy. This is the 6th independent semiconductor demand confirmation (joining Korea +48%, SK Hynix +12%, Samsung 50x, QCOM data center, GFS beat).

The AMD beat matters specifically because it demonstrates AI demand is broad enough to support multiple hardware winners simultaneously. NVDA’s dominance was already established; AMD proving it can capture meaningful data center share at scale validates the entire AI infrastructure capex thesis. Combined with the Nvidia-Corning partnership (three new US optical fiber plants), the AI buildout timeline extends with physical infrastructure commitments that signal multi-year visibility.

The Corning partnership deserves emphasis: when NVDA commits its supply chain partner to building three dedicated manufacturing plants, it reveals demand confidence at a level no analyst estimate can match. Corporate capital allocation decisions outperform analyst forecasts for commodity/infrastructure direction (per analyst lessons).

SPY at Record Highs While Vol Structure Returns to Complacency

The S&P 500 and Nasdaq hitting new highs while SPY near-term IV sits at 11.9% (essentially equal to 12.4% HV) represents a complete unwinding of the May 4 vol spike. The 19.6% near-term reading from two days ago has collapsed to 11.9% — confirming the April 27 pattern of rapid vol normalization rather than sustained stress.

Calibration question: was the May 4-5 vol spike a false signal, or is today’s compression the false signal? The peace deal news provides an explanation for the normalization, but it also creates a dangerous setup: if the deal collapses (70-80% probability per my assessment), vol will reprice from an even more complacent base than May 2’s 8.6%.

What to Watch

The options market is flashing a critical divergence: SPY implied vol has collapsed back to 11.9% — essentially fair value — while HYG put/call open interest remains at an extreme 5.30 with 1-week put skew at 26.0%, indicating institutions have not unwound credit protection despite the peace deal euphoria. GLD options at -4.9pp below realized vol offer the cheapest geopolitical hedge in weeks, and 3-month SPY protection at just 13.7% IV captures both the 48-hour deal-failure binary and June’s unprecedented Warsh FOMC at minimal cost. The premium section below details specific positioning adjustments — including where to trim energy exposure proportional to updated deal probabilities, how to exploit the GLD vol discount, and the risk scenarios that determine whether today’s complacency is the setup for the next violent repricing.

Full options positioning analysis, portfolio playbook, and risk scenario framework below for subscribers.

This publication is for informational and educational purposes only and does not constitute financial, investment, or trading advice. The analysis, opinions, and commentary presented here should not be interpreted as a recommendation to buy, sell, or hold any security. Always conduct your own research and consult a qualified financial advisor before making investment decisions. Past performance does not guarantee future results.