US-Iran Ceasefire Triggers Massive Repricing, But Markets Are Overshooting on Multiple Dimensions [UPDATED]

Credit markets flash their most extreme stress signal of the entire crisis even as equities surge — and 15 inflation channels remain active despite oil's 16% plunge.

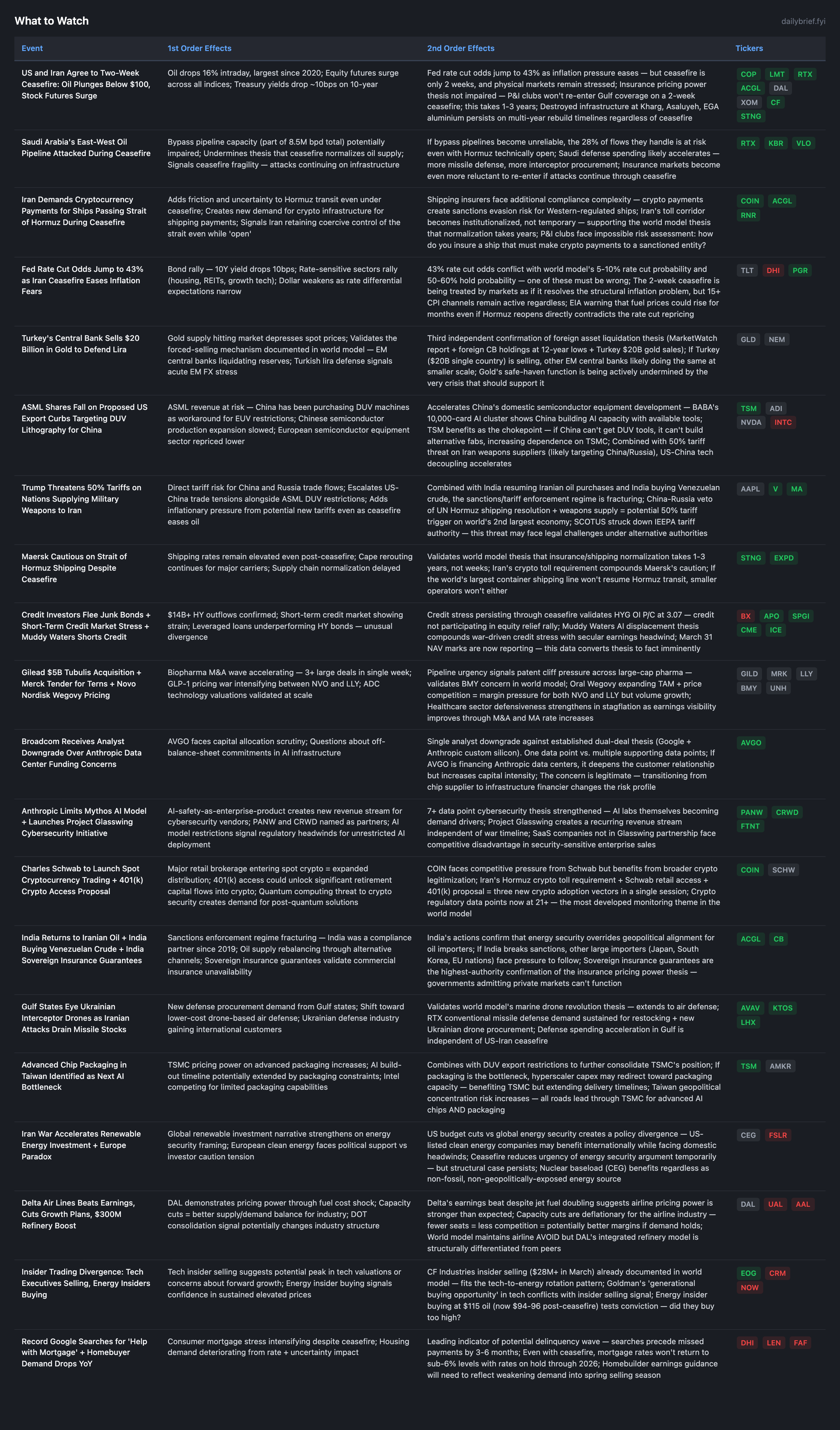

The ceasefire between the US and Iran announced April 8 is the most consequential geopolitical development since the war began on February 28. Oil crashed 16% intraday — Brent to ~$94, WTI to ~$96 — the largest single-session decline since 2020. Equity futures surged (S&P +2.6%, Dow +1,200, Nasdaq +3%). Treasury yields dropped ~10bps on the 10-year. Markets repriced Fed rate cut odds to 43% for 2026, up from the world model’s 5-10%. The market is treating this as a resolution, but it is likely overshooting on several dimensions simultaneously.

Three facts prevent the ceasefire from resolving the underlying macro regime. First, the ceasefire is two weeks long, contingent on Hormuz reopening, and core demands between Washington and Tehran remain unresolved. Goldman Sachs warns upside may be limited. Saudi Arabia’s East-West pipeline was attacked during the ceasefire. Iran is demanding cryptocurrency payments for Hormuz transit, adding compliance friction that P&I clubs cannot navigate without sanctions risk. Maersk explicitly stated it remains cautious about resuming Hormuz shipping. Second, the physical infrastructure destruction documented across prior briefs — Kharg Island, Asaluyeh, EGA aluminium, SAMREF, Kuwait refining, Jubail petrochemical, now the Lavan refinery — persists on 3-5 year rebuild timelines independent of any diplomatic outcome. The structural oil floor drops from $105-115 to perhaps $95-105 under a durable ceasefire, but cannot return to pre-war levels ($75-85) because the supply has been physically destroyed. Third, Turkey’s central bank selling $20 billion in gold to defend the lira is the third independent data point confirming the foreign asset liquidation thesis. EM central banks are depleting reserves at scale. This forced-selling dynamic has structural momentum that a 2-week ceasefire does not arrest — the accumulated damage to EM balance sheets takes quarters to repair.

The rate repricing to 43% cut probability is, in my assessment, the most mispriced element of today’s market reaction. The ceasefire eases one of 15+ active CPI channels (oil). It does not reverse diesel passthrough (+40% already embedded), used car prices at summer 2023 highs, fertilizer supply disruption, aluminium capacity destruction, petrochemical supply loss, or shipping reroute surcharges. The EIA explicitly warned that fuel prices could rise for months even if Hormuz reopens. If the ceasefire collapses after two weeks, the rate cut repricing reverses violently. Even if it holds, the accumulated inflationary impulse from six weeks of $100+ oil is still working through the pipeline on 3-6 month lags. I maintain the world model’s rate regime: 50-60% hold, 30-40% hike, 5-10% cut.

Ceasefire Mechanics and Fragility Assessment

The ceasefire has specific terms: Iran opens Hormuz, US suspends bombing for two weeks, and negotiations proceed. Multiple sources (AP, Reuters, CNBC) corroborate. Unlike prior peace signals, this is an executed agreement, not a proposal.

Three immediate complications undermine durability. Iran’s demand for cryptocurrency payments for Hormuz transit (FT, Tier 2) transforms the strait from a freely navigable international waterway into a toll road. Shipping insurers face an impossible position: insuring vessels that must make crypto payments to a sanctioned entity creates sanctions evasion liability. This is a deliberate friction that keeps Iran’s coercive control intact even during “reopening.” The Saudi East-West pipeline attack during the ceasefire (FT, Tier 2) demonstrates that not all parties have ceased hostilities — whether this is an Iranian proxy, Houthi action, or opportunistic strike, it signals that Saudi infrastructure remains vulnerable. Maersk’s explicit caution about resuming Hormuz shipping (Reuters, Tier 1) confirms that the world’s largest container line treats this ceasefire as insufficient basis for route resumption.

Revised scenario probabilities post-ceasefire:

Ceasefire holds and extends to permanent deal: 15-20% (up from 10-15% pre-ceasefire)

Ceasefire collapses within 2 weeks, escalation resumes: 30-35%

Ceasefire extends but without full resolution, low-level tension persists: 35-40%

Rapid re-escalation beyond pre-ceasefire levels: 10-15%

The oil floor adjusts: $95-105 under durable ceasefire (down from $105-115 pre-ceasefire), $110-125 if ceasefire collapses, $85-95 only under permanent comprehensive deal (15-20% probability).

Rate Cut Repricing: The Market’s Most Probable Error

The jump to 43% rate cut odds is a one-variable repricing (oil) of a multi-variable problem. FRED data as of April 7 shows: Core PCE at 3.1% (1.1pp above target), 5Y breakeven at 2.61% (still rising), CPI rising, Core CPI rising. None of these reverse because oil dropped from $115 to $94.

The CPI pipeline model has 15+ active channels. Oil passthrough is the largest single channel (+0.8-1.5%), but even if oil sustains below $100, the six weeks of $100+ oil already produced: diesel at $5.29/gallon (embedded in trucking costs for 6+ weeks), airline fuel cost increases passed through as higher fares (Delta raised bag fees, cut capacity), fertilizer prices elevated by Hormuz closure (86% of Gulf→East Africa flows ceased), petrochemical feedstock costs embedded in manufacturer contracts, used car prices at summer 2023 highs from pre-war consumer stress, and shipping reroute surcharges (Cape +112%) already contracted.

Musalem (Reuters, Tier 1) said no need to change rates even before the ceasefire. The IMF (Bloomberg, Tier 1) said little scope for cuts. The March FOMC minutes showed “several participants” suggesting the next move could be a hike. Wells Fargo abandoned cut expectations. The institutional consensus is hold, not cut. The 43% cut pricing reflects options market dynamics and momentum traders rather than the weight of institutional and central bank evidence.

If the ceasefire collapses in two weeks, the 43% cut repricing reverses to zero in a single session, with cascading effects on rate-sensitive assets that rallied today.

Credit Markets: Ceasefire Doesn’t Resolve the Cascade

HYG OI P/C dropped from 5.17 (April 7 PM) to 3.07 (April 8). This is a meaningful reduction but remains heavily put-dominated — 3.07 puts per call in open interest is still extreme by any historical standard. Volume P/C at 3.29 shows current trading flow remains put-dominant. The ceasefire reduced the binary risk premium in credit positioning but did not normalize it.

Near-term HYG IV spiked to 33.3% (27.9pp above HV of 5.5%) — the steepest backwardation of any reading in the crisis. This appears anomalous: a 33.3% near-term IV in a credit ETF during a ceasefire suggests someone is pricing an imminent credit event independent of the geopolitical outcome. Possible explanations: (1) March 31 NAV marks are reporting now and someone has early information about write-downs; (2) the ceasefire itself triggers credit events by collapsing oil prices, which impairs energy-exposed borrowers who were counting on sustained high prices; (3) options market maker dynamics creating a technical distortion.

Explanation (2) deserves attention. A rapid oil decline from $115 to $94 creates mark-to-market losses for energy-exposed private credit portfolios analogous to PSX’s $900M inventory loss. Private credit funds that lent to E&P companies at $80 oil on the assumption that prices would remain elevated face potential covenant triggers if oil stays below $100. The ceasefire that helps the broad equity market could simultaneously accelerate credit stress in energy-exposed private portfolios.

I maintain credit cascade probability at 55-65% (slightly reduced from 60-68%, reflecting ceasefire reduction of one tail risk, but the NAV mark cycle remains the catalyst and is now actively reporting).

Turkey Gold Sales: Foreign Asset Liquidation Thesis Upgraded

Turkey’s $20 billion in gold sales to defend the lira (FT, Tier 2) is the third independent data point confirming the foreign asset liquidation cascade. The thesis now has: (1) MarketWatch report on EM countries selling US assets and gold; (2) foreign CB Treasury holdings at NY Fed lowest since 2012; (3) Turkey $20B gold sales. Three data points from independent sources constitutes a confirmed pattern, not a hypothesis.

The mechanism: $100+ oil for 6 weeks → energy importers face acute dollar shortages → central banks sell most liquid assets (gold, Treasuries) → gold price declines despite geopolitical crisis → Treasury demand weakened despite rate attractiveness. The ceasefire eases but does not resolve this: EM balance sheets have been damaged by $500+ billion in incremental oil costs (rough estimate: ~15M bpd of import-dependent consumption × $30-40/bbl premium × 42 days = $189-252B in excess costs, with multiplier effects through supply chains). This depleted capital doesn’t return instantly.

The strong 3-year Treasury auction (2.68 bid-to-cover, 11.2% dealer) from April 7 remains a counter-signal. But it occurred before the ceasefire and the massive oil repricing. The next Treasury auction will be more informative — it will show whether the ceasefire has stabilized foreign demand or whether the structural damage persists.

Foreign asset liquidation probability: 30-35% (slightly up from 25-30%, reflecting Turkey confirmation as third data point, partially offset by ceasefire easing near-term pressure).

Defense: The Accumulation Moment

Defense stocks will pull back on the ceasefire. LMT, RTX, NOC, GD, HII, LHX, and LDOS all trade with some war premium that compresses as acute hostilities pause. Prior conflicts (Gulf War, early Iraq) show defense stocks initially pull back on ceasefire/peace signals, then resume uptrend as appropriations process confirms spending levels.

The structural thesis is unchanged and arguably strengthened. The $1.5T budget proposal is in congressional process regardless of ceasefire. Gulf states are seeking Ukrainian interceptor drones because their missile stocks are depleted — this procurement cycle operates on 2-5 year timelines. Saudi pipeline attack during ceasefire confirms infrastructure remains vulnerable. The Kharg Island and Asaluyeh destruction requires sustained US military presence in the region even under peace. $500M/day operational costs don’t stop immediately. LMT Q1 earnings this week will be the first defense report of the cycle — expectations for forward guidance are high.

A 5-10% defense pullback on ceasefire is the entry point the framework prescribes.

Energy: Structural Floor Recalibration

The ceasefire drops the oil floor from $105-115 (post-Kharg) to $95-105 (ceasefire with destroyed infrastructure). Even at $95, E&P companies like COP, EOG, and OVV are highly profitable. The pre-war floor was $75-85. Destroyed Iranian capacity (Kharg, Asaluyeh), damaged Saudi infrastructure (pipeline attack), depleted Gulf refining capacity (SAMREF, Kuwait, Jubail), and insurance market closure mean that global supply cannot normalize for years regardless of diplomacy.

The oil pullback is smaller than it appears in structural terms. $94 Brent is still 25-30% above February levels. No drilling response has materialized at $116 (confirmed by 3+ sources on capital discipline). No drilling response will materialize at $94 either. SPR depletion continues. OFS remains bearish (HAL, SLB) because capital discipline has structurally decoupled services from prices.

Shell’s disclosure of Q1 production losses paired with oil trading gains (Reuters, Tier 1) shows the integrated major model: production headwinds offset by trading volatility income. XOM’s Q1 production losses are the first concrete quantification of conflict impact on major oil output.

Refiners (VLO, MPC) benefit from continued Gulf capacity destruction — the crack spread advantage persists because competitor capacity was physically destroyed. CF Industries thesis (12+ data points, MAX conviction) is unaffected — fertilizer supply disruption from Hormuz operates on different timelines than crude oil, and the ceasefire doesn’t address fertilizer shipping routes.

Obligatory disclaimer: This publication is for informational and educational purposes only and does not constitute financial, investment, or trading advice. The analysis, opinions, and commentary presented here should not be interpreted as a recommendation to buy, sell, or hold any security. Always conduct your own research and consult a qualified financial advisor before making investment decisions. Past performance does not guarantee future results.