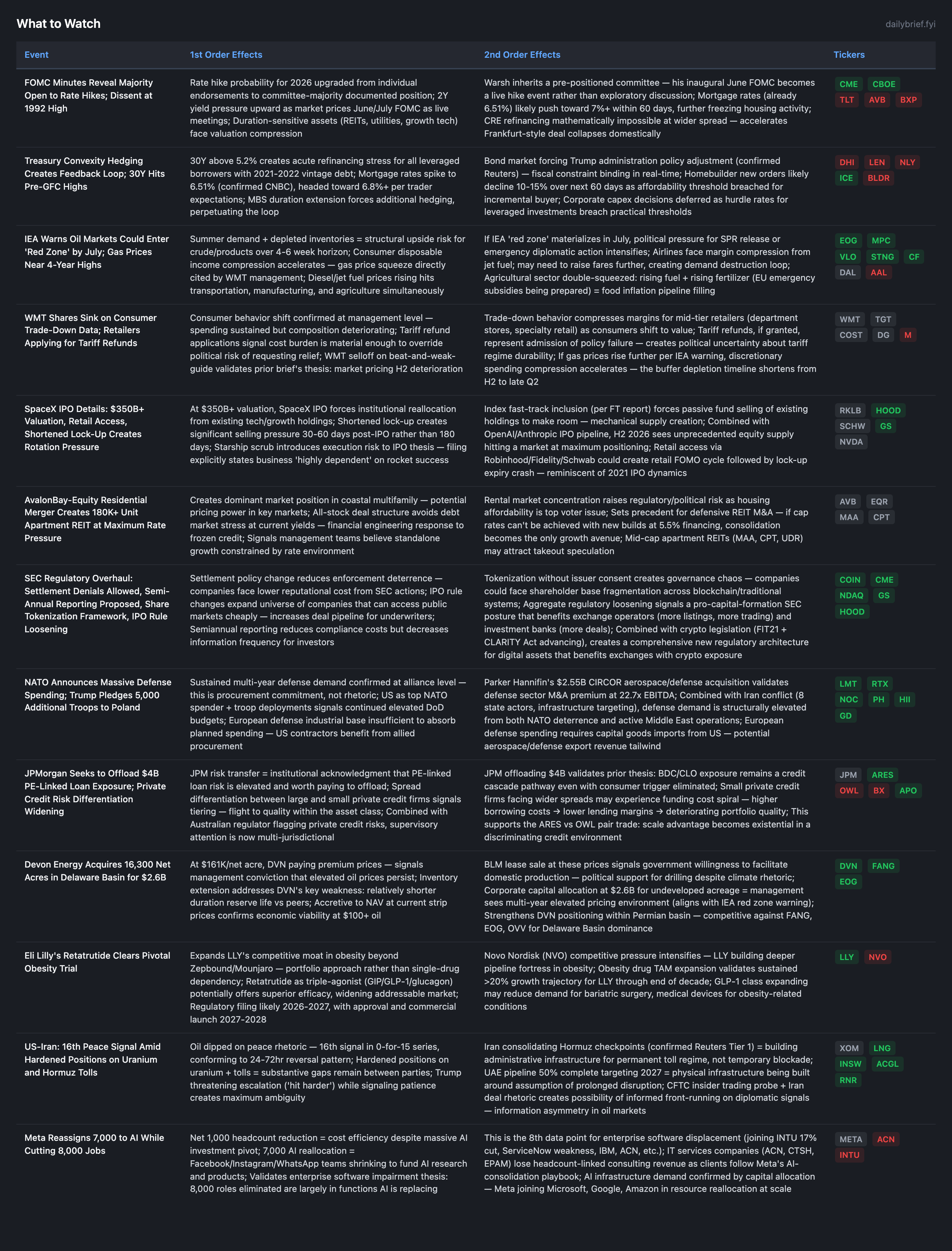

Treasury Convexity Loop Hits Pre-GFC Highs as FOMC Minutes Reveal Majority Hawkish Consensus

JPMorgan's $4B private credit offload and IEA's "red zone by July" oil warning confirm multiple stress pathways activating simultaneously.

The primary shift since yesterday: the FOMC minutes document a committee-majority hawkish position, not isolated voices. This upgrades rate hike probability from “two members endorsed” to “institutional consensus forming,” arriving simultaneously with the 30Y Treasury hitting pre-GFC highs via a convexity hedging feedback loop. The result is the tightest financial conditions configuration since 2007, with the mechanism now self-reinforcing through mortgage investor hedging.

Three secondary developments: (1) IEA’s “red zone by July” oil warning + Iran checkpoint consolidation confirms physical supply constraints intensifying ahead of summer demand, (2) JPMorgan offloading $4B in PE-linked loans validates the private credit stress pathway in our cascade thesis, and (3) SpaceX IPO structural details (retail access, shortened lock-up, $7.5T performance targets) confirm mechanical rotation pressure on existing tech holdings.

The consumer picture from prior briefs remains: WMT weak guide confirmed buffer depletion, but collapse delayed to H2. The NVDA beat-and-dip thesis from yesterday is intact. Net positioning: tightening financial conditions accelerate all medium-term structural risks while near-term catalysts (NVDA dip, consumer Q2 hold) play out as expected.

New Developments

Treasury Convexity Feedback Loop: New Systemic Mechanism

The mortgage investor hedging dynamic creating a self-reinforcing Treasury selloff represents a genuinely new market structure risk, distinct from Japan/China selling or inflation-driven yield rise. It is a mechanical, endogenous amplification mechanism.

The causal chain: rates rise → MBS duration extends (negative convexity) → mortgage investors must sell Treasuries to hedge → selling pushes yields higher → further duration extension → more hedging → more selling. Reuters (Tier 1) confirms this produced “the biggest rate spike in a year.”

This mechanism has no natural stopping point absent external intervention (Fed purchases, yield reversal from other factors, or exhaustion of hedging demand). At 30Y 5.2%+, each additional 10bp triggers additional hedging. The last time this dynamic was acutely active was 2022-2023 during the MBS runoff.

Investment implication: Shorting duration or owning rate-vol beneficiaries has a reinforcing catalyst that operates independently of fundamental inflation data. The convexity loop can persist for days or weeks once activated.

JPMorgan $4B PE-Linked Loan Risk Transfer: Institutional Stress Acknowledged

JPM seeking to offload PE-linked loan risk at a time when private credit spreads show growing differentiation between large and small lenders matters for two reasons: (1) JPM is the bellwether for institutional risk appetite — if they’re paying to transfer risk, the risk is real, and (2) it validates our credit cascade pathway via non-consumer channels even with the consumer trigger eliminated.

Combined with Australian regulatory scrutiny of private credit (Tier 3, but multinational pattern), India’s 360 ONE raising $500M for private credit amid quality concerns, and Goldman BDC 4.7% NPLs from earlier this month, we now have 5 independent data points on private credit stress building.

The ARES-over-OWL thesis gains additional confirmation: scale differentiation in funding costs is becoming existential for smaller vehicles. OWL’s 40.7% redemption + elevated bond spreads vs. ARES’s scale advantage = widening competitive gap.

Iran Checkpoint Consolidation: De Facto Permanent Toll Regime

Iran establishing island checkpoints and charging fees for Hormuz transit (confirmed Reuters Tier 1) represents a qualitative shift from “temporary wartime disruption” to “administrative infrastructure for permanent revenue extraction.” Combined with the UAE pipeline bypassing Hormuz at 50% completion targeting 2027, state actors are building physical infrastructure around the assumption of prolonged disruption.

This strengthens the structural oil thesis: even if diplomatic rhetoric continues, Iran has economic incentive to maintain the toll regime (revenue), Russia benefits from elevated prices (+39% YoY), and the physical bypass won’t complete until 2027. The minimum disruption duration is extending.

India preparing to send oil tankers through contested waters (Bloomberg Tier 1) introduces a new flashpoint: if Iran blocks an Indian tanker, it escalates the conflict to include a nuclear power with 1.4B people. This raises tail-risk probability for acute escalation even as diplomatic rhetoric suggests progress.

SpaceX IPO: Structural Capital Markets Pressure Quantified

The IPO details reveal three concerns beyond the headline valuation:

Shortened lock-up = selling pressure arrives faster than typical IPOs. Pre-IPO investors with cost basis near zero will sell early.

Business “highly dependent” on Starship (their disclosure) + Starship test scrubbed = material execution risk disclosed in the filing itself.

Musk performance awards at $7.5T = incentive structure that requires 20x appreciation, creating permanent dilution expectation.

Combined with OpenAI/Anthropic pipeline, the index rebalancing mechanics (FT analysis) force passive sellers at scale. At maximum institutional positioning (BofA survey: lowest cash since Feb 2024), the allocation money for SpaceX must come from liquidating existing holdings.

Eli Lilly Retatrutide: Portfolio Deepening in Obesity

LLY’s retatrutide clearing its pivotal trial is incrementally positive for an established thesis. The triple-agonist mechanism (GIP + GLP-1 + glucagon) represents a potentially superior next-generation approach vs. NVO’s semaglutide. If approved, LLY would have the deepest obesity pipeline (Mounjaro, Zepbound, retatrutide) creating franchise dominance.

This is the third major positive clinical readout in the obesity/GLP-1 class in 2026 — the sector’s growth trajectory is being validated repeatedly.

Developing Themes

FOMC Minutes: Majority → Warsh Inheritance (Rate Hike Probability 40-45%)

Prior brief identified Collins + Paulson as individual endorsements. Today’s minutes reveal a majority position — qualitative upgrade. Combined with record dissent (1992 highs), Warsh inherits a polarized committee on Friday. Rate hike probability for 2026: 40-45%, aligning with Kalshi at 39%. June becomes a live meeting.

FRED data shows 10Y at 4.57% and 2Y at 4.04% (as of 5/20), with 10Y-2Y spread at 0.49% — both rising in tandem signals market expects tightening, not recession. If the convexity loop pushes yields another 20-30bp before June FOMC, the committee’s majority position becomes actionable.

Consumer Buffer Depletion: Now Management-Confirmed

WMT weak guide (prior brief) + today’s consumer trade-down data (NYT Tier 2) = the thesis now has both quantitative support (savings rate 3.6%, negative real wages) and qualitative management validation. Retailers applying for tariff refunds despite political risk confirms cost burden is acute.

Retail sales (FRED): $757B in April, +4.9% YoY — but with CPI at 3.8%, real spending growth is approximately 1.1%. The headline masks stagnation in volume terms.

Enterprise Software Impairment: 9th Data Point (Meta 8,000 Cuts)

Meta’s 8,000 cuts join INTU 17%, ServiceNow weakness, IBM, ACN guidance, Datadog displacement signal, Twilio/Atlassian bifurcation, Cisco AI supercycle. The GOOG vs INTU pair trade now has 9 independent supporting data points on the short leg with zero counter-signals on the long leg.

Continuing Themes

Iran conflict: 16th diplomatic signal, 0-for-15 series. IEA “red zone by July.” Checkpoint consolidation = permanent toll regime. Energy maximum overweight unchanged.

EM currency crisis: INR 97/USD record, 8 consecutive declines, RBI dividend conscription. 20-30% probability within 30 days. Turkey market selloff (court ousting opposition figure) adds another EM stress vector.

Semiconductor correction: NVDA beat-and-dip confirmed yesterday. China gaming ban. QQQ put skew bearish. Samsung strike risk. Correction probability 40-50% within 2-4 weeks.

Credit cascade (40-45%): Consumer trigger dead. CRE + private credit pathways active (JPM $4B offload + Frankfurt collapse).

What to Watch

The options market is flashing a critical divergence: QQQ put skew has hit cycle extremes at 14.8% even as headline IV compresses — institutions are positioning for a sharp tech decline, not a gradual one. Meanwhile, IWM near-term volatility spiked to 29.5% (a +4.7pp jump from prior scan), the widest gap over historical vol across all US equity ETFs, pricing acute small-cap credit and rate sensitivity. Perhaps most unusual: EWJ call skew hit an extraordinary -54.8%, suggesting a concentrated institutional bet on Japanese equities worth monitoring. These signals, combined with the bond market’s convexity loop not yet reaching equity options (a lag that won’t persist), define the positioning environment for the next 2-4 weeks. Full options positioning analysis, portfolio playbook, and risk scenario framework below for subscribers.

This publication is for informational and educational purposes only and does not constitute financial, investment, or trading advice. The analysis, opinions, and commentary presented here should not be interpreted as a recommendation to buy, sell, or hold any security. Always conduct your own research and consult a qualified financial advisor before making investment decisions. Past performance does not guarantee future results.