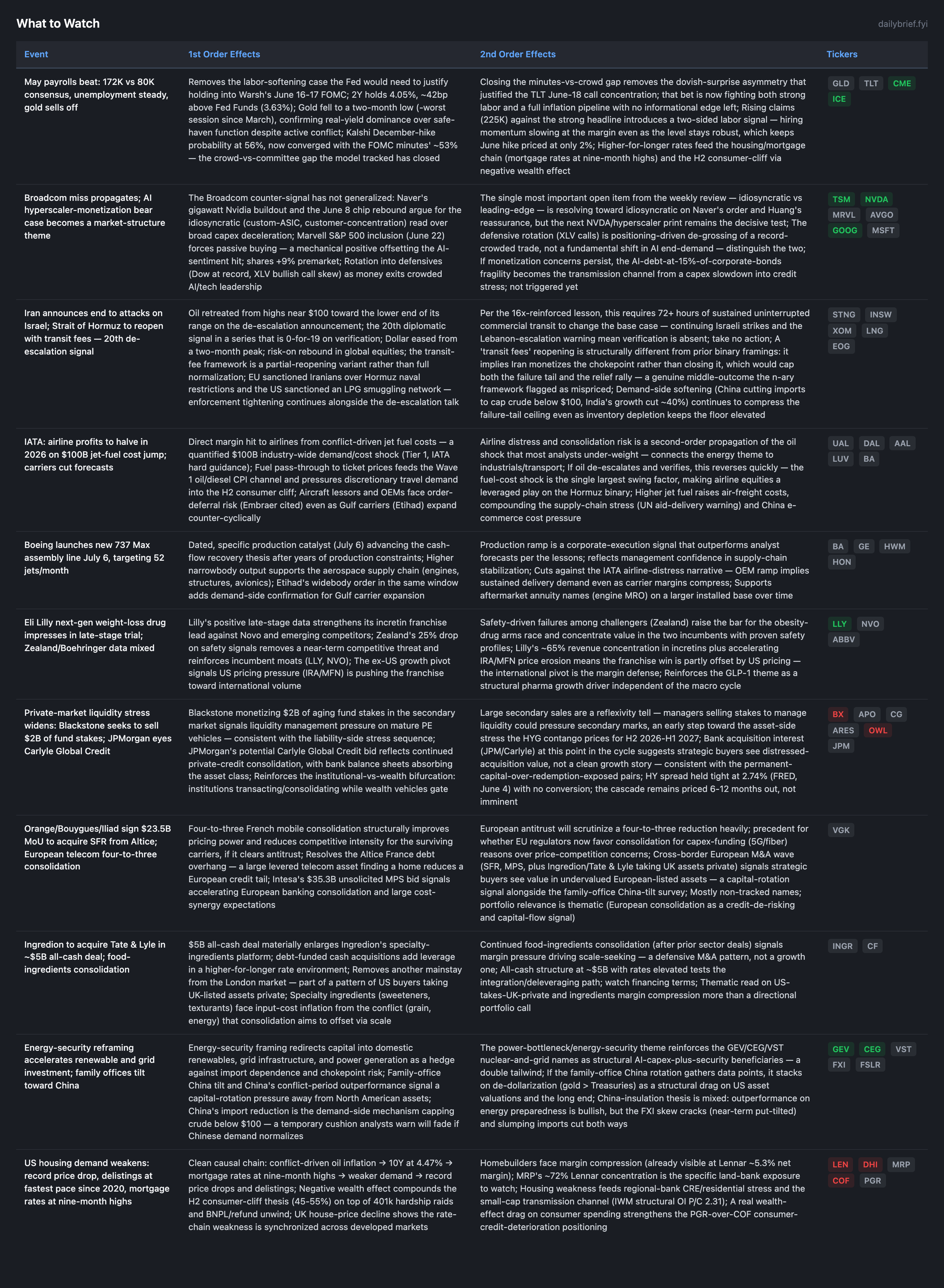

Payrolls Beat Slams the Door on the Dovish-Warsh Trade

A custom-ASIC scare resolves toward idiosyncratic as Nvidia reassures, while Iran's 20th de-escalation signal arrives with a transit-fee twist that caps both tails.

Two things shifted decisively since the weekly review. First, the May payrolls print resolved the labor question toward the hawks: 172K jobs versus an 80K consensus (FRED confirms +172K to 159,001K nonfarm), unemployment steady at 4.3%, and the Kalshi December-hike probability now at 56%, fully converged with the FOMC minutes’ ~53%. The minutes-vs-crowd gap that the model tracked for weeks has closed, which removes the dovish-surprise asymmetry that justified the TLT June-18 call concentration. The dovish-Warsh bet now fights strong labor and a full inflation pipeline, and its own informational edge is gone. Gold’s worst session since March confirmed the real-yield channel dominates its safe-haven function even with an active Gulf conflict.

Second, the Broadcom counter-signal is resolving toward idiosyncratic rather than leading-edge. Naver’s gigawatt-scale Nvidia data-center order, Huang’s investor reassurance, and the June 8 chip rebound (Nasdaq futures +1%) all argue the custom-ASIC weakness was customer-concentration timing, not broad AI-capex deceleration. The single most important open item from the weekly review is provisionally answered in favor of the narrow read, with the next NVDA/hyperscaler print as the decisive test. The Hormuz binary produced its 20th unverified signal (Iran declared an end to attacks on Israel, with a transit-fee reopening framework), and continuing Israeli strikes plus a Lebanon-escalation warning mean the 0-for-19 verification discipline holds with no position change. The new wrinkle is the transit-fee structure: a middle outcome that monetizes the chokepoint rather than closing it, capping both tails. New today: IATA’s $100B jet-fuel shock halving airline profits, and a widening private-market liquidity-management signal (Blackstone selling $2B of fund stakes).

IATA: $100B Jet-Fuel Shock to Halve 2026 Airline Profits

IATA projects 2026 airline profits roughly halving on a ~$100B jet-fuel cost increase from the Iran conflict, warning of potential carrier failures and consolidation. This is hard industry guidance that quantifies a second-order propagation of the oil shock the energy theme had not yet connected to transport equities.

The mechanism is direct: conflict-driven crude keeps jet fuel elevated, fuel is ~25-30% of airline operating cost, and the pass-through to ticket prices both compresses margins and dampens discretionary travel demand into the H2 consumer cliff. The leveraged read is that airline equities are now a two-sided play on the Hormuz binary: if oil de-escalates and verifies, the fuel shock reverses quickly and the profit-halving guidance unwinds; if the conflict grinds on or the failure tail ($150-160) materializes, carrier distress and consolidation accelerate. Etihad’s counter-cyclical widebody order and Boeing’s 737 Max line ramp (52/month from July 6) cut against the distress narrative on the OEM side, implying sustained delivery demand even as carrier margins compress.

This is a single industry-level data point on a specific 2026 forecast cut, so I am keeping airline names (UAL, DAL, AAL, LUV) neutral and monitoring rather than establishing bearish conviction. AAL, the most balance-sheet-leveraged major, is where IATA’s failure warning bites hardest. This confirms the oil-shock-propagation thesis rather than supplying a directional equity call, consistent with the lesson that second-order supply disruptions can exceed first-order effects.

Private-Market Liquidity Management Widens: Blackstone Sells $2B of Fund Stakes

Blackstone is looking to sell ~$2B of stakes in private investment funds in one of the largest secondary deals of its kind (FT, Tier 2), and JPMorgan is reportedly weighing a bid for Carlyle’s Global Credit business if it goes up for sale. These follow the named-fund gating sequence (Cliffwater, Partners Group, Blackstone’s flagship) the prior briefs documented.

The new information is the move from liability-side stress (gating redemptions) to active liquidity management on the asset side (selling stakes into the secondary market). Large secondary sales are the reflexivity tell the weekly review flagged: managers monetizing aging stakes to manage liquidity can pressure secondary marks, the first step toward the NAV-markdown/spread-widening stage the HYG contango prices for H2 2026-H1 2027. The HY spread held tight at 2.74% (FRED, June 4) with no conversion, so the cascade remains priced 6-12 months out, not imminent. JPMorgan’s potential Carlyle Global Credit bid reflects strategic buyers seeing distressed-acquisition value at this point in the cycle, consistent with the permanent-capital-over-redemption-exposed pairs (BX bearish, APO bullish-lean; OWL bearish, ARES bullish-lean). I am keeping CG neutral despite its short leg in RNR-vs-CG, because a take-out report is event-specific and not a thesis change.

What to Watch

Developing Themes

Broadcom Question Resolving Toward Idiosyncratic

The chip-rebound and reassurance signals (covered in the Executive Summary) argue the AVGO miss was custom-ASIC customer-concentration timing rather than broad capex deceleration. The defensive rotation into healthcare (Dow at a record, XLV bullish call skew) is positioning-driven de-grossing of a record-crowded AI trade, not a fundamental shift in end-demand; distinguish the two. The clean expressions are unchanged: TSM (diversified across the silicon complex), GOOG and MSFT (cloud layer, demand-backed capex), with integrators conviction-neutral. Marvell’s S&P 500 inclusion (June 22) is a mechanical passive-buying catalyst (+9% premarket) that does not change the underlying lumpy-ASIC-order fundamentals. The next NVDA/hyperscaler print is the decisive test; the burden has shifted toward the narrow read, but it is not closed.

Rates: Payrolls Close the Crowd-vs-Committee Gap

The June hike is still priced at 2%, so the binary is December and the tone of Warsh’s June 16-17 inaugural FOMC guidance. Rising initial claims (225K, a four-month high per FRED) against the strong headline is the one two-sided element: hiring momentum slowing at the margin even as the level stays robust. Do not pre-position; let exchanges (CME, ICE) carry the vol. The global stance stays synchronized hawkish, though the Bank of Canada is expected to hold through 2026 (treating conflict inflation as temporary) and the BoE’s Taylor signaled rates on hold barring a severe downturn, two central banks resisting the tightening pull, partial offsets to the synchronized-hawkish read.

Hormuz: 20th Signal, Now a Transit-Fee Middle Outcome

The 20th diplomatic signal (covered in the Executive Summary) sits in a series 0-for-19 on verification. Israeli strikes reportedly continued, Iran warned of Lebanon escalation, and Trump won’t unfreeze Iranian assets pre-deal; verification (72+ hours sustained transit) is absent, take no action. The transit-fee structure is a middle outcome the n-ary framework flagged as structurally mispriced, and it caps both the failure tail and the relief rally. Demand-side softening (China capping crude below $100, India’s growth cut ~40%) continues compressing the failure-tail ceiling while inventory depletion keeps the floor elevated. Hold STNG/INSW and LNG; energy overweight maintained, no add (energy BUYs -1.58% across 142 calls per calibration). The SPR refill plan (40M barrels post-war) is future crude demand and a policy bet on resolution.

Housing Demand Deteriorates via the Rate Chain

Home values posted their largest drop in nearly a decade, delistings hit the fastest pace since 2020, and mortgage rates reached nine-month highs (covered in the prior brief, now reinforced with the price-drop data point). The negative wealth effect compounds the H2 consumer-cliff thesis on top of 401k raids and the BNPL unwind. UK house prices also fell unexpectedly, showing the rate-chain weakness is synchronized across developed markets. Homebuilders (LEN, DHI) trade on this already; Consumer Discretionary is BUY-prohibited, so read misses as confirmation. Reinforces PGR-over-COF on consumer-credit deterioration.

Continuing Themes

Small-cap: IWM OI P/C at 2.31 (highest among US-equity ETFs), structural put dominance intact despite near-term IV normalization. July 2 $260 put thesis live. Continue to avoid.

Defense: Multi-front demand (Middle East, NATO/Russia, Israel-Lebanon) structurally confirmed; overweight maintained (RTX, NOC, GD, LMT, LHX). No material change.

Software bifurcation: Pair trades CORE (GOOG vs INTU, TSM vs WDAY, PANW vs CRM). The professional-services-led JOLTS hiring breadth still sits uneasily against the white-collar-displacement thesis; unresolved.

GLP-1/obesity: Lilly’s positive next-gen data and Zealand’s safety stumble concentrate value in the incumbents (LLY, NVO). LLY BUY (7.2) held; the ex-US pivot is margin defense against IRA/MFN erosion.

Crypto: CLARITY Act advancing (medium-term positive); no portfolio-relevant change.

CF Industries: No new data point; tactical HOLD (6.0). Clean exit if Hormuz physically reopens.

The options tape is telling a more precise story than the headline vol spike suggests: SPY near-term IV at 33.2% against 12.1% HV looks rich, but the >10% decline probability is only 1.4% — event-hedging into SpaceX/FOMC, not durable stress. The durable signals sit elsewhere — EEM’s +36.1pp near-term spread and 2.1% tail probability mark the cleanest Hormuz-plus-hawkish expression, IWM’s 2.31 OI P/C survives another vol cycle, and TLT’s 7.1% IV with a call-heavy 0.79 OI P/C shows the dovish-Warsh bet stranded without an edge after payrolls. The portfolio playbook below maps which conviction names to hold versus where to stay neutral, and the risk framework runs the scenarios that would force a reassessment — from a generalized Broadcom miss to a private-credit cascade pulled forward off the 2.74% spread.

Full options positioning analysis, portfolio playbook, and risk scenario framework below for subscribers.

This publication is for informational and educational purposes only and does not constitute financial, investment, or trading advice. The analysis, opinions, and commentary presented here should not be interpreted as a recommendation to buy, sell, or hold any security. Always conduct your own research and consult a qualified financial advisor before making investment decisions. Past performance does not guarantee future results.