Physical Oil Markets Defy Ceasefire Rally as Credit Stress Converges Across Four Independent Channels

CPI at 3.3% confirms war-driven inflation is embedding while the options market reveals a stark contradiction: large-cap equities fully normalized but HYG, small-caps, and Japan still pricing crisis

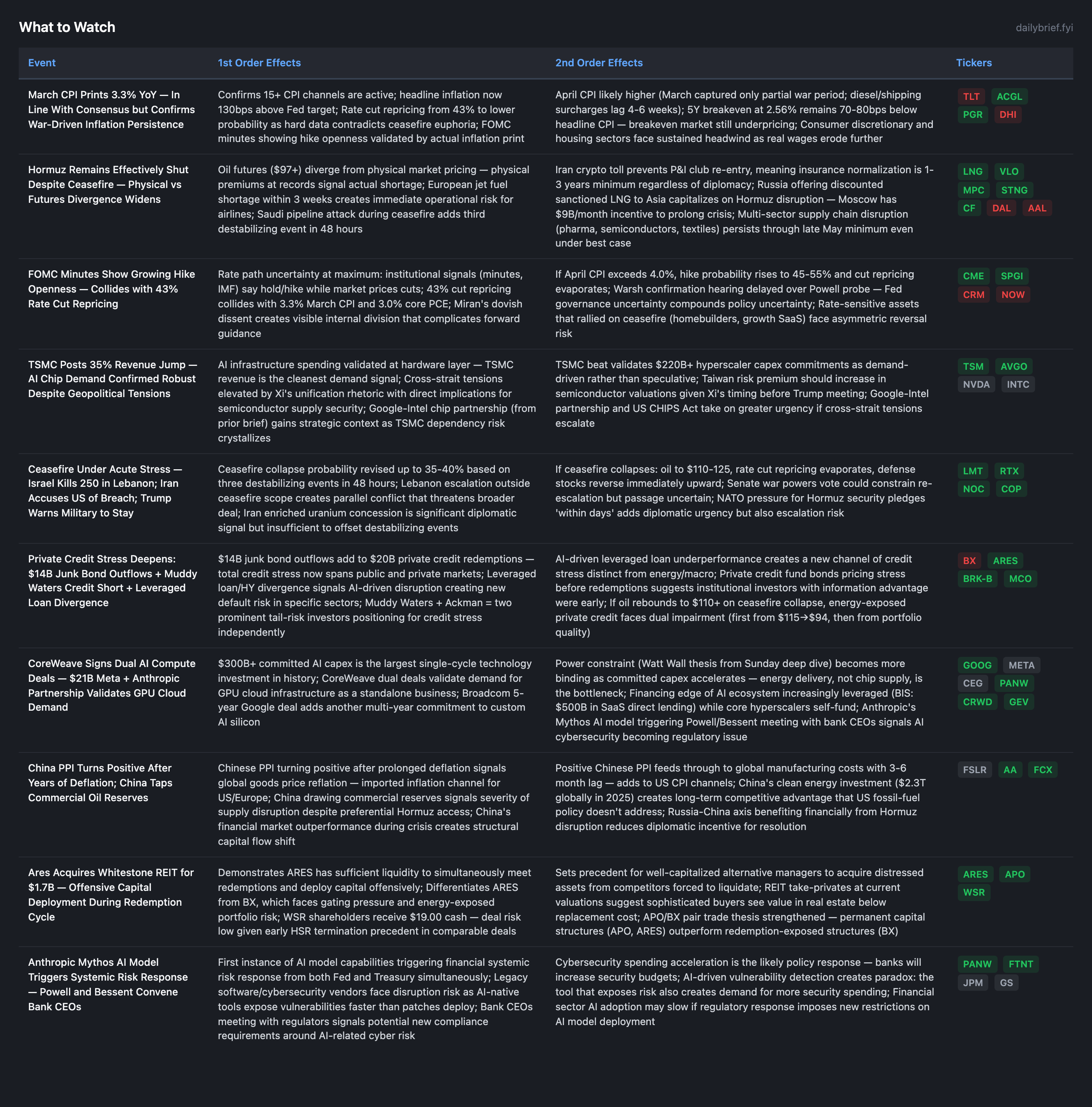

The ceasefire-driven market rally is being tested by hard data on two fronts simultaneously. March CPI printed at 3.3% YoY — in line with consensus but confirming that war-driven inflation is now embedded in official statistics. Core PCE was already at 3.0% in February, rising for a third consecutive month before the war’s energy spike hit. The physical reality is worse than the futures market suggests: European and African crude benchmarks hit records even as Brent futures fell, and European airports face jet fuel shortages within three weeks. The S&P 500 has nearly erased its Iran war losses, but this pricing reflects a resolution that has not occurred. Hormuz remains at 15 ships per day under an Iranian crypto-toll system, Saudi pipeline infrastructure was attacked during the ceasefire, Israel killed 250 in Lebanon outside the ceasefire’s scope, and Trump warned the military to stay near Iran. Three destabilizing events in 48 hours push ceasefire collapse probability to 35-40%.

The most consequential development since the prior brief is the convergence of four previously independent stress signals into a single credit narrative. The FT’s $14 billion in junk bond outflows now compounds the $20 billion in private credit redemptions. Bloomberg reports leveraged loans diverging from high-yield bonds due to AI-driven disruption of specific borrowers — a structural credit channel that operates independently of energy or macro stress. Muddy Waters is recommending bearish credit derivatives, citing AI labor displacement. Ackman is exploring a “complacency fund.” Private credit fund bonds had already fallen to year-lows before the redemption wave materialized. The HYG options market, while normalizing from its 33.3% crisis spike, still shows 24.6% near-term IV (19.8pp above HV) in steep backwardation with OI P/C at 3.89. The credit cascade thesis now has 17+ independent data points across public and private markets, institutional positioning, and hard flow data.

On the positive side, TSMC’s 35% revenue beat confirms AI chip demand remains robust, validating the $300B+ hyperscaler capex cycle. CoreWeave signed dual deals with Meta ($21B) and Anthropic. Broadcom’s 5-year Google custom chip agreement adds another multi-year commitment. The AI infrastructure buildout is generating measurable revenue at the hardware layer. Anthropic’s Mythos AI model triggering a joint Powell-Bessent meeting with bank CEOs introduces a genuinely novel signal: AI capabilities creating systemic financial risk that regulators feel compelled to address in real time. This is the first instance of an AI model’s capabilities — rather than its misuse — prompting a financial stability response.

March CPI: The 43% Cut Repricing Meets Hard Data

March CPI at 3.3% YoY is the first inflation reading that captures the initial weeks of the Iran conflict’s energy price impact. It is consistent with the world model’s framework but understates the forward trajectory because: (1) March only captured partial war-period energy passthrough — diesel and shipping surcharges lag 4-6 weeks; (2) core PCE at 3.0% in February was already rising before the war, indicating underlying inflation momentum independent of energy; (3) the 5Y breakeven at 2.56% (FRED, April 9 — unchanged) still prices inflation 70-80bps below headline CPI and approximately 120-180bps below the world model’s H2 2026 central case of 3.8-4.3%.

The FOMC minutes showing hike openness, the IMF stating “little room for cuts,” and the 3.3% CPI print form a three-source convergence against the 43% cut repricing. Governor Miran’s dovish dissent (calling for ~100bps of cuts) creates a visible internal divide, but the weight of institutional evidence (minutes, IMF, Musalem, Wells Fargo) firmly supports hold-or-hike. The market is pricing the ceasefire scenario; the Fed is pricing the inflation data.

April CPI will be more informative — it will capture a full month of war-period pricing including diesel passthrough, shipping surcharges, and food price increases from fertilizer disruption. I maintain: April CPI >3.5% at 80-90% probability; >4.0% at 55-65% probability. If >4.0%, the 43% cut repricing reverses completely.

Physical vs. Futures: The Market’s Supply Illusion

The most analytically important signal this week is the divergence between oil futures (declining on ceasefire) and physical crude benchmarks (hitting records). European and African crude at fresh record highs (Reuters, Tier 1) while Brent futures trade at $97 means the actual cost of delivered oil is higher than the financial market price suggests. This is a supply chain signal — physical buyers who need actual barrels are paying record prices because the barrels cannot get through Hormuz.

European airports facing jet fuel shortages within three weeks (FT, Tier 2) adds a time-specific constraint. If Hormuz doesn’t meaningfully reopen by late April, European airlines face operational curtailment — potential flight cancellations from physical fuel unavailability.

The Iran crypto-toll system (15 ships/day, crypto payments required) creates a structural barrier to normalization that persists through and beyond diplomatic efforts. No major P&I club can authorize crypto payments to a sanctioned entity. Insurance market closure means shipping normalization is 1-3 years minimum, not 6-8 weeks. The Hapag-Lloyd 6-8 week estimate assumes stable peace and insurance market re-entry, which the crypto requirement prevents.

Russia’s oil revenue doubling to $9B in April (Reuters, Tier 1) and Russia offering discounted sanctioned LNG to Asian buyers (Bloomberg, Tier 2) confirm that Moscow is financially incentivized to prolong disruption. Combined with China’s preferential Hormuz access via yuan payments and China drawing on commercial reserves (Reuters, Tier 1), two major powers benefit from the status quo. This reduces diplomatic pressure for full resolution.

Credit: Four Independent Stress Channels Converge

The credit thesis has evolved from a positioning signal to a multi-channel stress pattern. Four independent channels are now active simultaneously:

Private credit redemptions: $20B in Q1 2026 (FT) — operational, forcing liquidation or gating

Public credit outflows: $14B from junk bonds YTD (FT) — institutional risk appetite deteriorating

AI-driven leveraged loan divergence: Bloomberg reports leveraged loans underperforming HY due to AI disruption of specific borrowers — a structural default risk channel

Private credit fund bonds at year-lows: Reuters confirms bond prices were pricing stress before redemptions materialized — informed institutional investors were early

The AI-driven leveraged loan divergence is genuinely novel. Prior credit stress analysis focused on energy-exposed private credit and macro-driven spread widening. Bloomberg’s report that AI disruption is creating borrower-specific impairment in the leveraged loan market opens a fifth stress channel independent of energy or rates. Combined with Muddy Waters explicitly targeting corporate credit via AI labor displacement risk (MarketWatch), the credit cycle may have a technology-driven component that most models don’t capture.

HYG OI P/C at 3.89 (down from 4.10 yesterday) shows institutional hedges being modestly reduced but still heavily in place. The 24.6% near-term IV (19.8pp above 4.8% HV) in steep backwardation means the options market is still pricing a near-term credit event despite the ceasefire rally.

AI Infrastructure: $300B Capex Meets the Watt Wall

TSMC’s 35% revenue beat is the cleanest validation that AI hardware demand is real, not speculative. When the world’s foundational semiconductor manufacturer reports record revenue with 35% growth, the capex commitments from Meta ($21B CoreWeave + Richland Parish), Amazon ($200B), Google (Broadcom 5-year + Intel partnership), and others are demand-driven.

[SPOILER ALERT!] This Sunday deep dive’s “Watt Wall thesis” gains immediate relevance: $300B in committed capex creates power demand that the grid cannot serve on the AI timetable. GE Vernova’s 83 GW turbine backlog, transformer lead times of 1-4 years, and PJM capacity auction clearing prices (from $29 to $333/MW-day) are the binding constraints. TSMC can make the chips; the constraint is whether the power system can run them.

The Anthropic Mythos meeting is a genuinely novel development. This is the first time an AI model’s capabilities (detecting decades-old financial infrastructure vulnerabilities) triggered a systemic risk response from both the Fed and Treasury. It is distinct from AI safety debates or AI ethics discussions — it is a concrete, operational financial stability concern. The policy response will likely be increased cybersecurity spending mandates for financial institutions, creating direct revenue for enterprise security platforms (PANW, CRWD, FTNT).

Constellation Brands: Consumer Weakness Confirmed

STZ withdrawing fiscal 2028 guidance and reporting subdued demand across categories (CNBC) confirms the consumer contraction thesis. It reflects the same consumer stress that produced declining mortgage demand (-40% refi), rising underwater auto loans (30.5%), and mortgage rates above 6.5% suppressing the spring housing season. With March CPI at 3.3% and April likely higher, real wage growth is negative for most consumers. The consumer discretionary AVOID thesis (4th consecutive calibration) is reinforced.

Cross-Strait Tensions: The Other Chokepoint

Xi Jinping hosting Taiwan’s opposition leader and calling unification “inevitable” ahead of a May Trump meeting (FT, CNBC — Tier 1/2, dual-sourced) introduces a second geopolitical chokepoint scenario. TSMC’s centrality to the AI buildout is confirmed by its revenue results. The FT’s analysis that Taiwan’s semiconductor chokehold poses existential risk to the AI boom is the strategic frame: Hormuz controls 20% of global oil; Taiwan controls 90%+ of leading-edge chips. If both chokepoints come under simultaneous pressure, the AI infrastructure thesis and the energy thesis collide.

Google-Intel chip partnership gains additional strategic context — it is a supply-chain diversification play that reduces single-point-of-failure risk on TSMC/Taiwan.

What to Watch

The options market is sending a signal that demands attention: SPY implied volatility has fully normalized to 15.4% — making equity downside protection historically cheap — while HYG near-term IV re-steepened to 24.6% (19.8pp above realized) with an OI put/call ratio of 3.89, and EWJ has escalated for four consecutive sessions to 59.9% IV, the highest stress reading in the entire dataset. When equity and credit markets disagree this sharply, credit has been right approximately 70% of the time historically. The premium section below breaks down exactly how the options term structures are pricing specific event windows, which hedges are actionable at current vol levels, and how to position across the six risk scenarios — from ceasefire collapse (35-40%) to the 50-55% probability equity correction from credit contagion that current SPY pricing leaves almost entirely unhedged.

Full options positioning analysis, portfolio playbook, and risk scenario framework below for subscribers.

This publication is for informational and educational purposes only and does not constitute financial, investment, or trading advice. The analysis, opinions, and commentary presented here should not be interpreted as a recommendation to buy, sell, or hold any security. Always conduct your own research and consult a qualified financial advisor before making investment decisions. Past performance does not guarantee future results.