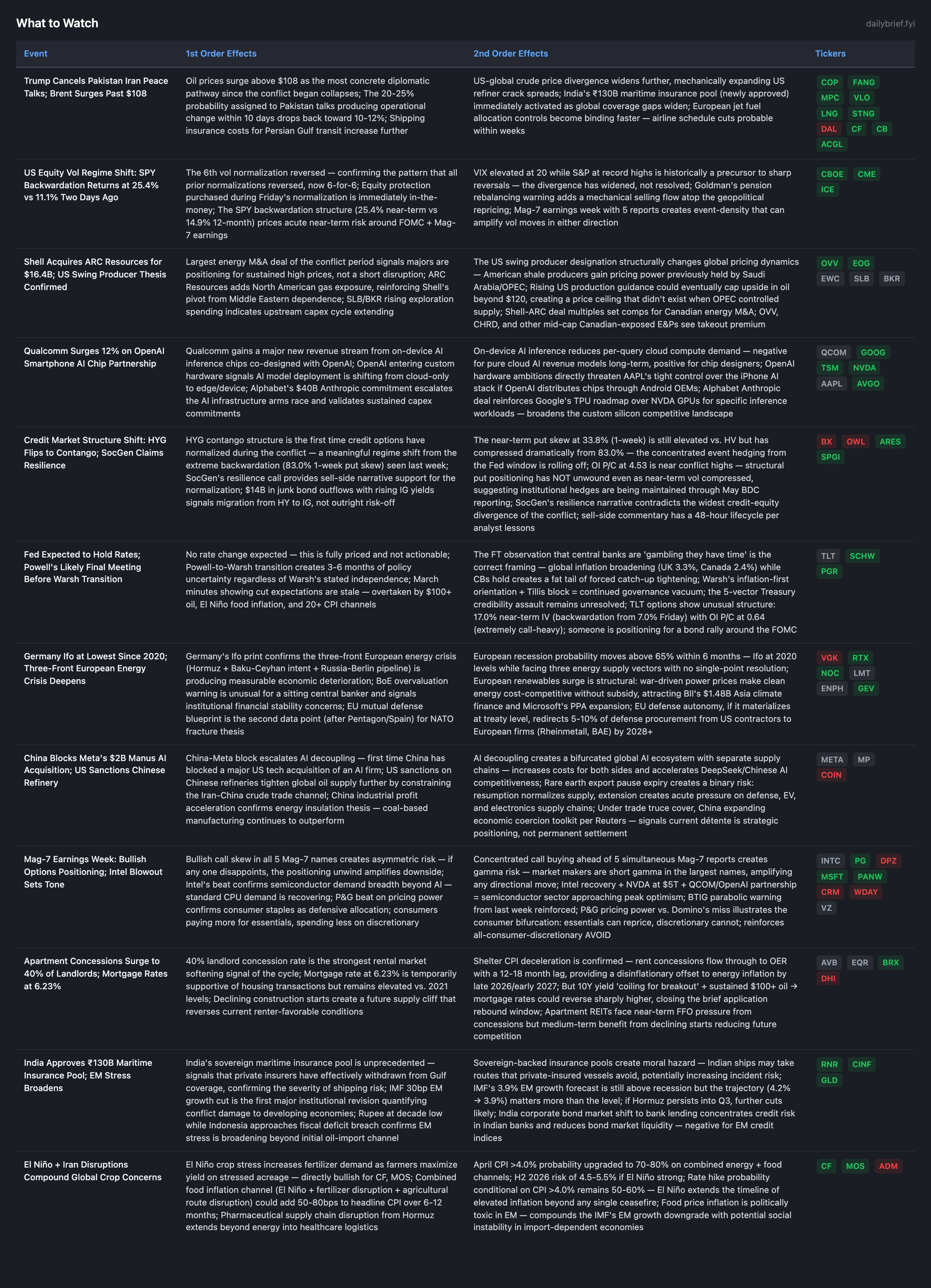

Pakistan Talks Collapse Resets Diplomatic Odds as Vol Regime Shift Hits 6-for-6 Reversal Pattern

Germany's Ifo at 2020 lows confirms European recession path while India's sovereign maritime insurance pool signals private coverage has effectively withdrawn from Gulf shipping

Two material shifts since Friday’s brief. First, the diplomatic probability upgrade has reversed: Trump canceled the Pakistan negotiator trip, collapsing the most specific diplomatic framework of the conflict. The 20-25% probability assigned to operational change within 10 days drops back to 10-12%. Brent surged past $108. Second, the equity options market underwent the sharpest vol regime shift of the conflict — SPY near-term IV jumped from 11.1% (Friday) to 25.4% (Sunday), confirming for the 6th consecutive time that vol normalizations during active military conflicts reverse.

Germany’s Ifo at 2020 lows confirms the European recession path. India created a sovereign maritime insurance pool — an admission that private coverage has effectively withdrawn from Gulf shipping. China blocked Meta’s $2B AI acquisition while the US sanctioned a Chinese refinery, compressing the US-China technology and energy relationship simultaneously. Mag-7 earnings week with bullish options positioning creates gamma risk in the largest names.

Pakistan Talks Collapse: Diplomatic Probability Reset

Trump’s cancellation of the Witkoff/Kushner Pakistan trip is the single most important event of the weekend. Friday’s brief upgraded diplomatic probability to 20-25% based on the specificity of the framework — named envoys, specific venue, third-party verification, Iran’s stated willingness to make an offer. The cancellation eliminates this upgrade. We are back to 0-for-10 on diplomatic signals producing operational change.

Brent at $108 with only five ships transiting Hormuz daily means the base case has shifted further toward sustained disruption. Iran’s Hormuz reopening proposal remains on the table but without a US negotiating counterparty. Oil path probabilities: sustained blockade with periodic openings 45-50% (up from 40-45%), US-Iran naval confrontation within 7 days 18-22% (the tanker interceptions in Asian waters are expanding the contact surface), extended framework deal 8-10% (down from 10-12%), Pakistan-type talks producing change 8-10% (down from 20-25%).

The second-order consequence that matters most: US oil executives now expect domestic crude output to rise. Reuters confirms America has become OPEC’s de facto swing producer. American shale responding to sustained >$100 prices while Middle Eastern supply is constrained has no post-1970s precedent. The beneficiaries extend beyond producers (COP, FANG, EOG) to the entire domestic energy supply chain: refiners (MPC, VLO) processing cheaper domestic crude at globally elevated product prices, midstream (KMI, WMB, TRGP) handling incremental volumes, and LNG exporters (LNG) capturing European desperation premiums.

Vol Regime Shift: 6-for-6 Normalization Reversal Pattern

SPY near-term IV surged from 11.1% to 25.4% in 48 hours — from 1.4pp below HV to 12.9pp above. QQQ moved from 14.1% to 32.5%. IWM hit 40.0%. The magnitude validates two lessons simultaneously: (1) vol normalization during active conflicts is a mispricing, and (2) the window for buying protection closes in hours, not days. Anyone who followed Friday’s recommendation to buy SPY protection saw immediate gains.

The reversal was driven by the Pakistan cancellation, but the vol structure reveals additional risk. VIX at 20 while S&P 500 sits at record highs is historically associated with 2-4 week reversals (2018 and 2020 provide the closest analogs). Goldman’s pension rebalancing warning adds a mechanical selling flow. Five Mag-7 reports this week with concentrated bullish call positioning creates gamma risk — market makers short gamma in the largest names amplify any directional move. The setup for a 3-5% drawdown within 2 weeks is the most favorable since the conflict began.

Shell-ARC $16.4B: Strategic Energy M&A Validates Sustained High Prices

Shell acquiring ARC Resources for $16.4B is the largest energy acquisition of the conflict period. A major integrated oil company deploying capital at current valuations to add 370K boe/d of North American production is a bet that $100+ oil persists long enough to earn adequate returns on a multi-decade asset. Shell’s willingness to pay this premium contradicts the ceasefire-resolution scenario where oil normalizes to $85-90.

For the tracked universe, the deal sets acquisition multiples for Canadian-exposed E&Ps. OVV, CHRD, and other mid-cap names with similar production profiles now carry takeout premiums. The US swing producer thesis means domestic energy is now strategic infrastructure, not cyclical commodity exposure. Position accordingly.

China Blocks Meta AI Acquisition: Decoupling Accelerates

China’s block of Meta’s $2B Manus acquisition represents the first Chinese regulatory intervention against a major US tech company acquiring an AI firm. Combined with US sanctions on a Chinese teapot refinery and the $344M crypto wallet freeze, the US-China relationship is being compressed on both the technology and energy axes simultaneously.

The AI decoupling creates a bifurcated global AI ecosystem. DeepSeek’s new flagship model release — one year after its R1 model triggered a trillion-dollar market selloff — keeps Chinese AI competitive pressure alive. For portfolio positioning, this reinforces the NVDA/TSM/AVGO thesis (hardware layer benefits from both ecosystems needing foundry capacity) while creating downside risk for companies dependent on cross-border AI talent (META’s acquisition pipeline constrained, US AI labs losing access to certain Chinese research capabilities).

India’s Sovereign Maritime Insurance Pool: Private Coverage Has Withdrawn

India’s ₹130B government-guaranteed maritime insurance facility is a first-of-its-kind response confirming the private maritime insurance market has effectively priced Gulf shipping as uninsurable. This is the strongest bottom-up confirmation of the Hormuz disruption’s severity.

This is the 4th independent data point confirming the marine/war risk insurance hard market: (1) Beazley’s $1B facility, (2) Lloyd’s rate increases, (3) India’s sovereign pool, (4) Turkey’s demining offer (implying mine risk is real). RNR and ACGL are the direct beneficiaries through reinsurance pricing power. Any normalization of Hormuz shipping requires not just military de-escalation but insurance market recovery, which operates on 6-12 month cycles even after military risk subsides.

What to Watch

The options market is sending signals that deserve close attention this week. SPY’s 48-hour IV surge from 11.1% to 25.4% has made new protection expensive, but TLT’s unusual structure — near-term IV jumping to 17.0% from 7.0% with an extremely call-heavy OI P/C of 0.64 — suggests institutional money is positioning for a flight-to-quality event around FOMC, potentially triggered by Mag-7 earnings disappointment. Meanwhile, HYG’s OI P/C at 4.53 near conflict highs confirms structural put positioning has not unwound despite the surface-level contango normalization, and the 60-70% credit event probability from May BDC NAV marks remains the most underappreciated risk in the market. Full options positioning analysis, portfolio playbook, and risk scenario framework below for subscribers.

This publication is for informational and educational purposes only and does not constitute financial, investment, or trading advice. The analysis, opinions, and commentary presented here should not be interpreted as a recommendation to buy, sell, or hold any security. Always conduct your own research and consult a qualified financial advisor before making investment decisions. Past performance does not guarantee future results.