Stagflation Confirmed as Hard Data Locks Fed Into Paralysis at $125 Oil

Apple and Samsung independently confirm semiconductor supply tightness through 2027 as supermajors refuse White House production pressure.

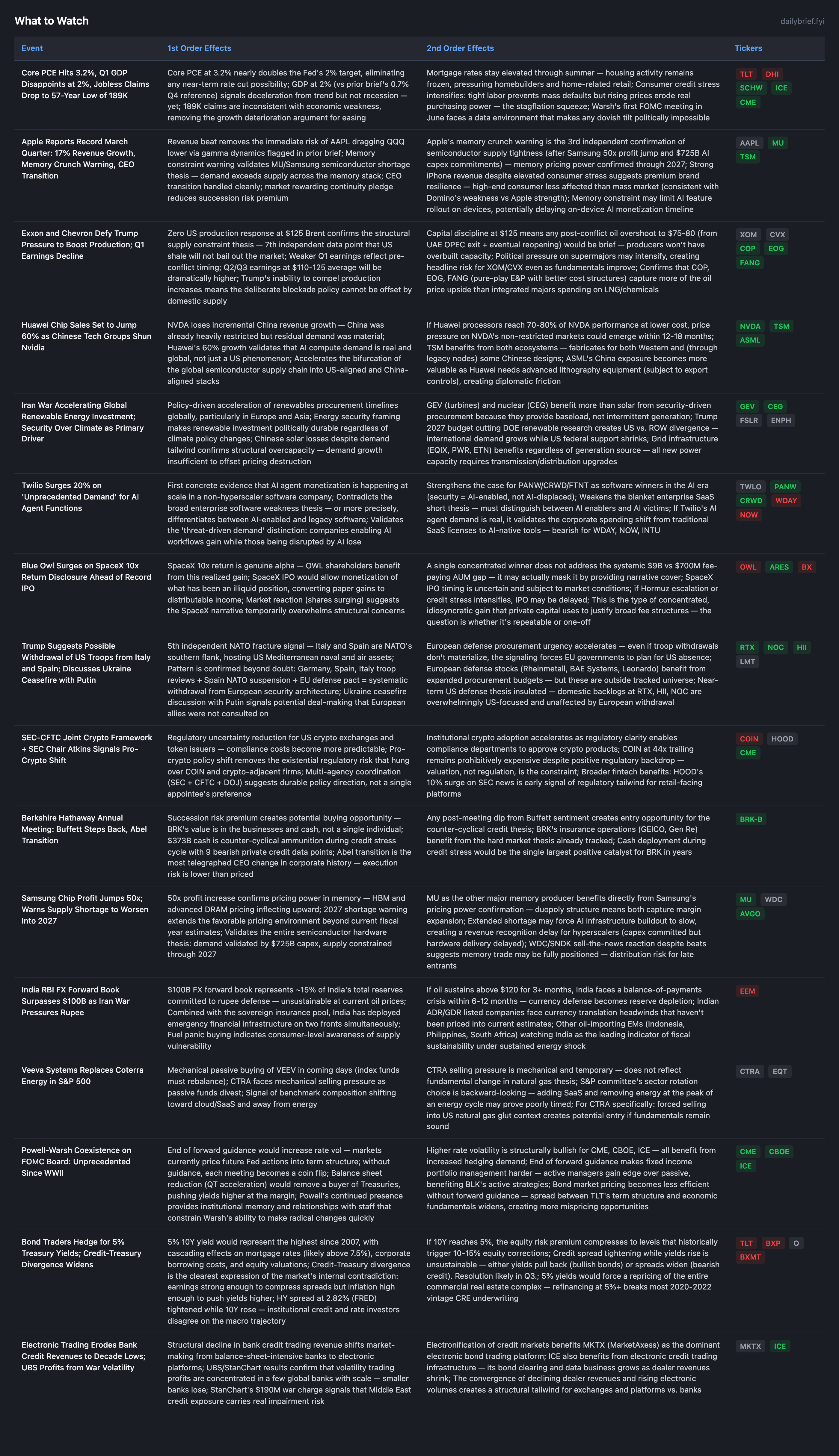

Three shifts since yesterday’s brief reframe the near-term picture. First, hard economic data crystallizes the stagflation diagnosis: Core PCE hit 3.2%, Q1 GDP disappointed at 2%, but jobless claims plunged to 189,000 — the lowest since 1969. This trifecta eliminates any Fed easing rationale while confirming growth-deceleration, locking Warsh into a paralyzed FOMC at his inaugural June meeting. Second, Apple’s record quarter and memory crunch warning, combined with Samsung’s 50x chip profit surge, provide the third independent confirmation of semiconductor supply tightness extending through 2027. Third, Exxon and Chevron’s explicit refusal to increase production despite $125 Brent and White House pressure validates the structural supply constraint that makes the energy overweight thesis self-reinforcing.

The Iran ceasefire appears to have entered a new phase: the White House indicated it pauses the 60-day War Powers deadline, suspending Congress’s leverage to force withdrawal. Combined with Trump’s months-long blockade extension discussion from yesterday’s brief, the conflict’s institutional architecture is being built for persistence, not resolution.

Stagflation Confirmed in Hard Data: PCE 3.2% / GDP 2% / Claims 189K

The simultaneous release of Core PCE at 3.2% YoY (rising), Q1 GDP at 2% (below consensus), and initial claims at 189,000 (57-year low) constitutes the cleanest stagflation signal in the data since the conflict began. Prior briefs assessed stagflation probability; today’s data removes the probabilistic framing. It is the operating reality.

The labor market is the critical piece. At 189K initial claims and 1.785M continuing claims (down 23K week-over-week), the Fed cannot credibly argue that economic weakness justifies easing. Inflation can rise without unemployment providing the countervailing signal that typically triggers Fed intervention — the Phillips curve dynamic is broken.

For the Warsh transition: his stated desire to end forward guidance and shrink the balance sheet is now boxed in by data that neither supports tightening (GDP decelerating) nor easing (inflation accelerating, labor tight). The June FOMC meeting becomes the most constrained inaugural meeting for a new chair since Volcker in 1979 — except Volcker had a clear mandate to crush inflation, while Warsh faces genuine ambiguity.

Rate path update: hold through June probability rises to 60-65%. Year-end hike probability maintained at 35-45% (conditional on sustained PCE >3.5%). Cut probability negligible at 2-3%.

Apple Record Quarter + Samsung 50x + Cook Memory Warning = Supply Tightness Confirmed

Three independent data points now confirm semiconductor supply tightness extending through 2027:

Samsung’s semiconductor profit jumped 50x with explicit warning that shortages worsen into 2027

Apple CEO Tim Cook warned of extended memory component constraints during Q2 earnings

$725B aggregate AI capex from Big Tech creates demand pull that existing fab capacity cannot satisfy

This triad validates the memory pricing power thesis that underpins MU. HBM is sold out. DRAM pricing is inflecting. NAND margins are recovering. The supply constraint is physical (fab construction timelines are 24-36 months) and cannot be resolved by software optimization or demand management.

Counter-signal: Western Digital and Sandisk beat earnings but shares declined, suggesting the memory trade may be crowded. This is a positioning risk, not a fundamental risk. The distinction matters for sizing: maintain conviction but be prepared for 10-15% drawdowns driven by profit-taking rather than thesis deterioration.

Supermajor Production Discipline: 7th Confirmation of Supply Constraint

FT (Tier 2) reports Exxon and Chevron are defying White House pressure to boost oil production at $125 Brent. This is the 7th independent data point that US shale will not provide supply relief at current prices. Prior confirmations: zero drilling rig response at $114, capital discipline commitments in Q4 earnings, investor pressure for returns over production, depletion of Tier 1 acreage, labor shortages in the Permian, and DUC (drilled but uncompleted) well inventory at decade lows.

The COP development is more nuanced: ConocoPhillips trimmed production guidance specifically because of Qatar LNG disruption from the Iran conflict. The war is simultaneously keeping oil prices elevated AND constraining one of the largest US producers from capturing the upside. COP’s domestic production benefits from $125 Brent, but the Qatar exposure creates a direct earnings headwind that other E&P names (EOG, FANG) don’t face.

Huawei 60% Chip Revenue Growth: Tech Decoupling Accelerates

FT reports Chinese tech companies are ordering Huawei AI processors at sufficient volume to drive 60% revenue growth. This is the clearest evidence yet that the global semiconductor supply chain is bifurcating into US-aligned and China-aligned stacks.

For NVDA: the China revenue loss is real but was already partially priced in via export controls. The $725B Western capex commitment dwarfs the China revenue at risk. Huawei’s growth validates that AI compute demand is structurally higher globally — the total addressable market is larger than a single-ecosystem model assumed.

For TSM: dual-ecosystem beneficiary. TSM fabricates advanced chips for Western customers while maintaining legacy node capacity that serves broader Asian demand. The bifurcation strengthens TSM’s strategic position as the indispensable supplier to both sides.

War Powers Clock Paused: Institutional Architecture for Extended Conflict

The White House indicated the Iran ceasefire pauses the 60-day War Powers Resolution deadline. Congress had a ticking clock to force debate on continued military operations. By declaring a ceasefire (however nominal), the executive branch reset that clock, removing the legislative pressure point.

Combined with Trump’s months-long blockade discussion with oil executives, Republican members breaking ranks to challenge the war, and $25 billion in disclosed military costs, the conflict is transitioning from a military event to a budgeted government program. Defense contractors benefit from the institutionalization: sustained operations require sustained procurement.

Twilio +20% on AI Agent Demand: Software Bifurcation Sharpens

Twilio’s 20% surge on “unprecedented demand” for AI agent functions is the first concrete evidence from a mid-cap software company that AI monetization is happening outside hyperscalers. The sector is bifurcating between AI-enabled winners (TWLO, PANW, CRWD) and AI-displaced losers (legacy workflow SaaS).

This is a single data point and doesn’t warrant conviction change on TWLO itself. But it reinforces the pair trade logic: long AI-enabled security/infrastructure software, short legacy enterprise SaaS. PANW’s concurrent acquisition of Portkey (AI security startup) provides a second independent data point for the AI-enabled software winners thesis.

Developing Themes

Blue Owl SpaceX 10x: First Counter-Signal (1 vs 9). OWL disclosed a 10x return on its SpaceX investment ahead of a potential record IPO. This is the first genuine counter-signal against 9 bearish data points. One concentrated winner in a single investment does not address the systemic $9B/$700M fee-paying AUM gap. The SpaceX gain is real but idiosyncratic — it doesn’t demonstrate repeatable fee generation across the portfolio. AVOID maintained; counter-signal logged. Would need 2+ consecutive quarters of fee-paying AUM growth matching capital raised to upgrade.

NATO Fracture: 5th Data Point (Italy/Spain). Trump’s “probably” on withdrawing troops from Italy and Spain extends the NATO fracture thesis to 5 independent data points (Germany review, Spain suspension, EU defense pact, Poland questioning, Italy/Spain withdrawal). The pattern is beyond established — it is now a stated policy direction. Near-term defense thesis remains insulated per prior analysis. Medium-term EU procurement autonomy is no longer speculative.

Credit-Treasury Divergence Intensifies. Reuters (Tier 1) explicitly named the divergence between credit (spreads tightening on earnings) and Treasuries (yields rising on inflation) as the defining fixed-income dynamic. HY spread at 2.82% (FRED, down 3bps) while 10Y hit 4.42% (up 6bps). Bloomberg reports traders hedging for 5% Treasury yields. This divergence resolves either via credit widening (bearish credit) or yield pullback (bullish bonds). HYG OI P/C at 5.16 — new conflict high — indicates institutional money expects the resolution to be credit widening.

Food Inflation: Confirmed by Rice Supply Threat. Reuters (Tier 1) reports world rice supply threatened by dual impact of Iran war disruptions and El Niño. This is the 4th independent food inflation data point (El Niño, fertilizer squeeze, cattle herd reduction, rice supply threat). CF and MOS thesis maintained at maximum conviction with conflict-dependent sizing.

Continuing Themes

Iran conflict: War Powers clock paused by ceasefire declaration. $25B military cost disclosed. Hormuz remains at trickle. Diplomatic resolution probability: 5-8%.

Consumer contraction: 15+ signals, zero contradictions. Unilever confirming price hikes “in small doses” adds a staples pass-through data point.

European recession: ECB and BoE both held. ECB warned of Iran war economic impact. Aluminium premiums doubled. >65% within 6 months.

De-dollarization: India RBI FX forward book past $100B = 9th data point. Institutional infrastructure for dollar bypass deepening.

Private credit cascade: OWL SpaceX = first counter-signal (1 vs 9). May BDC NAV marks approaching.

What to Watch

Today’s options signals are flashing a warning that equity investors aren’t hearing. HYG open interest put/call has surged to 5.16 — the highest reading of the entire conflict — with 1-week put skew at an extreme 41.8%, targeting a specific catalyst window around May BDC NAV marks. Meanwhile, SPY implied volatility has normalized to 12.7% (essentially at realized vol) during an active military conflict with $125 oil — the cheapest equity protection window since hostilities began. Gold options at 2.8 percentage points cheap to realized vol and FXI’s first shift to backwardation (breaking China’s insulation thesis for the first time) round out a picture of dislocated risk pricing that demands active positioning. Full options positioning analysis, portfolio playbook, and risk scenario framework below for subscribers.

Options Market Signal

US equity vol has collapsed while international markets remain in acute stress — a meaningful shift from yesterday’s broad stress pricing toward a more differentiated regime.

SPY (12.7%, flat): IV has returned to fair value (0.3pp above HV of 12.5%). The FOMC + Mag-7 earnings event premium has been extracted. This is the 8th vol normalization cycle — protection purchased at elevated levels has decayed as the market absorbed FOMC and most Mag-7 results without a systemic shock. SPY IV at HV during active military conflict with $125 oil is the cheapest protection window of the conflict. OI P/C at 1.08 is near equilibrium. If this flat regime persists through next week, the June Warsh FOMC becomes the next catalyst for repricing.

QQQ (19.1%, flat): Compressed from 27.6% in the prior brief — still 2.9pp above HV but backwardation has collapsed to flat structure. Apple’s record quarter removed the immediate gamma risk flagged previously. OI P/C at 0.88 remains call-heavy. NVDA May earnings is the next concentrated event.

HYG (4.9%, contango): Near-term vol normalized to 0.6pp above HV. But OI P/C has risen to 5.16 — the highest reading of the entire conflict. This is the single most important options signal today. Near-term complacency masking record structural put positioning. The 1-week put skew at 41.8% is extreme — concentrated near-term protection buying around a specific catalyst (likely May BDC NAV marks in the next 2-3 weeks). HY spread at 2.82% remains historically tight while institutional positioning for a credit event intensifies. This divergence between spread levels and options positioning is now at its widest.

TLT (13.4%, flat): IV rose from 12.8% to 13.4% — 3.1pp above HV. The market is repricing bond volatility higher as Treasury options traders hedge for 5% yields. OI P/C at 0.67 still call-dominated, but the call-buying for a bond rally that dominated the last two weeks appears to be fading. The structural case against duration strengthened by today’s PCE and claims data.

GLD (24.6%, backwardation): Now 2.8pp CHEAP to HV (27.4%). Gold options are underpricing realized volatility — the inverse of what you’d expect during geopolitical crisis. This makes gold options structurally attractive for both hedging and directional exposure. Gold at $4,236 (per GLD × 10) has pulled back from $4,847.

International divergence intensifies: VGK at 22.3% (7.4pp above HV, backwardation) — European stress pricing maintained at conflict highs. EWJ at 34.7% 1-week (14.8pp above HV, extreme backwardation) — the most extreme single-tenor reading of the conflict period, likely reflecting BOJ positioning and petroleum output decline. EEM at 31.0% (12.3pp above HV, backwardation) — India $100B FX defense is the primary driver. FXI has shifted to backwardation at 27.5% (7.6pp above HV) — this is new. China was the only major market in contango/calm through the entire conflict; the shift to backwardation with negative near-term put skew (-12.8%) signals emerging stress in Chinese equities, possibly from Hengli sanctions impact or broader trade war concerns. This is the first break in China’s insulation thesis and warrants close monitoring.

Synthesis: US equity vol has normalized for the 8th time while credit positioning sets a new record for bearish institutional conviction. The gold options cheapness and FXI’s first shift to backwardation are the most actionable new signals. The credit-equity divergence is at its widest of the conflict — per analyst lessons, when these diverge, credit is right ~70% of the time.