Oil Becomes Deliberate Policy as Brent Hits $125; Fed Fractures at 34-Year High Dissent

Big Tech's $725B AI capex commitment reveals winners and losers — Google outperforms while Meta stumbles and Microsoft's $190B spend lacks revenue attribution.

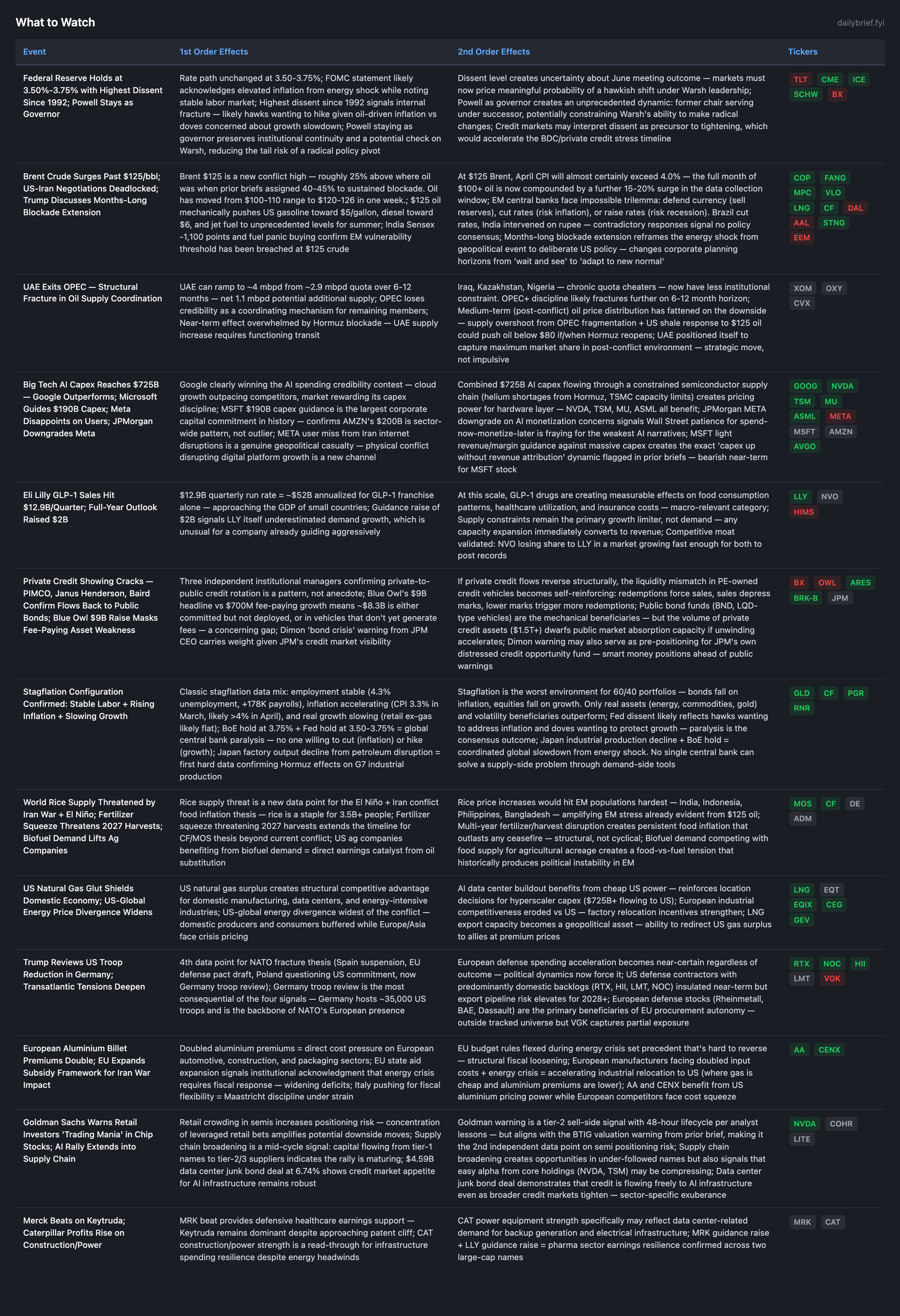

Three material shifts since yesterday’s brief. First, Brent crude breached $125/bbl on confirmed US-Iran negotiation deadlock AND Trump explicitly discussing a months-long blockade extension with oil executives. This converts the energy shock from geopolitical uncertainty to deliberate US policy, changing corporate planning horizons. Second, the Fed held with the highest dissent since 1992. Powell’s decision to stay as governor creates an unprecedented dynamic: former chair serving under Warsh, constraining radical policy shifts but signaling institutional concern about the direction of travel. Third, Big Tech earnings revealed a $725B aggregate AI capex commitment, with Google winning the spending-credibility contest while Meta was downgraded by JPMorgan and Microsoft guided $190B capex against light revenue.

The macro configuration has deteriorated: Brent $125, 10Y at 4.41% (second-highest of 2026), 5Y breakeven at 2.67% (rising), Michigan sentiment at 53.3, and the FOMC internally fractured. The stagflation thesis has graduated from risk scenario to operating reality.

Brent at $125: From Geopolitical Shock to Deliberate Policy

Trump met with oil executives to discuss a months-long blockade extension. Prior briefs treated the Hormuz disruption as a military/geopolitical event with uncertain duration. Trump’s meeting reframes it as a deliberate policy choice with an explicitly extended timeline. Companies can no longer hedge on near-term resolution.

The data confirms: oil surged 6% on April 29 (Brent approaching $120), then pushed to $125-126 on April 30. The US military commander is reportedly briefing Trump on new military options — escalation not de-escalation. The Hormuz shipping “trickle” continues with the US seeking an international coalition to reopen passage, implying it currently cannot be reopened unilaterally.

India provides the EM vulnerability confirmation: Sensex dropped 1,100+ points, the government moved to contain fuel panic buying, and the sovereign maritime insurance pool (₹130B) is now operational but insufficient to restore normal shipping volumes. At $125 crude, India’s current account deficit deteriorates by roughly $40-50B annually, consuming its reserve buffer within 12-18 months.

Oil path probabilities shift: sustained blockade with periodic openings 50-55% (up from 45-50%), months-long deliberate extension 20-25% (new scenario, carved from diplomatic resolution), US-Iran escalation 15-20%, diplomatic resolution 5-8% (lowest of the conflict).

For the CPI model: a full April at $100+ oil compounded by the surge to $125 in the final days locks in April CPI >4.0% with >80% probability. The 5Y breakeven at 2.67% (rising) confirms the market is repricing inflation expectations structurally higher.

FOMC Dissent at 34-Year High: The Institutional Signal

The hold at 3.50-3.75% was fully expected. The dissent level is the news. At least 2-3 governors broke from consensus — likely a mix of hawks wanting to respond to $125 oil-driven inflation and doves concerned about growth deceleration. The FOMC statement language will matter for parsing this, but the structural implication is clear: the June meeting under Warsh will face a pre-divided committee, making the first Warsh-chaired decision unpredictable.

Powell staying as governor is the under-appreciated development. A former chair has never served as a regular governor under their successor. Powell’s continued presence means Warsh cannot easily pack the committee with sympathetic voices — Powell’s institutional knowledge and relationship with staff creates a check on radical departures from the framework. This reduces the tail risk of a surprise hike at the June meeting from perhaps 20% to 12-15%, while increasing the probability of continued paralysis.

Rate path: hold at 3.50-3.75% through June with 55-60% probability. Rate hike by year-end: 35-45% (unchanged but the composition of the dissent will clarify this). Effective cut probability: 3-5% (negligible).

$725B AI Capex: Google Wins, Meta Stumbles, MSFT Light on Revenue Attribution

The aggregate $725B combined Big Tech AI capex validates the hardware demand thesis. Beneath the aggregate, a quality differentiation has emerged:

Google (Alphabet) outperformed on cloud growth vs. AWS and Azure. The market rewarded this — Google’s AI capex is perceived as disciplined and revenue-attributable. This strengthens the GOOG/INTU pair trade long leg.

Microsoft guided $190B capex, the largest corporate capital commitment in history, but with light revenue and operating margin guidance. This is the sell signal flagged in prior briefs: capex up without proportionate revenue attribution. MSFT will likely pressure the broader tech complex near-term as investors debate whether the spending generates adequate returns.

Meta was downgraded by JPMorgan on AI monetization concerns and missed on user growth — attributed to Iran-related internet disruptions. The Iran conflict is now directly impairing Meta’s growth metrics, an effect no analyst model anticipated. Combined with the JPM downgrade, Meta has accumulated 2 bearish data points within 24 hours.

AWS at 28% growth beat estimates and validates mid-cycle cloud acceleration. This supports the AMZN HOLD thesis (cloud strong, but $200B capex compresses FCF).

Anthropic fundraising at $900B valuation (surpassing OpenAI) inverts the competitive hierarchy assumptions built into the AI thesis. If the perceived leader is no longer OpenAI, pricing and margin assumptions across the AI value chain become less predictable.

For the hardware layer: NVDA, TSM, MU, ASML, AVGO all benefit from $725B of validated demand flowing through constrained capacity. Goldman’s retail crowding warning in semis (2nd positioning risk signal after BTIG) warrants monitoring but doesn’t change the fundamental thesis — demand is real, validated by corporate commitments, and constrained by physical supply chains.

Blue Owl $9B Headline Masks Fee Disaster: 9th Bearish Data Point for Private Credit

Blue Owl attracted $9B in new capital, but fee-paying AUM grew only $700M. This $8.3B gap represents capital that is either committed but not deployed, in structures that don’t generate fees, or simply overstated relative to productive AUM. For a company whose valuation depends on fee-related earnings, this is the most damaging single data point in the OWL thesis.

Combined with PIMCO, Janus Henderson, and Baird confirming measurable capital flows from private to public credit, the private credit stress thesis now has 9+ independent bearish data points:

KKR KREF 3.9 score

Blue Owl 40.7% redemption gating

CDS on Apollo/Ares/Blackstone

HYG OI P/C structural put positioning

$14B junk bond outflows

Silver Rock $4B distress fund

AI software portfolio impairment channel

Griffin warning + PIMCO/JHG/Baird flow data

Blue Owl $9B headline vs $700M fee-paying growth

Zero counter-signals. BX AVOID, OWL AVOID MAX reinforced.

NATO Fracture: 4th Data Point with Germany Troop Review

Trump’s review of US troop presence in Germany — triggered by Chancellor Merz’s criticism of Iran strategy — is the 4th independent NATO fracture signal (after Spain suspension, EU defense pact draft, Poland questioning commitment). Germany hosts ~35,000 US troops, the largest US military presence in Europe, making this the most consequential of the four.

The NATO fracture thesis has transitioned from monitoring to confirmed pattern. Near-term defense thesis remains insulated (backlogs overwhelmingly domestic for RTX, HII, NOC). Medium-term: EU procurement autonomy will accelerate regardless of whether troop withdrawals actually occur, because the political dynamics now demand European defense self-sufficiency as a plank in every major European party’s platform.

What to Watch

The options market is flashing signals that demand attention: HYG put/call open interest has hit 4.60 — a new conflict high — even as credit spreads remain complacent at 2.85%, creating the widest gap between institutional hedging and spread levels of the entire crisis. QQQ implied volatility sits 11.4pp above realized at 27.6% in steep backwardation, the most extreme reading outside the initial conflict spike. And for the first time, SPY is maintaining elevated protection pricing through an FOMC meeting rather than normalizing — a behavioral shift from all seven prior vol cycles. Whether this elevated regime sustains through May or compresses for the 8th time (creating what would be the cheapest protection window yet ahead of the June Warsh-chaired FOMC), the positioning playbook is materially different from last week. Full options positioning analysis, portfolio playbook, and risk scenario framework below for subscribers.

Options Market Signal

The options market has settled into a coherent post-FOMC + Mag-7 earnings stress regime.

SPY (19.7%, backwardation): 7.2pp above HV. The market is pricing near-term event risk from earnings + oil escalation. The 1-month tenor at 15.8% with 8.7% put skew indicates concentrated downside hedging through mid-May. OI P/C at 1.11 is mildly put-heavy — institutional hedging active but not panicked. SPY has not collapsed back to the 11.1% complacency level from last week, suggesting this vol regime may be stickier than prior normalizations. If SPY IV holds above 15% through next week despite FOMC passing without incident, it would be the first time the market maintained elevated protection pricing during the conflict.

QQQ (27.6%, steep backwardation): 11.4pp above HV — the most extreme QQQ reading outside the Sunday spike. The 1-week tenor at 27.6% vs 1-month at 21.2% reflects concentrated event risk from remaining Mag-7 reports. OI P/C at 0.92 remains call-heavy, meaning the bullish consensus hasn’t fully unwound despite META/MSFT headwinds. The gamma risk flagged in prior briefs remains live: market makers short calls will sell into any decline, amplifying moves.

HYG (6.6%, contango): Near-term IV has remained elevated vs. the sub-3% readings of a week ago but the contango structure persists. OI P/C at 4.60 — highest of the conflict period. Open interest put/call ratio rising to 4.60 even as near-term IV normalizes means institutional investors are steadily accumulating medium-term credit protection. The 1-week put skew at 27.3% is extreme for a near-maturity reading. HY spread at 2.85% (FRED) appears complacent vs. this institutional positioning — the gap between spread levels and options positioning is at conflict highs.

TLT (12.8%, flat): Normalized from Sunday’s 17.0% spike. OI P/C at 0.66 remains call-dominated. The concentrated call buying for a bond rally didn’t pay off through FOMC (yields rose) — these positions may unwind, adding modest selling pressure. At 10Y 4.41% and rising, the structural case against duration strengthens. BNP Paribas now targets 4.55% year-end.

GLD (28.4%, backwardation): Near fair value vs HV (1.0pp spread). Gold at $4,590 stabilized after a two-day pullback from $4,847. The backwardation structure (28.4% near-term → 21.1% at 12-month) reflects concentrated near-term event sensitivity. OI P/C at 0.70 remains call-heavy. Gold’s underperformance relative to oil reflects real rate dynamics dominating safe-haven demand. The structural case via de-dollarization supports positions, but entry timing matters with elevated near-term vol.

International divergence persists and intensifies: VGK at 23.4% (8.7pp above HV, backwardation) — European stress pricing at conflict highs. EWJ at 31.0% (11.0pp above HV, extreme backwardation) — Japan dual shock (petroleum output decline confirmed + BOJ rate expectations). EEM at 33.2% (14.6pp above HV, extreme backwardation) — most extreme EM stress reading, driven by India $125-crude vulnerability. FXI at 23.9% in contango — China remains the only major market not pricing imminent stress. The divergence between FXI contango and all other international ETFs in steep backwardation is the clearest expression of China’s energy insulation advantage.

Synthesis: Options market is pricing genuine stress in a sustained way (not just a 48-hour spike). HYG OI P/C at 4.60 is a new conflict high. QQQ backwardation intensified on Mag-7 results. SPY maintaining elevated vol through FOMC is new behavior. If this elevated pricing regime sustains through May, it would be unprecedented in this conflict; if it normalizes for the 8th time, it would represent the cheapest protection window yet ahead of the June Warsh-chaired FOMC.

This publication is for informational and educational purposes only and does not constitute financial, investment, or trading advice. The analysis, opinions, and commentary presented here should not be interpreted as a recommendation to buy, sell, or hold any security. Always conduct your own research and consult a qualified financial advisor before making investment decisions. Past performance does not guarantee future results.