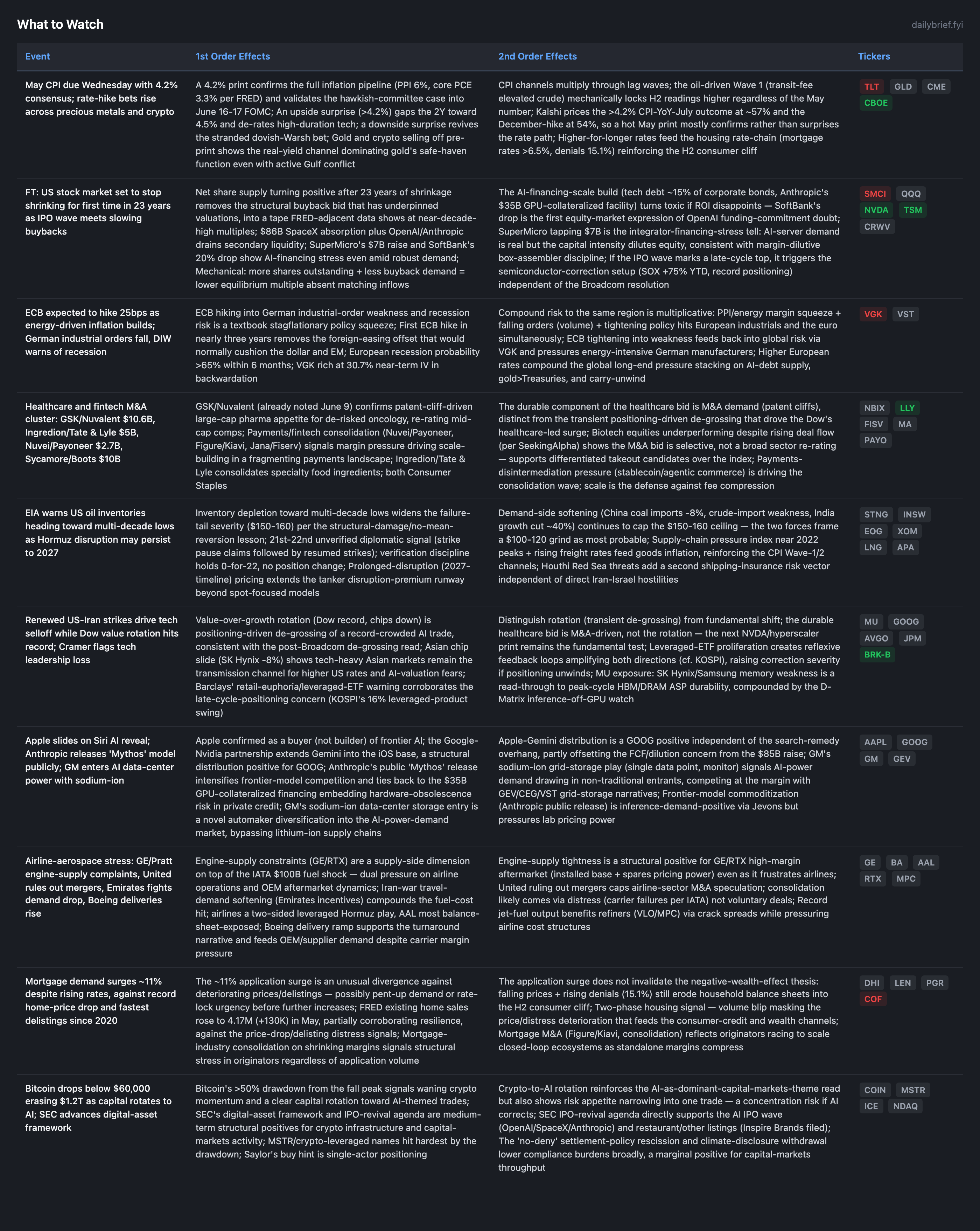

The Buyback Era Ends: AI IPO Wave Set to Turn Net Share Supply Positive for First Time in 23 Years

The ECB is poised to hike into a German recession warning just as May CPI lands Wednesday as the last major input before the June FOMC.

The landscape is largely unchanged from yesterday. Most of today’s flow restates threads already processed: Iran reversed twice more (now ~22 unverified signals, 0-for-22 on verification), the AI IPO wave and the 172K payrolls print were both covered, and the housing/private-credit/consumer threads carry no fundamental shift.

Two new items deserve weight. First, the FT quantifies the AI-supply-wave thesis structurally: the US stock market is set to stop shrinking for the first time in 23 years as SpaceX, OpenAI and Anthropic debuts meet slowing buybacks. This makes the net-share-supply drain a measurable mechanism, and it arrived alongside the first two equity-market expressions of AI-funding-sustainability doubt — SoftBank lost ~20% in a week on OpenAI funding-commitment concerns, and Super Micro fell on a $7B financing plan despite strong AI-server orders. Second, May CPI lands Wednesday at a 4.2% consensus, the last major input before the June 16-17 FOMC, with the 10Y at 4.56% and 2Y at 4.15% (FRED). The ECB is now expected to hike, into German industrial-order weakness and an explicit DIW recession warning, which removes the foreign-easing offset.

The single most important open item is unchanged: whether the Broadcom miss is idiosyncratic or the leading edge. Today’s Asian chip slide (SK Hynix -8%, Samsung -7%) and the Dow’s value rotation are positioning-driven de-grossing, not new fundamental evidence. The next NVDA/hyperscaler print is the decisive test.

The Net-Share-Supply Shift Becomes a Measurable Mechanism

The FT (Tier 2) reports the US equity market is set to stop shrinking for the first time in 23 years as IPO debuts combine with slowing corporate buybacks to turn net share supply positive. This is the quantified version of the late-cycle-top hypothesis the prior brief flagged. The mechanism is mechanical: for two decades, buybacks net of issuance removed shares and supported per-share metrics; if that flips while valuations sit near a multi-decade high, the equilibrium multiple falls absent matching inflows. SpaceX alone absorbs ~$86B.

Two data points today give this thesis its first earnings/financing-market expression. SoftBank lost its title as Japan’s most valuable company on worries about its OpenAI funding commitments and OpenAI’s ability to hit internal growth targets (MarketWatch, Tier 2). Super Micro fell after announcing the financing despite strong AI-server orders (CNBC, Tier 2). These are the leverage-build risks the world model has tracked turning visible: SoftBank is the equity-market doubt about AI-funding sustainability, and SuperMicro is the integrator-financing-stress tell. AI-server demand is real, but the capital intensity dilutes equity, which is why integrators stay conviction-neutral (box-assemblers; demand confirmation is not a buy signal).

This does not change the AI-infrastructure positioning. The clean expressions stay TSM, MSFT, GOOG; integrators and financing-dependent names (SMCI, CRWV) stay neutral-to-cautious. The supply wave plus the first financing-stress signals raise the bar but do not flip the thesis, which rests on the next NVDA print. The probability that the IPO wave marks a late-cycle top has risen at the margin.

ECB Set to Hike Into German Recession Risk

The ECB is expected to raise rates 25bps as energy-driven inflation builds (eurozone 3.2%, energy +10.9%), while German April industrial orders fell more than expected and DIW economists warn the Iran energy shock threatens to push Germany into recession (Reuters, Tier 1, three corroborating data points). This is a textbook stagflationary policy squeeze: tightening into falling orders. The world model carried this as priced; today it firms with the German-order data and the explicit recession warning. The first ECB hike in nearly three years removes the foreign-easing offset that would normally cushion the dollar and EM. Compound risk to the same region is multiplicative: energy-margin squeeze plus falling order volume plus tightening policy hit European industrials and the euro at once. VGK is rich at 30.7% near-term IV in backwardation. Bearish-Europe lean reinforced.

What to Watch

Developing Themes

May CPI Wednesday: The Last Pre-FOMC Input

Consensus is 4.2% (CNBC), and gold/crypto sold off pre-print on rising rate-hike bets. A 4.2% print mostly confirms the hawkish-committee case rather than surprising it — Kalshi prices the December hike at 54% and the >4.2% July-CPI-YoY outcome at ~57%, so the convergence the prior brief noted holds. The binary into June 16-17 is Warsh’s guidance tone, not the May number or the June move (priced ~1%). An upside surprise gaps the 2Y toward 4.5%; a downside surprise revives the stranded dovish-Warsh TLT bet. Do not pre-position; let CME/CBOE carry the vol. The full inflation pipeline (PPI 6%, core PCE 3.3% per FRED) plus the oil Wave-1 channel mean H2 readings stay elevated regardless of the May print.

Hormuz: 22nd Signal, Inventory Depletion Confirms the Failure-Tail Severity

US strikes resumed after a downed helicopter; strike-pause and near-deal claims were again followed by continuing strikes (no position change). The additive data point is the EIA warning that US oil inventories are heading toward multi-decade lows, which confirms the structural-damage/no-mean-reversion lesson and keeps the failure-tail severe ($150-160). Against that, China coal imports fell 8% and crude-import weakness persists, capping the ceiling — the $100-120 grind stays most probable on the 2027-timeline pricing. Houthi Red Sea threats add a second shipping-insurance vector. Energy overweight maintained, HOLD, no add (energy BUYs -1.58% across 142 calls per calibration).

Value Rotation and Asian Chip Weakness: De-Grossing, Not Fundamentals

The Dow hit a record on rotation into banks/healthcare/value while chips stumbled; today Asian semis slid (SK Hynix -8%, Samsung -7%, TSMC -2%) on AI-valuation fears. Read this as positioning-driven de-grossing of a record-crowded AI trade, consistent with the post-Broadcom pattern. The durable healthcare bid is M&A-driven (GSK/Nuvalent, patent cliffs), not the rotation. The memory weakness (SK Hynix/Samsung) is a read-through to MU’s peak-cycle HBM/DRAM ASP durability after its ~954% run, compounding the D-Matrix inference-off-GPU watch. Barclays’ leveraged-ETF warning is a real reflexivity concern (cf. the KOSPI 16% swing), but the rotation itself carries no new fundamental signal. The next NVDA/hyperscaler print is the test.

Continuing Themes

AI IPO/financing wave: SpaceX priced for June 12 across major brokerages; SEC’s IPO-revival and digital-asset agenda support the throughput. No change to the idiosyncratic-Broadcom read.

Private credit: Blackstone’s $2B secondary stake sale and the Anthropic $35B GPU-collateralized facility already processed; HY spread tight at 2.75% (FRED), no conversion. Watch the first HYG move off that level.

Bitcoin/crypto: Bitcoin fell below $60K (>$1.2T erased) on rotation to AI, steadying near $63K. SEC framework is a structural positive; no portfolio-relevant change.

Consumer: Campbell’s tightening-spending flag and NY Fed worries (worst since mid-2022) reinforce the H2 cliff; the ~11% mortgage-application surge is a volume blip against the price/delisting deterioration. Express via PGR over COF.

Defense: Multi-front demand intact; GE/Pratt engine-supply tightness structurally positive for aftermarket. RTX, NOC, GD, LMT, LHX.

Biotech M&A: GSK/Nuvalent $10.6B and the broader cluster confirm patent-cliff demand; biotech equities underperforming despite deal flow shows the bid is selective. Supports LLY and differentiated mid-caps (NBIX).

GLP-1: No new data; incumbent favorability (LLY, NVO) against multi-year erosion intact.

The cross-asset signals beneath the surface tell a sharper story than the headline tape. EEM is the most stressed complex in the book — near-term IV at 52.3% versus 21.3% HV, backwardated to 34.7% at twelve months with a 10.4% one-week put skew — the cleanest options expression of prolonged-Hormuz stacked on the removal of the EM dollar cushion. Meanwhile IWM carries the highest US-equity OI P/C at 2.25 and the FXI 12-month skew at -8.2% shows China demand-softening as longer-dated downside protection, even as the TLT dovish-Warsh call concentration (OI P/C 0.79) sits stranded without informational edge after payrolls. The premium section maps exactly where to lean, where to hedge, and which of the eight risk scenarios — from the quantified IPO-supply top to an EM currency crisis — to position around.

Full options positioning analysis, portfolio playbook, and risk scenario framework below for subscribers.

This publication is for informational and educational purposes only and does not constitute financial, investment, or trading advice. The analysis, opinions, and commentary presented here should not be interpreted as a recommendation to buy, sell, or hold any security. Always conduct your own research and consult a qualified financial advisor before making investment decisions. Past performance does not guarantee future results.