Private Credit CDS Launch Creates First Instrument to Short Shadow Banking as Diplomatic Signals Face 0-for-7 Track Record

Former Treasury Secretary Paulson calls for emergency plan as the Fed's last dovish voice capitulates, widening the gap between equity complacency and credit stress to a fourth consecutive day.

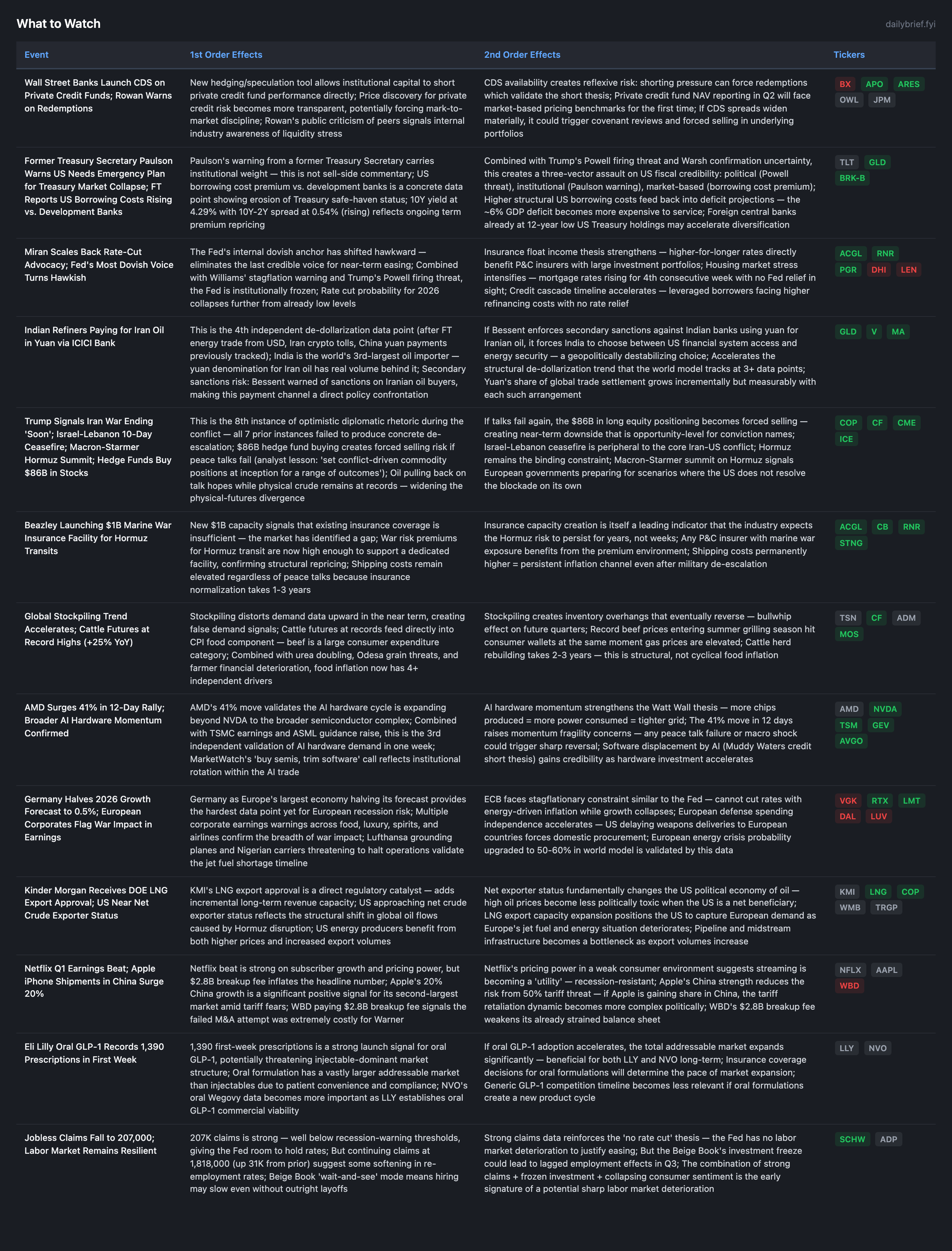

The primary shift since yesterday’s brief: the diplomatic track has moved from stalled to tentatively active. Trump signaled the Iran war “should be ending pretty soon,” a 10-day Israel-Lebanon ceasefire was confirmed, and a Macron-Starmer summit on Hormuz security was announced. Goldman data shows $86B in hedge fund stock buying on peace hopes. Oil pulled back on these signals. However, three structural developments argue the equity market’s all-time high remains fragile: (1) Wall Street banks have launched credit default swaps on private credit funds managed by Apollo, Ares, and Blackstone — the first market-based instrument for shorting private credit directly; (2) former Treasury Secretary Paulson called for an emergency plan for Treasury market collapse, while the FT reports the US is losing its lowest-cost-dollar-borrower status; (3) Fed Governor Miran, previously the most aggressive rate-cut advocate, scaled back his dovish stance, eliminating the last internal voice for easing. The credit-equity divergence identified in prior briefs persists: HYG OI P/C at 4.82 (up from 4.78 yesterday), international markets in backwardation, while SPY sits at 12.8% IV in flat term structure.

Private Credit CDS: The Short Instrument Arrives

JPMorgan and Barclays offering credit default swaps on funds managed by Apollo, Ares, and Blackstone is the most significant structural development in credit markets since the crisis began. This creates a price-discovery mechanism that previously did not exist for private credit.

First, banks are creating these instruments because they want to hedge their own exposure and because client demand for shorting private credit is high enough to justify product development.

Second, CDS availability creates reflexive dynamics. If CDS spreads widen, it validates the bear thesis, encourages more shorting, forces redemptions, and produces realized losses that widen CDS further. This is the mechanism by which localized stress becomes systemic.

Third, Rowan’s public criticism of peers who “cannot meet rising redemption requests” is an offensive move, positioning Apollo as the survivor while signaling that weaker players are already failing. When CEOs publicly attack their competitors’ liquidity, the stress is real.

This is the 7th independent stress channel for the private credit cascade thesis (adding to: private credit redemptions $20B Q1, public credit outflows $14B YTD, AI-driven leveraged loan divergence, private credit fund bonds at year-lows, blockade energy mark-to-market, Muddy Waters credit shorts). The credit cascade probability should be revised upward: 60-70%, with localized event within 4-6 weeks at 48-55%.

BX at ~46x bears the heaviest weight from this development. The CDS instrument provides a specific, liquid mechanism for institutional shorts to express the thesis that has been building for weeks.

Paulson Warning + FT Borrowing Cost Premium: Treasury Credibility Under Three-Vector Assault

Paulson calling for a Treasury market “break-the-glass” plan is qualitatively different from market commentary. He ran the Treasury during the 2008 crisis and understands systemic risk from the operational side. His warning, combined with the FT reporting that the US is losing its lowest-cost-dollar-borrower status to development banks, creates a three-vector assault on US fiscal credibility:

Political: Trump’s direct Powell firing threat (yesterday’s brief)

Institutional: Paulson’s emergency plan call (former Treasury Secretary)

Market-based: US borrowing costs rising relative to development banks (FT data)

TLT options at 9.8% near-term IV in contango are pricing zero risk of Treasury dysfunction. The world model assigns 20-25% probability to Treasury market dysfunction. This gap between options pricing and structural risk is widening. The 10Y-2Y spread at 0.54% (rising) and the curve steepener trade reported by Reuters are early signs of institutional repositioning, but Treasury options haven’t caught up.

Miran’s Hawkish Pivot: The Last Dove Falls

Miran was identified in the world model as the Fed’s most aggressive rate-cut advocate. His acknowledgment that inflation is “more persistent than expected” eliminates the last internal voice for near-term easing. Combined with Hammack’s “hold for a good while” and Musalem’s “no need to change,” the FOMC consensus is unanimous: rates stay at 3.64% indefinitely. The San Francisco Fed research paper showing “nonmarket-based” inflation keeping headline elevated provides the intellectual framework for this position.

The rate-cut probability for 2026 should be revised to 3-5% (from 5-8%). Rate hike probability conditional on April CPI >4.0% remains 50-60%.

Indian Yuan Oil Payments: De-dollarization Data Point #4

Indian refiners using yuan to pay for Iranian oil via ICICI Bank is the 4th independent de-dollarization data point tracked in the world model (after FT energy trade from USD, Iran crypto tolls, China yuan payments). This is now an established pattern. India is the world’s 3rd-largest oil importer; yuan denomination at this scale has real macroeconomic weight.

The secondary sanctions risk is the near-term catalyst: Bessent warned of sanctions on Iranian oil buyers on April 15. If the US sanctions ICICI Bank or Indian refiners for yuan-denominated Iranian oil purchases, it forces India into a direct confrontation between US financial system access and energy security, with implications for dollar reserve status, Indian equity flows, and the broader EM bloc’s sanctions compliance calculus.

Commodities Supercycle + Stockpiling: Inflation Pipeline Extending

Reuters reporting a commodities supercycle “underway” is sell-side framing (1 data point), but the underlying evidence is substantial: cattle futures at record highs (+25% YoY), India urea at $1,000/ton (doubled), Iran petrochemical exports halted indefinitely, physical crude at records, and the FT reporting accelerating corporate and consumer stockpiling.

The stockpiling dynamic creates artificial demand in the near term that inflates prices and depletes inventories faster, then reverses as overstocked inventories are worked down. For the CPI framework, this means near-term inflation reads higher than the structural level, but the unwinding creates deflationary pressure later. Net effect: sharper CPI spikes in Q2-Q3 2026, potentially softer Q4-Q1 2027.

Cattle herd reduction takes 2-3 years to reverse — this is structural food inflation that operates independently of energy or fertilizer channels.

Diplomatic Track: 8th Time Optimistic — Track Record Is 0 for 7

Trump’s “ending pretty soon” signal, the Israel-Lebanon ceasefire, and the Macron-Starmer Hormuz summit create the appearance of diplomatic progress. Goldman’s $86B hedge fund stock buying reflects institutional conviction that resolution is near.

The analyst lesson is explicit and reinforced 6 times: “Discount vague diplomatic signals without operational specifics.” The Israel-Lebanon ceasefire is peripheral to the core Iran-US conflict. No framework agreement, no Hormuz reopening timeline, no binding commitments. The 7 prior optimistic signals (March 10, March 22, March 23, April 1, April 9, April 13 Islamabad) all reversed within 24-72 hours.

The $86B in hedge fund buying creates asymmetric risk: if talks fail again, this positioning unwinds rapidly, creating forced selling that compounds any geopolitical deterioration. The cheap protection window from Monday’s brief is closed, but the risk-reward for conviction long positions improves on any such forced selling.

European Crisis: From Warning to Operations

Germany halving its GDP forecast to 0.5%, Lufthansa grounding planes, Nigerian carriers threatening to halt operations, and EU emergency jet fuel plans all confirm the European energy crisis is transitioning from forecast to operational impact. Tesco, Pernod Ricard, Hermes, and Kering all flagged Iran war impacts in earnings. US weapons delivery delays to Europe add a defense dimension to the European stress.

VGK options at 21.4% near-term (6.8pp above HV) continue pricing stress, though the intraday IV surge to 39.2% noted in yesterday’s world model has partially normalized. The IMF’s “guns vs. butter” framework is now directly observable: European governments facing energy crisis + defense underspending + fiscal constraints cannot address all three simultaneously.

Credit-Equity Divergence: Day 4 at Extreme

HYG OI P/C at 4.82 (up from 4.78 yesterday, 4.65 Monday, 3.89 pre-blockade). Four consecutive days of widening divergence. IG spreads at 1990s lows (Barron’s confirms) while HY faces $14B outflows and Citi forecasts rising defaults.

The private credit CDS launch provides the missing instrument for the divergence to resolve — institutional shorts now have a liquid way to express the credit deterioration thesis that HYG options have been signaling for weeks.

Continuing Themes

Iran blockade: Fully implemented per White House confirmation. Two tankers interdicted. No second round of talks scheduled despite diplomatic signals. Physical-futures crude divergence persists. Iran halted all petrochemical exports indefinitely.

AI hardware cycle: TSMC 58% profit growth + ASML guidance raise + AMD 41% rally = strongest week of validation since cycle began. CoreWeave $2.75B bond upsizing is the leveraged-edge yellow flag.

Consumer contraction: Record-low sentiment (47.6), housing sales -3.6%, mortgage rates rising 4th consecutive week, Spring housing market showing inventory but no price relief. AVOID all discretionary.

Defense: Dual-theater (Iran + Ukraine). US delaying European weapons deliveries accelerates domestic European procurement. LMT Q1 earnings imminent.

Fertilizer: Maximum conviction (14+ confirmations). India urea $1,000/ton. Iran petrochemical halt indefinite. 60% farmer financial deterioration.

Fed independence: Trump firing threat + Warsh confirmation uncertainty + Paulson warning = three institutional data points. Rate cut probability collapsed to 3-5%.

What to Watch

The options market is telling two sharply different stories: SPY at 12.8% IV with 0.93 P/C ratio reflects near-total crisis resolution, while HYG’s OI put/call ratio has climbed to 4.82 — its fourth consecutive day of widening — and its 6-month IV at 8.5% is nearly double the 1-month reading of 4.9%. The private credit CDS launch now provides the mechanism by which this divergence resolves, and history favors the credit signal roughly 70% of the time. Meanwhile, TLT sits at 9.8% near-term IV in clean contango, pricing zero risk of Treasury dysfunction against a 20-25% probability framework — the widest disconnect in any asset class. Full options positioning analysis, portfolio playbook, and risk scenario framework below for subscribers.

This publication is for informational and educational purposes only and does not constitute financial, investment, or trading advice. The analysis, opinions, and commentary presented here should not be interpreted as a recommendation to buy, sell, or hold any security. Always conduct your own research and consult a qualified financial advisor before making investment decisions. Past performance does not guarantee future results.