Private Credit Liability Stress Broadens to a Fifth Manager as AI Debt Supply Compounds

A hot May PPI surge is contingent on Hormuz, while Oracle's negative free cash flow deepens the AI-capex credit channel.

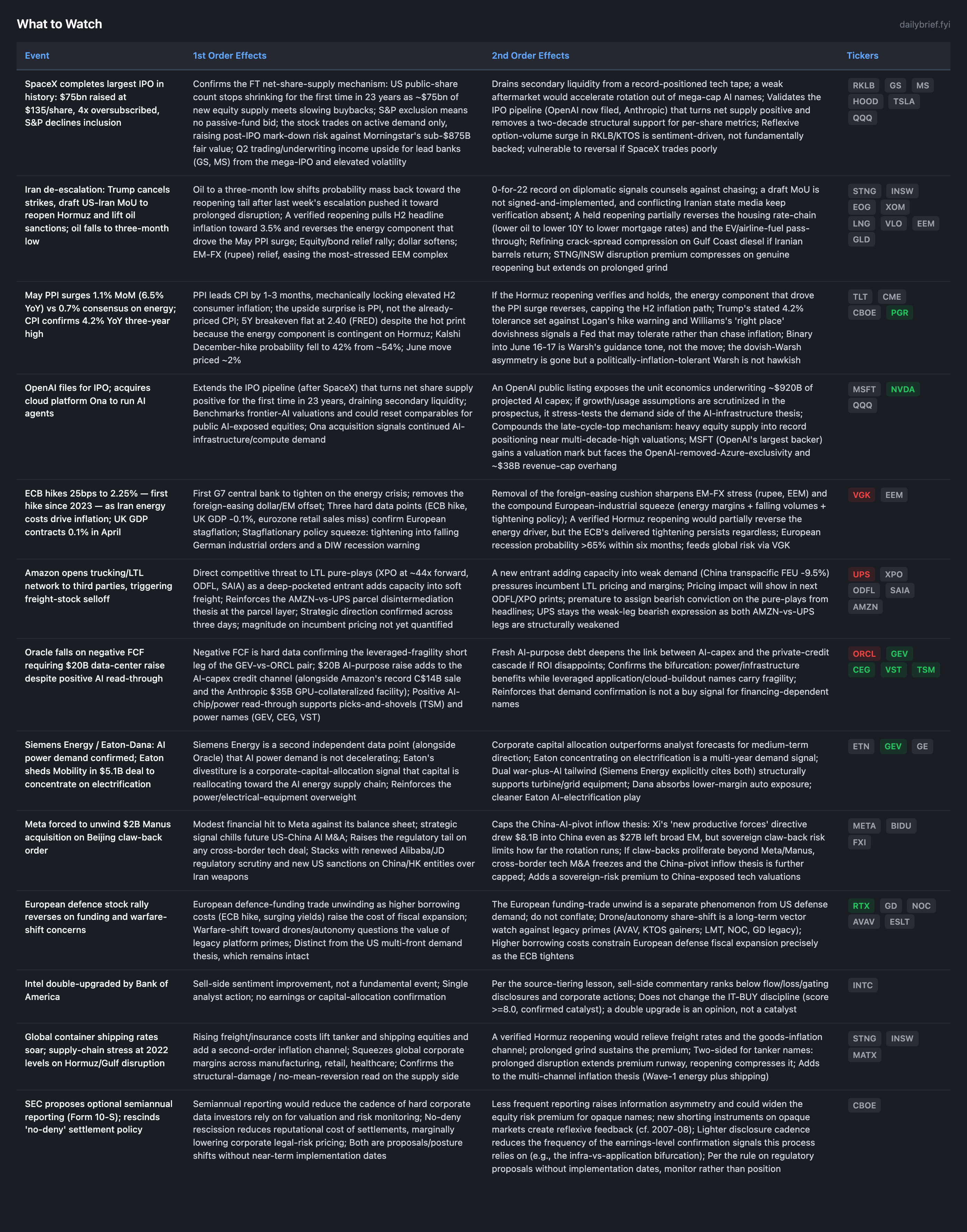

The landscape is largely a continuation of yesterday, with two binaries now partially resolved in the same direction. The Iran de-escalation reached its highest-quality signal in 22 reversal cycles: Trump cancelled strikes, a draft US-Iran MoU to reopen Hormuz and lift oil sanctions is reportedly circulating, and WTI/Brent fell to a three-month low. The 0-for-22 record and conflicting Iranian state-media signals (IRNA/Fars) the same day mean the pre-committed trigger (72+ hours of sustained uninterrupted commercial transit) is not met; energy positioning stays HOLD, no add. SpaceX completed the largest IPO in history ($75bn at $135/share, 4x oversubscribed), confirming the FT net-share-supply mechanism while the S&P 500’s decision to exclude it removes the passive bid. OpenAI’s IPO filing extends the same supply wave.

The genuinely new items are concentrated in private credit and AI leverage. BlackRock’s $13bn HPS fund honoured under 40% of redemption requests for a second consecutive quarter, adding a fifth named manager to the gating sequence and confirming that liability-side stress is broadening. CoreWeave’s subsidiary raised $900M in HY, joining the Oracle/Amazon/Anthropic AI-debt supply wave. These two together tighten the AI-capex-to-credit linkage that is the system’s primary open risk. The European defence trade reversed on funding costs, confirming the world-model distinction between the unwinding European fiscal-funding trade and structurally separate US multi-front demand. The Iran draft MoU, May PPI surge, CPI at 4.2%, SpaceX pricing, and ECB hike were all processed in detail over the prior three briefs and are carried as developments or continuing themes, not re-litigated.

BlackRock HPS Fund Gates a Fifth Time; Private-Credit Liability Stress Broadens

BlackRock’s $13bn HPS Corporate Lending Fund fulfilled under 40% of redemption requests for a second consecutive quarter (FT, Tier 2). This is the fifth named manager to gate, after Cliffwater ($31B retail fund at 17%), Partners Group (two vehicles), and Blackstone’s flagship. The pattern now has enough independent confirmations (5+) that the burden has shifted: this is a sector phenomenon, not idiosyncratic to any one manager. Second-consecutive-quarter gating at a major sponsor signals persistent redemption pressure rather than a one-off liquidity event.

The mechanism the world model has tracked (liability-side gating → asset-side liquidity management via forced secondary sales and NAV markdowns → spread repricing) now has its liability leg confirmed across five managers. The reflexivity tell remains the first HYG spread move off 2.80% (FRED HY spread, +0.02, still tight). The AI-credit linkage is the amplifier: GPU-collateralized facilities (Apollo/Blackstone Anthropic $35B) sit on books whose liability sides are now gating at five managers. Hold APO/ARES over BX/OWL; the BX flagship-gating plus stake-selling plus this fifth named gating strengthens the short legs. Fed stress-test results June 24 are the near-term input.

CoreWeave Subsidiary Raises $900M in High Yield; AI-Debt Supply Compounds

CoreWeave’s subsidiary tapped the HY market for $900M (Bloomberg, Tier 2), joining Oracle’s $20B raise, Amazon’s record C$14B bond sale, and the Anthropic $35B GPU-collateralized facility. AI-purpose debt is being absorbed at tight spreads (HY at 2.80%), so primary access remains open; the cascade is not yet pulled forward through a primary-closure channel. The structural concern is that this leverage embeds rapid hardware-obsolescence risk into HY books at the same time equity supply is building (SpaceX $75bn priced, OpenAI filing). Both supply channels of AI capital are expanding while the OpenAI usage-plateau and Anthropic price-war reports (single-source, monitor-only) raise demand-side questions. This raises the stakes on the next NVDA/hyperscaler print, which now tests both chip-order supply and the demand assumptions underwriting ~$920B of projected capex and the leverage stacked against it. CRWV stays conviction-neutral-to-cautious as a financing-dependent integrator.

European Defence Trade Reverses on Funding Costs

The European defence rally, one of the largest equity trades of recent years, reversed on rising government borrowing costs and changing warfare dynamics (FT, Tier 2). This confirms the world-model distinction: the debt-financed European rearmament trade is unwinding as the ECB’s first hike since 2023 (to 2.25%) and rising long-end yields raise the cost of the fiscal expansion that underwrote it, while US multi-front demand (Middle East + NATO/Russia + Israel-Lebanon) is budget-driven and structurally separate. US primes (GD, NOC, RTX, LMT, LHX) are insulated from the European funding mechanism. The warfare-cost narrative behind the reversal, that drone/autonomy shifts the cost curve away from legacy platforms, reinforces the long-term share-vector watch on AVAV/KTOS against the legacy primes on both continents.

What to Watch

Developing Themes

Iran: Draft MoU at Verification Threshold, Failure Tail Still Severe

No material change from yesterday’s detailed treatment. Trump cancelled strikes, a draft MoU to reopen Hormuz and lift sanctions reportedly circulates, oil hit a three-month low. Iranian state media (IRNA, Fars) gave conflicting signals; the 72-hour sustained-transit trigger is not met. The new corroborating hard data is OPEC output at its lowest since 2000, which keeps the failure tail ($150-160) severe. Energy stays HOLD, no add, no reduce. The EEM options structure shows the EM market has not yet bought the reopening despite the rupee rally.

AI-Credit Linkage Tightens

CoreWeave’s HY raise plus the HPS gating connect the two open risks. The financing-side stress (SoftBank, Super Micro, Oracle negative FCF, Amazon, now CoreWeave) and the liability-side gating (five managers) are converging on the same channel: AI leverage on books that are gating. The demand-side hypothesis (OpenAI usage plateau) remains single-source. Next NVDA print decisive.

Marvell S&P 500 Inclusion June 22

Mechanical passive buying around the effective date; index membership broadens institutional ownership. This is structural flow, not a fundamental signal, and arrives into a record-positioned SOX (+75% YTD) where the 40-50% semiconductor-correction setup remains intact. QQQ options confirm the post-Broadcom hedging is resolving: acute front-end event-hedging into FOMC/SpaceX aftermath, durable longer-dated stability.

Continuing Themes

Rates: Do not pre-position into June 16-17. Kalshi December-hike at 42%, June move ~2%; binary is Warsh’s guidance tone. 5Y breakeven flat at 2.40, 10Y at 4.55%. Let CME/CBOE carry the vol.

SpaceX/net-supply: $75bn priced, 4x oversubscribed, S&P declined inclusion (no passive bid). Slow-structural drain on per-share metrics, not a single-day shock. OpenAI IPO filing extends the wave.

European stagflation: ECB 2.25%, UK GDP -0.1% April, eurozone retail down. VGK bearish lean; options rich at 24.1% near-term in backwardation. >65% recession probability within six months.

Consumer: Housing rate chain intact (30Y 6.52%, delistings fastest since 2020) against the existing-home-sales counter-point (4.17M, +130K, FRED) — two-phase read. Jobless claims rising to 229K (FRED, +11.7% YoY). PGR over COF, extending to SYF/RDN. Consumer Discretionary BUY-prohibited.

Amazon logistics: Third-day confirmation of third-party logistics opening; UPS the weak-leg bearish expression, LTL pure-plays (XPO/ODFL/SAIA) neutral-and-monitoring pending pricing confirmation.

Power/electrical: GEV, CEG, VST, ETN overweight reinforced (Siemens Energy AI gas-turbine demand, Eaton-Dana divestiture). GEV-vs-ORCL pair CORE.

Crypto: Bitcoin down >25% on the month, long-term-holder selling, CLARITY Act stalled after advancing. Momentum waning; no portfolio-relevant change.

Healthcare M&A: Merck Animal Health/TARGAN, KKR/Crowe continue the consolidation bid; selective. Supports LLY and NBIX.

The cleanest actionable read sits in the EEM structure — a -6.6% 12-month put skew and 1-month -13.1% protection that has not bought the Hormuz reopening even after the rupee rallied — alongside the HYG OI P/C now at 3.88 with H2 stress priced and the named-gating pattern reinforced by the fifth manager. The premium section maps how to position the APO/ARES-over-BX/OWL credit pair against the building AI-purpose HY supply, where the stranded TLT dovish-Warsh bet (call-heavy 0.78, no edge into June 16-17) and the sharpening EWJ carry-unwind (49.4% near-term IV, -14.6% 1-week skew) fit the durable-vs-front-end-noise distinction, and how the eight risk scenarios — from the AI-credit linkage converting to the Hormuz failure tail reopening $150-160 — frame the hedging calendar around the June 16-17 FOMC and June 24 stress tests. Full options positioning analysis, portfolio playbook, and risk scenario framework below for subscribers.

This publication is for informational and educational purposes only and does not constitute financial, investment, or trading advice. The analysis, opinions, and commentary presented here should not be interpreted as a recommendation to buy, sell, or hold any security. Always conduct your own research and consult a qualified financial advisor before making investment decisions. Past performance does not guarantee future results.