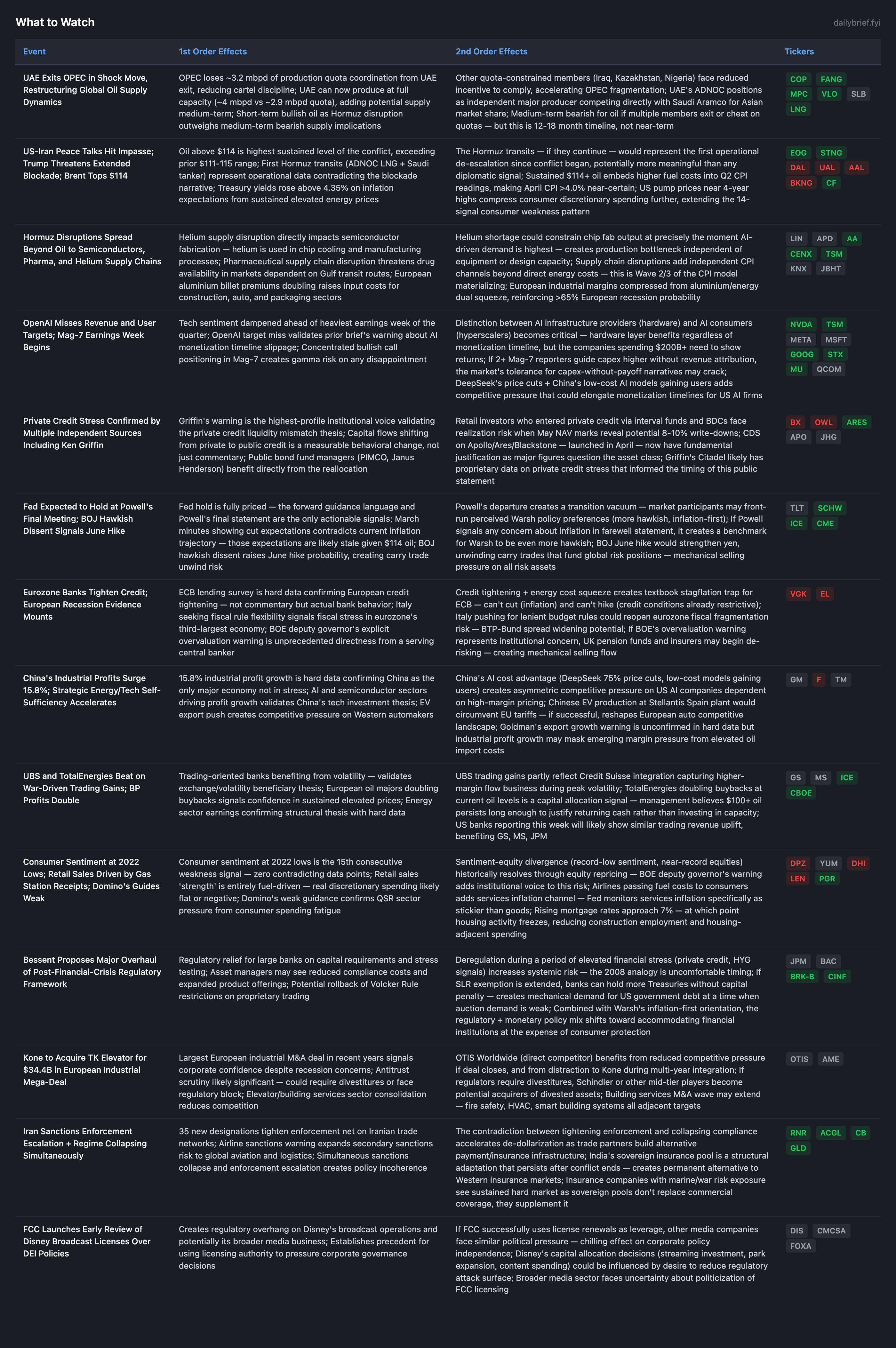

UAE's OPEC Exit Fractures Oil Supply Coordination as Hormuz Blockade Cracks

Ken Griffin adds the most prominent institutional voice yet to the private credit stress thesis ahead of a week loaded with FOMC and Mag-7 earnings

Three developments since Monday’s brief materially shift the near-term picture. First, the UAE exited OPEC — a structural fracture in global oil supply coordination with no precedent during an active Gulf conflict. Near-term this is bullish for oil (Hormuz disruption dominates), but medium-term it introduces supply discipline uncertainty that complicates the $100+ oil thesis on a 12-18 month horizon. Second, the first Hormuz tanker transits since the conflict began (ADNOC LNG + Saudi oil) provide operational data contradicting the near-total blockade narrative — physical ships moving through the strait carry more weight than any diplomatic signal. Third, Ken Griffin publicly warned on private credit liquidity risks, adding the most prominent institutional voice yet to the private credit stress thesis now at 8+ independent data points for BX.

The macro configuration heading into FOMC and Mag-7 earnings is: Brent at $114, 10Y at 4.35%, consumer sentiment at 2022 lows, and equity options in backwardation. The ECB lending survey confirming eurozone credit tightening moves European recession probability above 65%.

UAE OPEC Exit: First Structural Fracture in Oil Supply Coordination During Active Conflict

The UAE’s departure from OPEC removes ~3.2 mbpd of production from coordinated management permanently. UAE can now produce at full capacity (~4 mbpd vs ~2.9 mbpd quota), adding potential supply on a 6-12 month ramp timeline.

Near-term: Hormuz disruption overwhelms the supply implications. Oil hit $114 because the blockade constrains current supply regardless of UAE’s theoretical capacity. The exit is net bullish near-term because it signals Gulf institutional fracture that markets read as increased geopolitical uncertainty.

Medium-term (12-18 months): OPEC fragmentation is bearish for oil if multiple members follow. Iraq, Kazakhstan, and Nigeria have chronically cheated on quotas — the UAE’s formal exit removes the institutional constraint that kept even nominal adherence. If OPEC coordination breaks down while US shale responds to $100+ prices and Hormuz eventually reopens, the supply overshoot risk on the other side of this conflict is significant.

For portfolio positioning, this doesn’t change the structural energy overweight today. But it argues for tighter trailing stops on energy positions and increased awareness that the oil risk distribution has fattened on both tails — $120+ from escalation AND $75-80 from OPEC fragmentation + eventual Hormuz reopening are both more probable than a week ago.

First Hormuz Transits: Operational Data Over Diplomatic Signals

An ADNOC LNG tanker and a Saudi oil tanker crossed the Strait of Hormuz for the first time since the conflict began. Prior briefs tracked 10 failed diplomatic signals and zero operational changes. Today provides the first operational data point suggesting partial reopening.

Caveats are significant: two transits in isolation could be one-off risk-taking by state-owned entities with sovereign insurance backing (India’s new ₹130B facility enables exactly this). A sustained pattern of 15-20 ships/day would represent meaningful reopening; 2 ships is insufficient to change the base case. But this is the single most important conflict development since the blockade tightened, because it’s physical rather than rhetorical.

If transits continue at even 5-10 ships/day through the next 72 hours, the sustained blockade probability drops from 45-50% to 35-40%, and oil retraces to $100-105. If they don’t, the market will correctly dismiss this as an anomaly.

Ken Griffin on Private Credit: Highest-Profile Institutional Warning

Griffin’s public statement that retail investors “may not understand” private credit liquidity risks is the most prominent institutional voice validating the thesis. This is a fund manager with $60B+ AUM and proprietary data on credit market positioning. Combined with PIMCO, Janus Henderson, and Baird reporting measurable capital flows from private to public credit, the evidence base for the credit stress thesis has moved from “monitoring” to “established pattern”:

KKR KREF 3.9 score (bottom-up)

Blue Owl gating at 40.7% redemptions

CDS launched on Apollo/Ares/Blackstone

HYG OI P/C at 4.51 (structural put positioning)

$14B junk bond outflows (FT)

Silver Rock $4B distress fund

AI software portfolio impairment channel

Griffin warning + PIMCO/JHG/Baird flow data

BX AVOID thesis now has 8+ independent bearish data points across 4 channels with zero counter-signals.

Hormuz Disruptions Extend to Helium, Pharma, Semiconductors

Reuters (Tier 1) confirms that supply chain disruptions from the Hormuz blockade now extend beyond energy to helium (critical for chip fabrication cooling), pharmaceuticals, and industrial metals. European aluminium billet premiums doubled. This represents Wave 2/3 of the CPI model materializing — the channels beyond direct energy costs that take 30-90 days to appear in data.

The helium supply risk deserves specific attention. Semiconductor fabrication requires helium for wafer processing and equipment cooling. Qatar (Hormuz-dependent) supplies ~25% of global helium. If helium shortages constrain fab output, it creates a production bottleneck that existing equipment and design capacity cannot solve. This would be bullish for chip pricing (TSM, NVDA benefit from scarcity pricing) but bearish for the volume of chips reaching the market — potentially constraining AI infrastructure buildout at its most critical phase.

For CPI: aluminium premium doubling, diesel cost spikes into freight, pharmaceutical supply disruption, and helium shortages each represent independent inflationary channels. The 20+ channel model now has hard data confirming channels 18-22. April CPI >4.0% probability: 75-80%.

Iran Diplomatic: Impasse Confirmed, Blockade Rhetoric Escalated

US-Iran negotiations stalled over the weekend. Trump escalated rhetoric and rejected Tehran’s latest proposal. Diplomatic probability remains at 8-10% for near-term resolution. The physical Hormuz transits may represent a back-channel operational accommodation rather than a diplomatic breakthrough.

Mag-7 Earnings: OpenAI Miss Sets Negative Tone

OpenAI’s reported miss on revenue and user targets (WSJ, Tier 2) was covered in Monday’s brief. Today’s additions: Nasdaq futures -0.6% heading into the week, concentrated bullish call positioning still in place, and QQQ near-term IV at 26.9% in backwardation. The setup for gamma-driven amplification of any Mag-7 disappointment remains intact. MSFT, META, AMZN, AAPL all report this week.

Qualcomm reportedly developing custom chips for OpenAI is a positive single data point for QCOM’s AI diversification but doesn’t change the NVDA/TSM structural thesis — it confirms demand for AI silicon from multiple architectural approaches.

Consumer Contraction: 15th Consecutive Signal

Consumer sentiment at summer 2022 levels. Retail sales “beat” driven entirely by 15.5% gas station receipt spike (consumers spending more on fuel, not goods). Domino’s weak guidance. Trump approval at new low on cost-of-living. Mortgage rates rising again. Airlines hiking fares. Booking Holdings cut revenue forecast. This extends the streak to 15 signals with zero contradicting data points.

Yum Brands’ Taco Bell 8% SSS is the only partial counterpoint, but it confirms the mechanism: value-oriented fast food gains share while full-service and mid-price dining lose. The consumer is trading down.

European Recession: ECB Lending Data Confirms

The ECB lending survey showing eurozone banks tightening credit is hard data — actual bank behavior, not sentiment. Combined with doubled aluminium premiums, Germany’s Ifo at 2020 lows, UK retail collapse, Italy pushing for fiscal rule flexibility, and the three-front energy crisis, European recession probability exceeds 65% within 6 months. VGK options in backwardation at 22.2% (7.6pp above HV) is the market’s cleanest expression of this consensus.

BOE deputy governor publicly calling stock markets overvalued is unprecedented for a senior central banker. This suggests institutional concern about financial stability from asset prices disconnected from fundamentals.

Continuing Themes

Fed policy: Hold expected at Powell’s likely final meeting. March minutes showed rate cut expectations that are now stale given $114 oil and 4%+ CPI trajectory. Warsh transition looms.

Defense: No new data this session. LMT HOLD, RTX BUY, HII BUY, NOC BUY. NATO fracture monitoring continues.

Fertilizer: Reuters confirms Iran war fertilizer squeeze threatens next year’s harvests — 19th bullish data point for CF/MOS thesis.

De-dollarization: Sanctions enforcement escalation + sanctions regime collapse = policy incoherence that accelerates alternative infrastructure. 8th data point (India sovereign insurance pool as permanent bypass of Western markets).

AI infrastructure: Mid-cycle demand confirmed. Hardware layer (NVDA, TSM, ASML, AVGO, MU) maintained. Seagate’s bullish outlook validates storage demand. May NVDA earnings remains definitive.

Enterprise software impairment: No new data today. Sector-wide event confirmed. WDAY, INTU, ACN pair trade shorts maintained.

What to Watch

The options market tells a more specific story beneath these headlines. QQQ’s 26.9% near-term IV with call-heavy open interest (OI P/C 0.94) creates the sharpest gamma exposure setup heading into Mag-7 earnings — market makers short calls must sell into any decline, mechanically amplifying a move that OpenAI’s miss has already primed. Meanwhile, HYG’s surface normalization to 5.2% near-term IV masks a 4.51 put/call ratio concentrated in the 3-month tenor, precisely targeting the May-June BDC NAV reporting window where Griffin’s warning finds its catalyst. And the 60-70% probability assigned to a credit event within 3 weeks sits alongside a 30-35% chance of 2+ Mag-7 disappointments triggering a 5-8% Nasdaq drawdown — two risk scenarios that could compound rather than offset. Full options positioning analysis, portfolio playbook, and risk scenario framework below for subscribers.

This publication is for informational and educational purposes only and does not constitute financial, investment, or trading advice. The analysis, opinions, and commentary presented here should not be interpreted as a recommendation to buy, sell, or hold any security. Always conduct your own research and consult a qualified financial advisor before making investment decisions. Past performance does not guarantee future results.