US Equity Options Flip to Backwardation as Hormuz Naval Confrontation Triggers Violent Vol Repricing

Credit markets remain eerily calm at 30-year tight spreads while institutional put positioning hits extremes — the divergence resolution is the next major macro event.

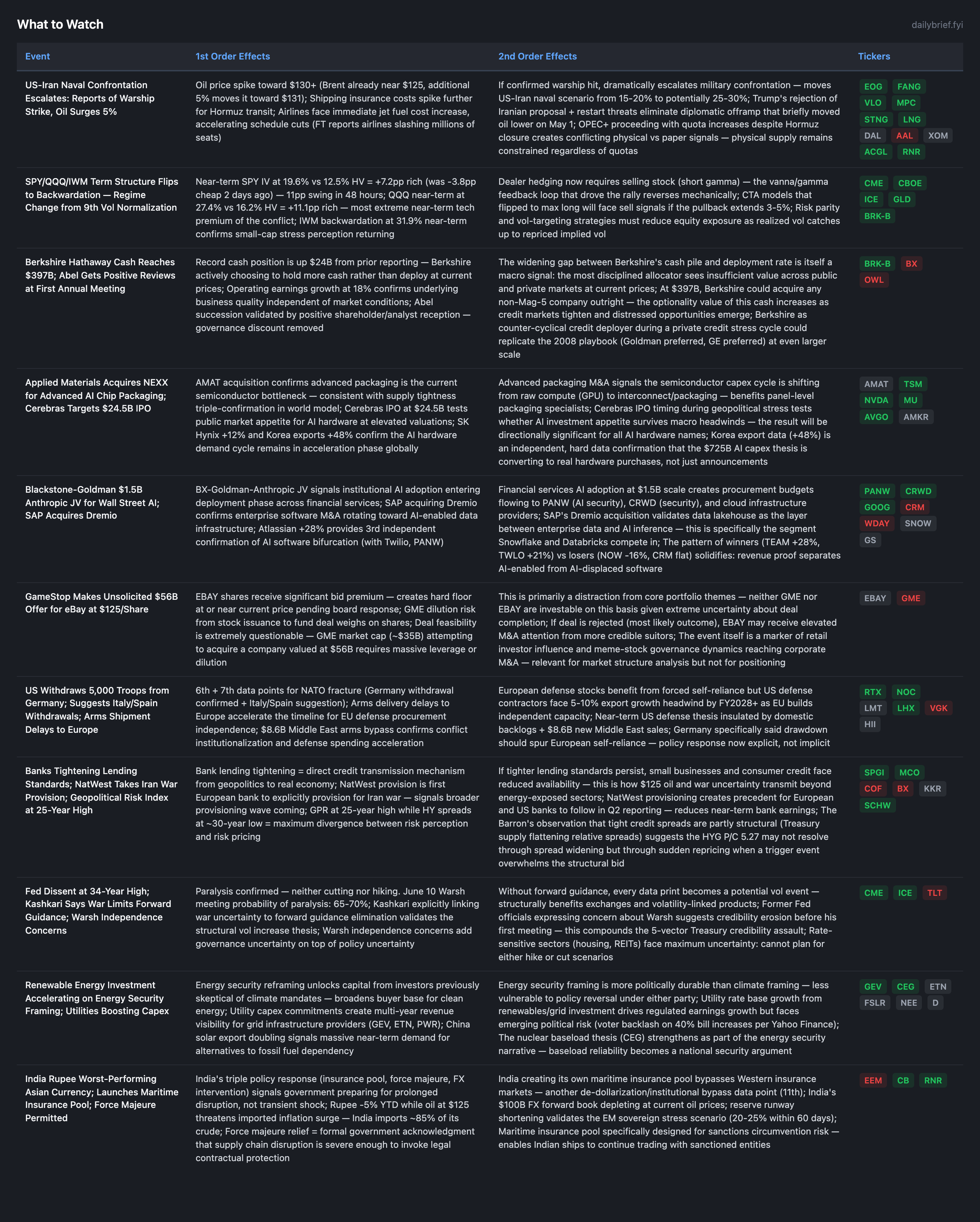

The macro picture shifted abruptly over the weekend. The most significant development is the regime change in US equity options: SPY, QQQ, and IWM all flipped from contango to backwardation between May 2 and May 4, with SPY near-term IV surging from 8.6% to 19.6% — an 11pp swing in 48 hours. The 9th vol normalization cycle identified in the prior brief repriced within the exact 5-10 trading day window that historical precedent predicted. The catalyst was a disputed US-Iran naval confrontation in the Strait of Hormuz (reports of a warship strike, though Washington denied), combined with Trump’s rejection of Iran’s diplomatic proposal and threat to restart strikes.

This validates the core positioning thesis from prior briefs: protection was cheap at 8.6% IV, and the repricing arrived faster than even the base case suggested. The equity-credit divergence remains unresolved — HYG spreads are still at 2.83% while institutional put/call OI sits at 5.27 — but the equity leg is now beginning to acknowledge the risk the credit leg has been pricing for weeks.

Vol Regime Change: Backwardation Across All US Indices

The options market underwent a structural shift between May 2 and May 4. On May 2, every US equity index was in contango with IV below HV — the deepest complacency of the entire conflict. By May 4, every major US equity index is in backwardation with IV above HV:

SPY: 8.6% → 19.6% (1-week); from -3.8pp discount to +7.2pp premium

QQQ: 11.9% → 27.4%; from -4.3pp to +11.1pp

IWM: 13.2% → 31.9%; from -6.1pp to +12.5pp

This is the most violent near-term vol repricing of the entire conflict period. GLD also flipped from -12.0pp discount to +9.5pp premium (36.8% near-term vs 27.4% HV). EWJ repriced from flat to backwardation (28.4% near-term). EEM shows similar stress (29.3% near-term, +10.7pp rich).

The mechanical implications are severe. Every vol-targeting and risk-parity strategy that added equity exposure as vol compressed to 8.6% must now reduce exposure as vol jumps to 19.6%. CTAs at maximum long face technical sell triggers. Dealer hedging shifts from supportive (long gamma as vol fell) to oppressive (short gamma as vol rises). The prior brief’s estimate of 60-65% of the rally being mechanical amplification means that same proportion is now vulnerable to mechanical reversal.

The critical question: is this a transient spike (like the April 27 episode where SPY went from 11.1% to 25.4% then normalized back to 12.7% within 4 days) or the beginning of a sustained repricing? The difference this time: the catalyst is an active naval confrontation with disputed warship strikes, not a ceasefire collapse. Escalation potential is structurally higher.

Hormuz Naval Confrontation: Disputed Strike Elevates Scenario Probabilities

Reports that Iran struck a US Navy ship (denied by Washington), combined with confirmed attacks on a tanker off Fujairah and a bulk carrier, represent the most direct US-Iran military engagement of the conflict. Trump rejecting Iran’s proposal to reopen Hormuz and threatening to restart strikes eliminates the diplomatic offramp that briefly moved oil lower on May 1.

The world model’s naval confrontation scenario was assigned 15-20% probability. The disputed warship strike — even if unconfirmed — raises the perceived probability of direct escalation. Oil surged 5% intraday. OPEC+ proceeding with quota increases is irrelevant to physical supply when the strait is functionally closed: quotas are paper, shipping routes are physical.

The combination of Trump’s escalation rhetoric, disputed military engagement, diplomatic proposal rejection, and airlines slashing millions of seats globally suggests the conflict has entered a higher phase of intensity. Spirit Airlines’ shutdown as the first corporate casualty is likely to be followed by others in cruise (CCL, NCLH), budget hospitality, and consumer-facing businesses operating at thin margins.

Citi Quant Analysts: Markets Beginning to Price Stagflation

MarketWatch reports Citi’s quantitative team flagging that markets are in the “early stages of pricing in stagflation.” This is the first sell-side quant shop to explicitly characterize the current market as transitioning to stagflation pricing. Combined with the vol regime flip, it suggests the institutional consensus is shifting from “ignore inflation/war, buy AI” to “acknowledge multi-vector stress.”

This is a 2nd independent data point (after the GPR 25-year high Forbes piece) that institutional risk frameworks are formally incorporating the stagflationary environment. The practical implication: asset allocation models that input “stagflation” produce very different outputs than “growth with elevated inflation” — specifically, they reduce equity weight, increase commodities/gold, and favor short duration.

Credit Divergence: HYG P/C OI at 5.27, Spreads Still 2.83%

HYG put/call OI ratio reads 5.27 (slight decrease from 5.31 on May 2, within measurement noise). Near-term HYG IV at 5.1% remains complacent while 1-week put skew is 21.0% (extreme). The credit market’s schizophrenia continues: institutions hold massive protection, spreads haven’t moved, and now a real default (Spirit) has occurred. BDC NAV reporting this week (May 5-11) remains the highest-probability near-term catalyst for credit repricing.

AI Hardware: Korea Exports +48%, SK Hynix +12%, AMAT Acquires NEXX

The semiconductor demand cycle received another independent hard data confirmation: South Korean exports surged 48% YoY in April, driven almost entirely by chip demand. SK Hynix +12% confirms memory demand for AI. Applied Materials’ acquisition of NEXX validates advanced packaging as the current bottleneck. Cerebras targeting a $24.5B IPO tests public market appetite for AI hardware at scale.

The AI earnings thesis remains the single strongest counter-argument to the bearish macro setup. Nothing in this week’s data weakens it. Whether AI earnings growth at the Mag-5 can hold up the cap-weighted index while the other 495 companies face $125+ oil, tighter lending, and consumer strain is unresolved.

European Multi-Front Crisis Deepens

NATO fracture now at 7 data points (Germany withdrawal confirmed + Italy/Spain suggestion). Auto tariffs at 25%. Arms delivery delays confirmed. VGK options in backwardation at 21.0% near-term vs 14.9% HV (+6.1pp rich). European recession probability remains >65% within 6 months, with auto sector now absorbing direct tariff shock on top of energy costs and reduced military security guarantees.

Continuing Themes

Iran conflict: institutionalized, escalating toward direct naval confrontation. Diplomatic resolution: 5-8% (unchanged). Oil: $125+ and rising on confrontation reports. FOMC: paralyzed with 34-year dissent; Warsh governance concerns adding credibility risk. Consumer: 16+ weakness signals + Spirit corporate casualty. Food inflation: quintuple-confirmed. De-dollarization: 10+ data points (India maritime insurance pool adds 11th). Private credit cascade: 75-85% probability.

What to Watch

The vol regime change validated the positioning thesis, but the more important question now is what happens next. SPY 3-month IV at 14.0% still underprices the June 10 Warsh FOMC by roughly 1.5pp. HYG credit vol remains static at 5.1% near-term even as equity vol doubled — the credit leg hasn’t repriced, and BDC NAV marks this week (May 5-11) carry 55-65% probability of triggering that repricing. Meanwhile, the escalation scenario has been upgraded to 15-25% probability, with specific implications for when to take partial profits on equity protection versus holding through the next catalyst cluster. Full options positioning analysis, portfolio playbook, and risk scenario framework below for subscribers.

This publication is for informational and educational purposes only and does not constitute financial, investment, or trading advice. The analysis, opinions, and commentary presented here should not be interpreted as a recommendation to buy, sell, or hold any security. Always conduct your own research and consult a qualified financial advisor before making investment decisions. Past performance does not guarantee future results.