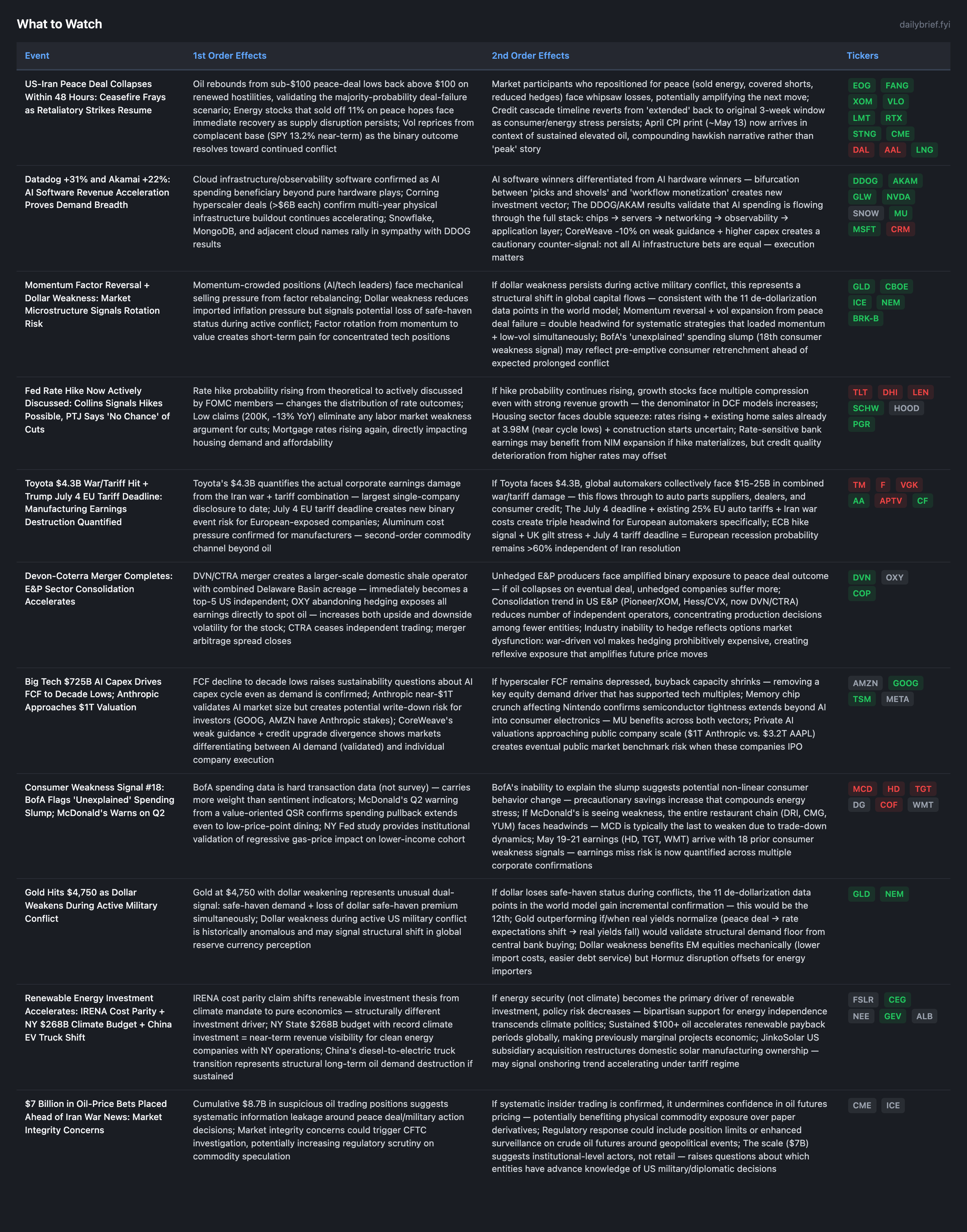

Peace Deal Collapses as Iran Seizes Tanker and US Strikes Ports — Oil Reclaims $100

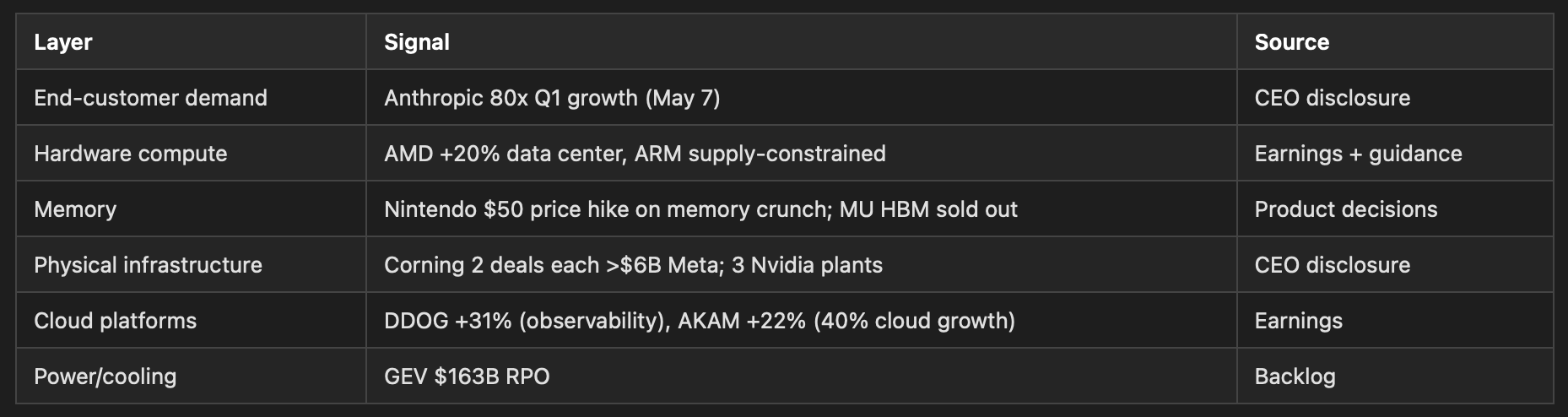

AI infrastructure receives its most comprehensive demand validation yet as Datadog surges 31%, Corning reveals two hyperscaler deals exceeding $6B each, and ARM confirms supply constraints

The 48-hour peace deal window has resolved toward the collapse scenario identified as 40-50% probability in the May 6 brief. Iran seized a tanker, the US struck Iranian ports, and hostilities resumed within the binary timeframe. Oil rebounded above $100 after briefly touching $96.75 on deal hopes. The peace framework has not formally died — Trump still claims the ceasefire holds — but operational reality (tanker seizures, port strikes, Navy under fire) confirms reversion to the conflict state.

Simultaneously, the April jobs report beat expectations at 115K (vs 55K consensus), eliminating any near-term Fed easing catalyst. Bank of America disclosed an unexplained consumer spending slump, providing the 19th consumer weakness signal independent of deal outcome. And the AI infrastructure thesis received its most comprehensive validation yet: Datadog +31%, Akamai +22%, ARM supply-constrained on AI chips, Corning CEO disclosing two hyperscaler deals each exceeding $6B, and Nintendo hiking Switch 2 prices $50 on memory constraints.

Deal Collapse Confirmed by Operational Reality

Within the 48-hour window defined on May 6, the peace deal framework has functionally collapsed despite no formal declaration. The evidence is unambiguous:

Iran seized the tanker Ocean Koi in the Gulf of Oman (Reuters Tier 1)

China confirmed a separate tanker attack in Hormuz (Reuters Tier 1)

US Navy destroyers came under Iranian missile fire (Reuters Tier 1)

US struck Iranian ports including Qeshm and Bandar Abbas (Reuters Tier 1)

CMA CGM vessel struck in Strait with crew injuries (from May 6 data, now confirmed as pattern)

Trump claiming the ceasefire “still holds” while his military strikes Iranian ports fits the 0-for-11 pattern of rhetoric diverging from reality.

Oil’s 12-13% crash on deal hopes has partially reversed — Brent back above $100 on renewed clashes. The NACHO trade (positioning for prolonged Hormuz disruption) is validated by Maersk’s explicit warning that “energy crunch will persist even if a peace deal is struck.” Physical infrastructure damage ($58B) and supply chain rerouting don’t reverse on diplomatic announcements.

Updated probability distribution: diplomatic resolution probability reverts from 20-30% back to 10-15%. The “deal collapses, reversion to prior state” scenario has materialized. Next iteration of diplomatic talks requires new credibility-building given this failure.

$7 Billion Pre-Positioned Oil Bets: Market Integrity Signal

Reuters exclusive reporting that $7 billion in oil bets were placed ahead of Iran war developments represents a genuinely new signal outside existing themes. At minimum, this indicates:

Political intelligence networks are trading at scale on geopolitical information before public dissemination

The oil market’s price discovery is partially compromised by asymmetric information

Regulatory scrutiny of energy futures markets likely increases

The size ($7B) suggests institutional actors, not retail. Combined with the UAE covert tanker movements reported in the May 7 brief, the oil market contains significant hidden information flows that make surface-level price action an unreliable indicator of physical supply/demand conditions.

For portfolio positioning: this reinforces the structural advantage of exchange operators (CME, ICE) who benefit from activity regardless of direction or information asymmetry, and underlines why vol-selling in oil is dangerous despite apparent mean-reversion tendencies.

Consumer Spending Collapse: BofA’s “Unexplained” Data Is Actually Explained

Bank of America’s internal card data showing a sudden consumer spending slump is framed as “unexplained,” but the explanatory framework is established: savings rate at 3.6% (depleted), gas above $4.50/gal (behavioral threshold approaching), mortgage rates near 7.5% (housing locked), and cumulative lagged effects of 69 days of war-driven inflation. The spending drop is the predictable consequence of every consumer stress signal converging.

This is the 19th independent consumer weakness data point: Spirit shutdown, WHR recession-level, MCD Q2 warning, Michigan 53.3, NY Fed lower-income study, restaurant sales declining, and now BofA real-time card data showing actual spending contraction. The May 19-21 earnings cluster (HD, TGT, WMT) faces the most hostile consumer backdrop in this cycle.

Critical distinction: the March retail sales headline (+1.7%) was driven by gasoline receipts (price inflation, not volume). Stripping gas stations, real consumer spending was likely flat or declining. The BofA card data confirms this interpretation.

AI Demand Validation Reaches Comprehensive Threshold

Today’s events complete the most comprehensive AI demand validation across every layer of the stack:

The capital allocation decisions (Corning building plants, Nintendo paying premiums, ARM admitting constraints) carry more weight than any analyst estimate per established lessons.

Momentum Factor Reversal: Potential Regime Signal

MarketWatch reports one of the biggest momentum reversals in five years. Momentum reversals of this magnitude have historically preceded 2-4 weeks of factor rotation. In the current context, this could mean:

AI/tech momentum names (which have driven indices to ATH) face near-term underperformance

Value/quality names (BRK-B, insurance, exchanges) outperform

The reversal coincides with peace deal failure → growth leaders may face double headwind of factor rotation + rising rates

One data point — insufficient for conviction — but directionally consistent with the portfolio tilt toward defensive quality (insurance, exchanges, domestic E&P) over growth momentum.

Oil Market: Reverts to $100-125 Range with Extended Duration

Oil’s intra-day round trip ($125 → $96.75 → $100+) within 48 hours confirms extreme binary sensitivity to diplomatic headlines. Maersk’s explicit statement that supply chains remain disrupted regardless of peace provides the physical market anchor. Updated base case: $100-125 for the foreseeable future, with spikes above $130 on escalation events and dips below $100 only on renewed credible diplomatic signals.

OXY scrapping hedges entirely is the corporate capital allocation signal that prices stay elevated. Per analyst lessons: “Corporate capital allocation signals outperform analyst forecasts for medium-term commodity price direction.”

Credit Market: Timeline Compresses Back to 3-4 Weeks

Peace deal failure means: consumer stress reintensifies (no gas price relief), banks can’t relax energy-related lending concerns, and the credit tightening impulse resumes. HYG OI P/C at 5.31 — unchanged from the all-time high despite the equity rally. BDC NAV marks due this week remain the immediate catalyst. The 1-week HYG put skew spiked to 41.9% — the highest level in our entire reporting period, exceeding the 36% that preceded the May 4 spike.

UK Gilt Pressure + ECB Hawkishness: European Multi-Front Crisis Deepens

VGK 1-week IV spiked to 33.5% (+18.1pp vs 15.3% HV) — the most extreme reading for any major equity ETF. This reflects: UK political instability (Starmer election losses → gilt selling), ECB hawkish signal (Schnabel), Trump July 4 EU tariff deadline, and sustained energy costs from Hormuz. The European crisis is now three-front: energy, tariffs, and political stability.

What to Watch

Full options positioning analysis, portfolio playbook, and risk scenario framework below for subscribers.

This publication is for informational and educational purposes only and does not constitute financial, investment, or trading advice. The analysis, opinions, and commentary presented here should not be interpreted as a recommendation to buy, sell, or hold any security. Always conduct your own research and consult a qualified financial advisor before making investment decisions. Past performance does not guarantee future results.