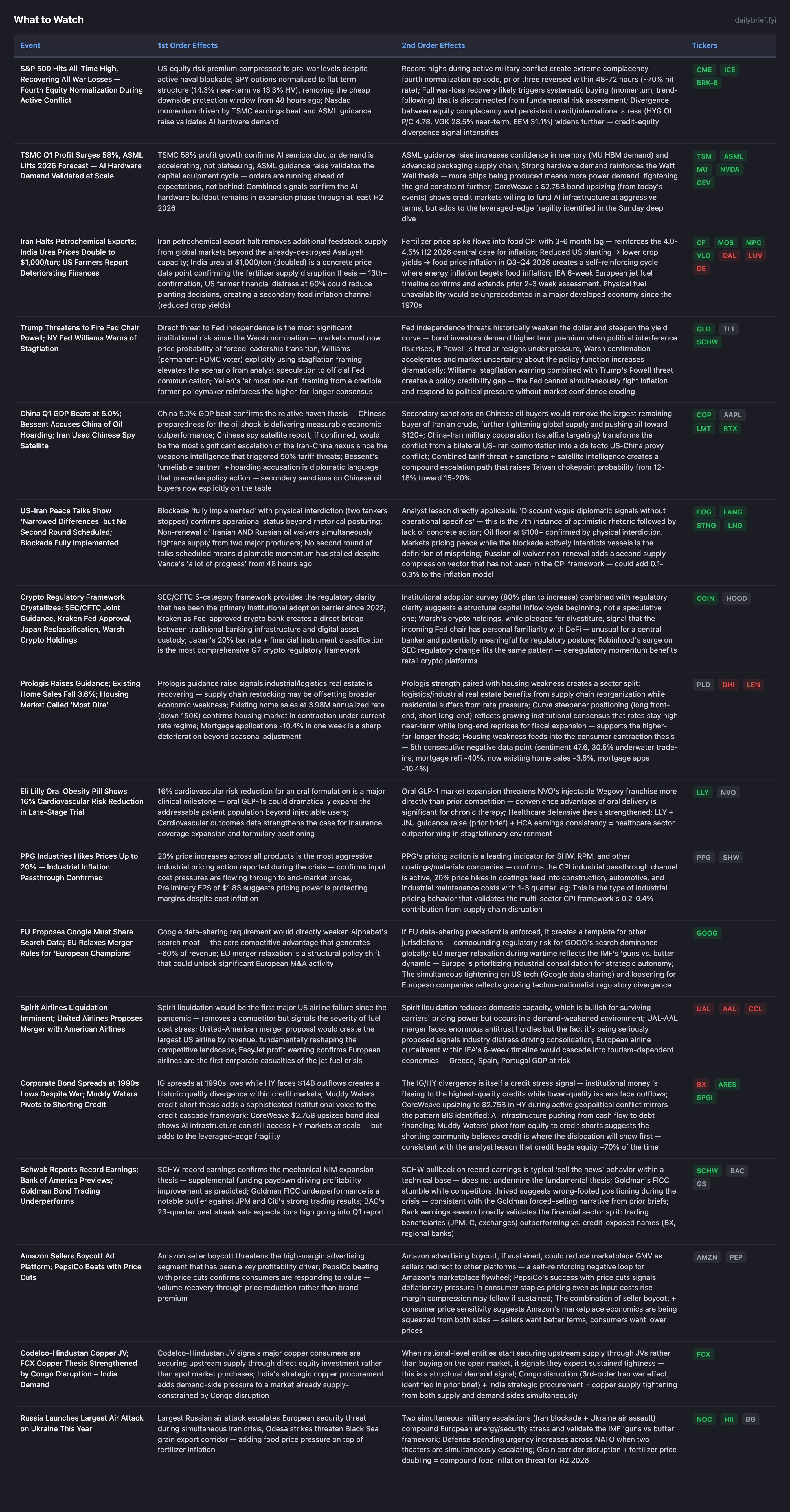

S&P 500 Hits All-Time High During Active Naval Blockade as Credit Markets Flash Distress

AI hardware earnings validate the demand cycle while fertilizer prices double, credit-equity divergence widens to crisis extremes, and Trump directly threatens to fire the Fed Chair.

The S&P 500 hit a new all-time high on April 15, fully recovering all losses since the Iran war began. This is the fourth equity normalization during an active military conflict; the prior three reversed within 48-72 hours approximately 70% of the time. SPY term structure has shifted from 28.1% near-term two days ago to nearly flat at 14.3%, removing the cheap downside protection window identified in Monday’s brief within a single session. The equity market is pricing peace while the US Navy is physically interdicting oil tankers at Hormuz.

The genuinely new information today falls into three categories: (1) TSMC’s 58% profit surge and ASML’s guidance raise validate the AI hardware cycle at scale, confirming the demand side of the Watt Wall thesis; (2) the fertilizer supply crisis has moved from thesis to hard price data — India urea at $1,000/ton (doubled), 60% of US farmers reporting financial deterioration, and Iran halting all petrochemical exports; (3) Trump’s direct threat to fire Fed Chair Powell adds a 6th data point to the Fed independence risk cluster, qualitatively different from prior political positioning. Additionally, five independent developments in crypto regulation (SEC/CFTC framework, Kraken Fed approval, Japan reclassification, Nomura 80% institutional survey, Warsh disclosures) collectively represent the most favorable regulatory environment the sector has experienced.

The credit-equity divergence has widened to its most extreme since the conflict began. HYG OI P/C at 4.78 (up from 4.65 on Monday), corporate bond spreads at 1990s lows for IG but $14B in HY outflows YTD, and Muddy Waters pivoting to shorting credit. VGK at 28.5% near-term (13.8pp above HV, backwardation) and EEM at 31.1% (12.8pp above HV, backwardation) continue pricing severe stress while US equity options price tranquility.

TSMC + ASML: AI Hardware Cycle Validated by Earnings

TSMC’s 58% YoY profit growth beating estimates and ASML raising its 2026 forecast on AI-driven orders provide the most concrete validation of the AI infrastructure buildout since the cycle began. These are realized revenue and profits from actual chip production and equipment deliveries, not forward-looking projections.

For the portfolio framework, this confirms two things: first, the demand side of the Watt Wall is real and accelerating. More chips being produced means more power demand at data centers, which tightens the grid constraint further. GEV’s 83 GW gas turbine backlog becomes more valuable when TSMC is beating by this magnitude. Second, the AI hardware cycle has not peaked despite the maturation signals discussed in the Sunday deep dive. The capital cycle concern remains valid for the financing-sensitive edge, but the core is still expanding.

CoreWeave’s $2.75B bond upsizing (from $1.75B originally) demonstrates that HY credit markets remain willing to fund AI infrastructure aggressively. This is a double-edged signal: it shows strong demand for AI assets but also confirms the BIS pattern of the AI ecosystem pushing from cash flow to debt financing. The leveraged-edge fragility identified in the deep dive is growing in real time.

Fertilizer Crisis: Thesis to Price Data

India’s urea tender pricing at $1,000/ton (doubled from prior levels) converts the fertilizer supply disruption from analytical framework to hard market price. Combined with Iran’s indefinite suspension of all petrochemical exports and 60% of US farmers reporting financial deterioration, the fertilizer supply chain is now visibly broken.

The mechanism for further inflation impact: US farmers facing fertilizer costs that have doubled + fuel costs at records → reduced planting decisions → lower crop yields in H2 2026 → food price inflation in Q3-Q4. This is a second-order channel that most CPI models have not incorporated because it operates on agricultural cycle timelines (planting decisions in spring → harvest in fall → retail prices 3-6 months later). The food inflation component of the H2 2026 CPI framework (+0.3-0.6%) may be conservative.

CF Industries remains maximum conviction. At ~9.3x revised FY2026E with 14+ independent confirmations and zero counter-signals, the analytical burden has shifted entirely to finding the first genuine disconfirming data point. The India price data is the strongest single confirmation yet.

Trump Threatens to Fire Powell: 6th Fed Independence Data Point

The direct presidential threat to fire the Fed Chair is qualitatively different from the prior data points in the Fed independence risk cluster (Bessent BOE remarks, Powell investigation, Warsh succession, Warsh disclosures, confirmation hearing). Prior incidents could be interpreted as political positioning or procedural governance. A direct firing threat is an operational challenge to institutional independence.

Williams’ explicit stagflation framing in the same news cycle provides important context: the Fed is simultaneously warning that the war could slow growth and worsen inflation while the President threatens to remove the Chair. This creates a credibility gap that bond markets will price through higher term premium. The 10Y-2Y spread at 0.53% (up 3bp) and curve steepener positioning reported by Reuters are early signs of this repricing.

For portfolio positioning, this strengthens the gold thesis (institutional hard-asset demand rises when central bank credibility is questioned) and adds urgency to the higher-for-longer rate framework (political interference risk reduces the probability of dovish pivots).

Crypto Regulatory Crystallization

Five independent crypto regulatory developments in a compressed timeframe constitute a structural regime change: (1) SEC/CFTC joint 5-category classification, (2) Kraken Fed approval as crypto bank, (3) Japan’s comprehensive reclassification with 20% tax rate, (4) Nomura survey showing 80% institutional adoption intent, (5) Warsh crypto portfolio disclosures suggesting personal familiarity with DeFi.

COIN at 41x/3.5 beta carries the most direct exposure. The HOLD rating from the world model reflected balanced regulatory tailwind vs. geopolitical headwind. With the regulatory tailwind now this strong across multiple jurisdictions simultaneously, the risk-reward has shifted materially.

Russia’s Largest Ukraine Air Attack: Dual-Theater Escalation

Russia launching its largest combined missile and drone attack of 2026 on Kyiv, Odesa, Dnipro, and Zaporizhzhia during the simultaneous Iran blockade creates a dual-theater military environment that has not existed since 2003. The Odesa strikes specifically threaten Black Sea grain exports at the same moment fertilizer prices have doubled, creating a compound food inflation channel.

Dual-theater escalation accelerates procurement across missile defense systems, naval assets, ISR platforms, and munitions. The IMF’s “guns vs. butter” framework becomes immediately relevant: governments facing two simultaneous security threats will prioritize defense spending over fiscal consolidation.

Credit-Equity Divergence: Widest Since Conflict Began

HYG OI P/C has risen to 4.78 (from 4.65 on Monday, 3.89 pre-blockade). Near-term IV at 2.6% with 1-month at 6.8% and 16.6% put skew. IG spreads at 1990s lows while HY faces $14B outflows. Muddy Waters shifting to credit shorts. The divergence is growing, not narrowing.

When credit and equity options diverge, credit is usually right (~70% base rate). The credit market is pricing 4-6 week stress while equities celebrate all-time highs. Localized credit event probability within 4-6 weeks remains 45-50%.

Blockade: Operational With Physical Interdiction

Two oil tankers interdicted by a US destroyer confirms the blockade has moved from declaration to enforcement. Bessent confirming non-renewal of Iranian AND Russian oil waivers simultaneously tightens supply from two major producers. No second round of Pakistan-mediated talks scheduled despite Vance’s “a lot of progress” claim 48 hours ago — the 7th instance of optimistic diplomatic rhetoric failing to produce concrete action.

European Energy Crisis: IEA 6-Week Jet Fuel Timeline

IEA head now warning Europe could run out of jet fuel in 6 weeks. EU developing emergency jet fuel plans. Spirit Airlines facing liquidation, EasyJet issuing profit warning. European airline operational curtailment probability within 6 weeks: revised upward to 50-60%.

Physical-Futures Crude Divergence Persists

European and African physical crude at records while futures held down by peace-talk optimism. US truckers’ diesel spending at record highs. The divergence signals that futures markets are mispricing the physical reality.

Continuing Themes

Rate path: Williams explicit stagflation warning + Yellen “at most one cut” + Trump Powell threat all reinforce higher-for-longer. Fed holds rate at 3.64%. No change to framework.

Consumer contraction: Housing sales -3.6%, mortgage apps -10.4%, RH CEO “most dire” assessment add to the 5th+ consecutive weakness confirmations. All consumer discretionary AVOID maintained.

Defense accumulation: Dual-theater escalation (Iran + Ukraine) strengthens the thesis. LMT Q1 earnings remain the key near-term catalyst.

China relative haven: Q1 GDP at 5.0% beating expectations. FXI options in contango at 20.1% (at HV) — the only major international ETF not showing stress.

What to Watch

The options market is telling a story that equity prices aren’t. HYG’s put/call OI ratio has climbed to 4.78 with a 16.6% one-month put skew — the sharpest term-structure dislocation tracked during the entire crisis — while SPY sits in flat term structure at 14.3% as if the blockade doesn’t exist. International stress readings remain extreme: VGK at 28.5% near-term (13.8pp above realized), EEM at 31.1%, both in steep backwardation. Meanwhile, the downside protection window flagged Monday has already closed, and the institutional positioning data suggests smart money is braced for a credit event within 4-6 weeks at 45-50% probability. Full options positioning analysis, portfolio playbook, and risk scenario framework below for subscribers.

This publication is for informational and educational purposes only and does not constitute financial, investment, or trading advice. The analysis, opinions, and commentary presented here should not be interpreted as a recommendation to buy, sell, or hold any security. Always conduct your own research and consult a qualified financial advisor before making investment decisions. Past performance does not guarantee future results.