Twin Inflation Binaries Resolve Hot as PPI Surges 6.5%; ECB Hikes Into German Recession Risk

The AI thesis fractures from financing into demand as Oracle's free cash flow turns negative and OpenAI weighs price cuts amid signs usage is plateauing.

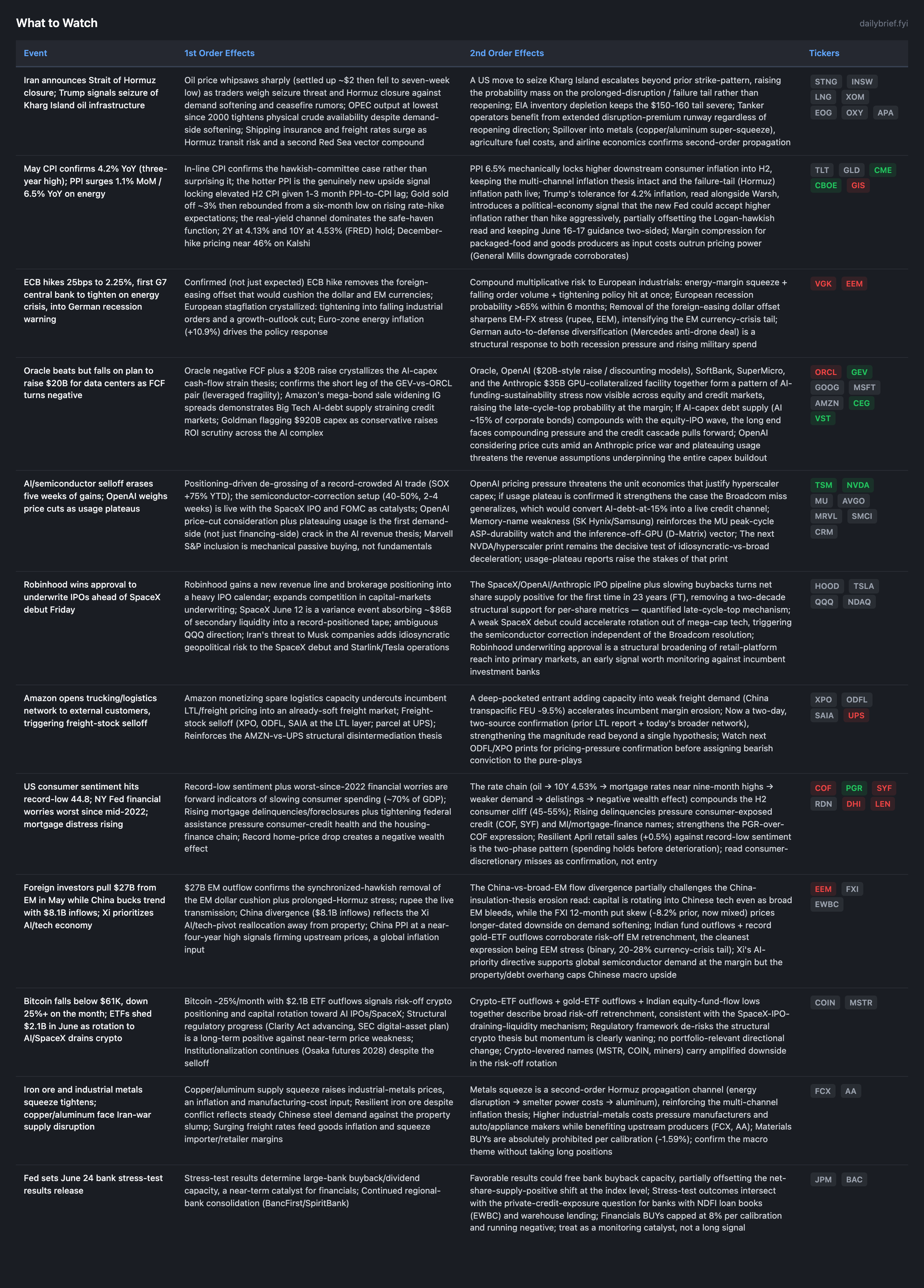

The two pending binaries resolved, and both resolved hard. May CPI confirmed 4.2% YoY (a three-year high, in line), and May PPI surged 1.1% MoM / 6.5% YoY — far above the 0.7% consensus and the largest back-to-back monthly increases since 2022. The CPI was already priced; the PPI is the genuinely new upside signal, and given the 1-3 month PPI-to-CPI lag it mechanically locks elevated H2 consumer inflation. The ECB delivered its first hike since 2023 (25bps to 2.25%), confirmed rather than expected, becoming the first G7 central bank to tighten on the energy crisis while cutting its growth outlook into a DIW German-recession warning. The foreign-easing dollar offset is now gone.

The shift on the AI thesis is more consequential than the daily chip tape. Oracle beat but fell because free cash flow turned negative and it must raise $20B for data centers, and OpenAI is reportedly weighing price cuts after enterprise complaints amid signs usage is plateauing. Oracle’s negative FCF is hard data confirming the leveraged-fragility short leg of the GEV-vs-ORCL pair. The OpenAI usage-plateau report is the first demand-side crack in the AI revenue thesis, distinct from the financing-side stress (SoftBank, SuperMicro) already on record. These do not flip the AI-infrastructure positioning, which still rests on the next NVDA print, but they raise the probability that the Broadcom miss generalizes and tighten the link between AI-capex and the credit channel (Oracle $20B raise, Amazon’s record C$14B bond sale widening IG spreads, the Anthropic $35B GPU-collateralized facility).

On Iran, the escalation is real this time in degree if not in verification: Trump stated the US will seize Kharg Island and Iran’s oil infrastructure, Iran announced a Hormuz closure, and OPEC output fell to its lowest since 2000. The verification discipline holds (oil round-tripped to a seven-week low on ceasefire rumors, 0-for-22 maintained), but the Kharg-seizure framing shifts probability mass toward the prolonged-disruption tail rather than reopening. Recession prediction markets remain sanguine (Kalshi 2026 recession 18%) against record-low 44.8 consumer sentiment, a divergence worth flagging.

PPI Surge Is the Real Inflation Signal; CPI Merely Confirmed

CPI matched the positioning the market carried into the print, so the marginal repricing was small (gold -3% then a rebound from a six-month low, consistent with the real-yield channel dominating). The new information is PPI (CNBC/MarketWatch, Tier 1-2). This is Wave-1 (energy) propagation showing up at the wholesale level before it hits the consumer, and it keeps the multi-channel inflation thesis intact and the Hormuz-failure inflation path live.

The political-economy wrinkle is new and genuinely two-sided: Trump said he is “happy with 4.2% inflation,” a stance CNBC reads as aligned with incoming Fed Chair Warsh (Tier 2). Set against Logan’s explicit hike warning and Williams’s “right place” dovishness, this signals the new Fed may tolerate higher inflation rather than hike aggressively. The binary into June 16-17 remains the guidance tone, not the move (Kalshi June hike ~2%, December hike ~46%). Do not pre-position; the dovish-Warsh asymmetry is gone but a politically-tolerant-of-inflation Warsh is not the same as a hawkish one. Two-sided.

Oracle Negative FCF and the OpenAI Usage Plateau: AI Stress Moves from Financing to Demand

Oracle’s results (CNBC, Tier 2) are hard cash-flow data confirming the leveraged-fragility thesis on the short leg of GEV-vs-ORCL. The more important item is qualitative: OpenAI is reportedly weighing price cuts after enterprise customers complained about high fees, amid a price war with Anthropic and signs AI usage is already plateauing (MarketWatch, Tier 3 — single source, treat the plateau claim as a hypothesis to monitor, but the price-war direction is corroborated by the Anthropic-IPO/Salesforce-$5B-stake competitive dynamic).

The causal chain matters. The AI-capex buildout is justified by an assumption of compounding demand and pricing power. If enterprise usage is plateauing and the two leading labs are entering a price war, the unit economics that underwrite ~$920B of projected capex (which Goldman says is too conservative) weaken. Financing stress (SoftBank -20%, SuperMicro $7B raise, Oracle negative FCF, Amazon’s record bond sale) and now a demand-side crack are both visible. This does not flip the positioning — the clean expressions stay TSM, MSFT, GOOG — but it raises the probability the Broadcom miss generalizes. The next NVDA/hyperscaler print is now the test of both supply (chip orders) and the demand assumptions underneath them. If that print confirms deceleration, AI-debt-at-15%-of-corporate-bonds becomes the live credit channel, amplified by the Anthropic GPU-collateralized precedent and Oracle’s fresh AI-purpose debt.

Trump Threatens to Seize Kharg Island; OPEC Output at Lowest Since 2000

The Iran escalation crossed a threshold in degree: Trump stated the US will seize Iran’s oil infrastructure including Kharg Island (which handles the bulk of Iranian crude exports), comparing it to Venezuela operations, while Iran announced a Hormuz closure after a downed US helicopter. A Reuters survey shows OPEC output at its lowest since at least 2000 on the US blockade of Iranian supply. The verification discipline holds — oil round-tripped to a seven-week low on Iran-Israel ceasefire rumors, and the 0-for-22 record on diplomatic signals is intact, so no position change. Seizing export infrastructure is categorically different from the strike-pause/near-deal cycle, and it shifts probability mass toward the prolonged-disruption / failure tail. EIA’s multi-decade-low inventory warning keeps the $150-160 failure tail severe; China demand softening caps the ceiling. The $100-120 grind on 2027-timeline pricing stays most probable. Energy overweight maintained, HOLD, no add (energy BUYs -1.58% across 142 calls).

Robinhood Approved to Underwrite IPOs

Robinhood received regulatory approval to underwrite IPOs, expanding from retail brokerage into investment banking ahead of the SpaceX debut Friday. This is a structural broadening of a retail platform into primary capital markets, an early signal to monitor against incumbent banks. One regulatory event, so no conviction; it lands as the IPO pipeline (SpaceX ~$86B, OpenAI, Anthropic) turns net share supply positive for the first time in 23 years. The relevant near-term variance event is the SpaceX listing itself: ambiguous QQQ direction, but a weak debut is a rotation accelerant in the post-Broadcom tape. Iran threatening Musk’s Middle East companies as military targets adds idiosyncratic risk to the debut and to Tesla/Starlink.

What to Watch

Developing Themes

ECB Hike Confirmed Into German Recession Risk

This moves the thread from “expected” to “confirmed” (CNBC/FT, Tier 1-2). The foreign-easing dollar offset is gone, which sharpens EM-FX stress (rupee, EEM) and the compound European-industrial squeeze (energy margins + falling orders + tightening policy). VGK rich at 36.1% near-term IV in backwardation. Bearish-Europe lean reinforced; European recession probability >65% within six months.

Amazon Logistics Entry: Two-Day Confirmation

Amazon opened its logistics network more broadly to external customers, driving a freight-stock selloff (CNBC, Tier 2). This is the second data point in two days (yesterday’s LTL report plus today’s broader-network confirmation), strengthening the magnitude read beyond a single hypothesis. The mechanism is unchanged: a deep-pocketed entrant adding capacity into soft freight (China transpacific FEU -9.5%) pressures incumbent LTL pricing (XPO at ~44x, ODFL, SAIA) and reinforces AMZN-vs-UPS disintermediation. I am keeping the LTL pure-plays neutral-and-monitoring pending pricing confirmation in the next ODFL/XPO prints; UPS stays the weak-leg bearish expression.

Consumer: Record-Low Sentiment, Rising Mortgage Distress

Michigan sentiment final May printed 44.8, the lowest in the survey’s modern history, below the June 2022 trough (Yahoo Finance, Tier 2), with NY Fed financial worries worst since mid-2022 and rising mortgage delinquencies/foreclosures as federal assistance tightens. The rate chain (oil → 10Y 4.53% → mortgage rates near nine-month highs → weaker demand → record home-price drop → negative wealth effect) compounds the H2 cliff (45-55%). The ~11% mortgage-demand jump is a volume blip against the price/delisting deterioration. Resilient April retail sales (+0.5%) against weak sentiment is the two-phase pattern; read consumer-discretionary misses as confirmation, not entry. Express via PGR over COF; the rising-delinquency data extends to SYF and the MI names.

EM Outflows Confirm; China Diverges

$27B left EM in May while China saw $8.1B inflows on Xi’s AI/tech-pivot directive (BW Businessworld/Economist, Tier 2-3). The broad-EM outflow plus the rupee slump and record Indian gold-ETF outflows confirm the most-stressed-complex read (EEM). The China divergence is a genuine tension with the China-insulation-erosion thesis: capital rotates into Chinese tech even as broad EM bleeds, while the FXI longer-dated put skew still prices demand-softening downside. China May PPI at a near-four-year high is a marginal global-inflation input. Aggregate this as a slow-burn signal rather than resolving it on one month’s flows.

Continuing Themes

Private credit: Amazon’s record C$14B bond sale and Oracle’s raise add AI-purpose supply to the channel; HY spread tight at 2.78% (FRED), no conversion. Fed stress-test results June 24 could free bank buyback capacity. Watch the first HYG move off 2.78%. Hold APO/ARES over BX/OWL.

Asian chip slide / value rotation: De-grossing of a crowded AI trade; memory weakness (SK Hynix/Samsung -7-8%) a marginal MU ASP-durability read. TSM the insulated expression. Marvell S&P inclusion is mechanical, not fundamental.

Defense: Multi-front demand intact; Mercedes-Benz anti-drone deal adds another European auto-to-defense data point; UK defence-secretary resignation over funding adds fiscal-political noise. RTX, NOC, GD, LMT, LHX.

Biotech/healthcare M&A: Chiesi/KalVista and Teva/Emalex closings plus Perrigo takeover speculation continue the patent-cliff consolidation bid; selective. Supports LLY and differentiated mid-caps (NBIX).

Bitcoin/crypto: Below $61K, -25%/month, $2.1B June ETF outflows on rotation to AI; Clarity Act advancing and SEC digital-asset plan structural positives. Momentum waning; no portfolio-relevant change.

GLP-1: Whey-protein shortage on GLP-1/wellness demand is a downstream confirmation of the obesity-drug demand wave; incumbent favorability (LLY, NVO) intact.

With front-end SPY IV at 29.9% against 12.2% HV but a >10% decline probability of just 3.1%, the options tape is screaming SpaceX/FOMC event-hedging rather than durable stress — and knowing which signals to trust versus discount is the difference between paying for protection you don’t need and missing the ones that matter. The genuinely durable signals sit elsewhere: EEM near-term IV at 68.3% with a -5.1% 12-month put skew as the cleanest prolonged-Hormuz-plus-hawkish-dollar expression, IWM’s structural 2.29 OI P/C surviving another cycle, and the H2 credit window now fed by Oracle’s and Amazon’s fresh AI-purpose supply against an HYG OI P/C of 3.86. The premium section maps how to position the GEV-vs-ORCL short leg, where to hold versus add in energy under the 0-for-22 verification discipline, and which of eight risk scenarios — from the Broadcom miss generalizing via demand to the Kalshi 18% recession sanguinity closing violently — deserve hedges now. Full options positioning analysis, portfolio playbook, and risk scenario framework below for subscribers.

This publication is for informational and educational purposes only and does not constitute financial, investment, or trading advice. The analysis, opinions, and commentary presented here should not be interpreted as a recommendation to buy, sell, or hold any security. Always conduct your own research and consult a qualified financial advisor before making investment decisions. Past performance does not guarantee future results.