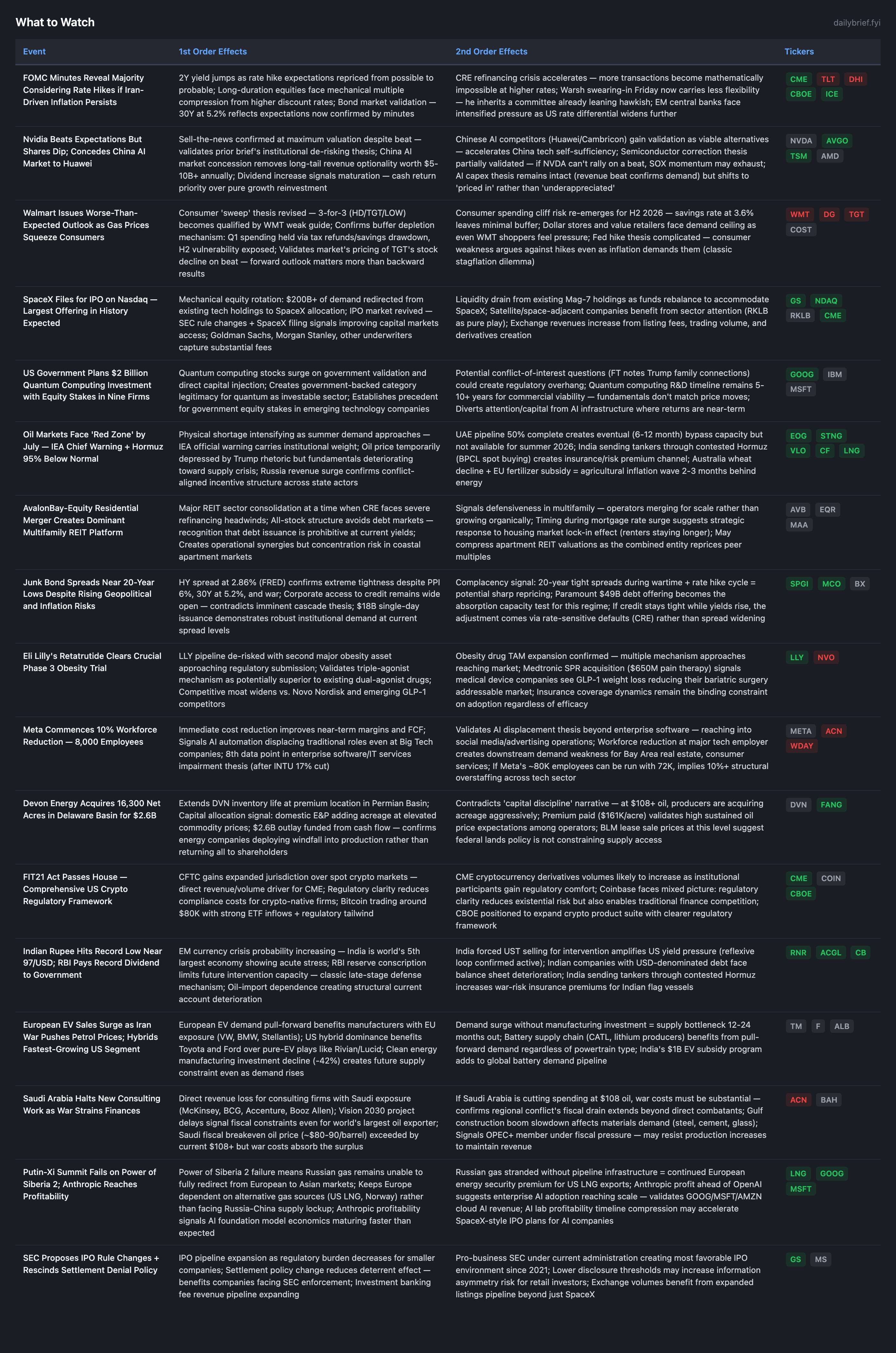

NVDA Beat-and-Dip Activates Semiconductor Correction as FOMC Minutes Reveal Majority Hawkish Lean

Walmart's weak guidance re-introduces the H2 consumer cliff thesis with management confirmation, while 30Y yields hit 5.2% — the tightest financial conditions since before the global financial crisis.

Three developments since yesterday’s brief materially shift the investment picture:

1. NVDA beat-and-dip confirmed. The prior brief’s warning about sell-the-news risk at maximum positioning materialized — shares declined despite beating expectations. Huang’s concession of China’s AI market to Huawei is the more significant strategic development. Semiconductor correction thesis (40-50% within 2-4 weeks) remains active.

2. WMT weak guidance partially reverses the “consumer sweep” narrative. Yesterday’s brief declared consumer-triggered cascade dead based on 3-for-3 beats (HD/TGT/LOW). WMT’s disappointing outlook — citing gas price squeeze on its lower-income customer base — re-introduces the H2 buffer depletion thesis with concrete management guidance behind it. The consumer is not collapsing now but is depleting the resources that sustain spending.

3. FOMC minutes document a majority hawkish lean, not just isolated commentary. Collins and Paulson were previously individual voices. Today’s minutes reveal a majority position considering hikes — a qualitative upgrade from “two members endorsed” to “committee consensus forming.” Combined with 30Y hitting 5.2%, this represents the tightest financial conditions configuration since before the global financial crisis.

The net result: near-term US consumer spending holds but forward guidance deteriorates, structural rate pressure intensifies with institutional backing, and the semiconductor correction catalyst (NVDA dip on beat) has arrived. The IEA’s “red zone by July” oil warning and Indian rupee record low (97/USD) confirm the structural risk pathways remain fully active.

NVDA Beat-and-Dip: Semiconductor Correction Thesis Activated

The prior brief assigned 15-20% probability to NVDA missing or guiding cautiously, and noted that sell-the-news risk was elevated even on a beat due to QQQ put skew flipping bearish and hedge fund de-risking. The outcome: NVDA beat revenue estimates, increased its dividend, but shares declined.

This is the first concrete price signal validating our semiconductor correction probability (40-50% within 2-4 weeks). At $5.7T market cap, NVDA cannot rally on mere beats — it requires acceleration. The China market concession to Huawei removes long-tail optionality worth $5-10B+ annually from a market that was previously $8-12B in gaming + data center revenue.

The dividend increase signals maturation — management acknowledging that pure growth reinvestment has diminishing returns and cash return becomes appropriate. This is characteristic of late-cycle leadership positions.

Immediate implication: The NVDA dip removes the “AI infinity” narrative that supported SOX +50% in 25 days. If the best AI company can’t rally on a beat, the lesser names (AMD, AVGO, MU) face multiple compression pressure.

WMT Weak Guide: Buffer Depletion Thesis Gets Management Confirmation

Yesterday I wrote that TGT stock falling on a beat “suggests the market agrees” with buffer depletion. Today WMT management explicitly cited gas prices squeezing consumer spending power and issued worse-than-expected forward guidance. This is the first major retailer providing forward guidance that directly attributes consumer weakness to the Iran war’s energy cost transmission.

Key distinction: Q1 results were acceptable because tax refunds (one-time buffer) partially offset energy costs. Q2 and beyond lack this buffer. The mechanism our framework identified — savings rate 3.6% + negative real wages + PPI passthrough creating an H2 cliff — now has direct management validation from the world’s largest retailer.

This revises the consumer picture: “immediate collapse eliminated” remains true, but “H2 2026 vulnerability” upgraded from thesis to management-confirmed outlook. The credit cascade probability should remain at 40-45% (consumer trigger dead for Q2) but recession probability for H2 adjusts upward toward 55-60%.

FOMC Minutes: Committee-Level Hawkishness

The prior brief tracked Collins and Paulson as individual endorsements of rate hikes. Today’s minutes reveal a majority position. Individual comments can be dismissed as outliers, but a documented majority consensus creates institutional momentum toward action.

Combined with: 30Y at 5.2% (19-year high per multiple sources), 10Y at 4.67% (FRED confirmed), and forecasters projecting 6% Q2 inflation, the rate hike probability now approaches 40-45%. Warsh inherits a committee pre-positioned for hawkishness on Friday — his first meeting will not be about building consensus for hikes but about whether he can resist the majority view.

The mechanism: PPI 6% → CPI passthrough → Q2 at 4.5-5.5% → FOMC majority already documented as favoring hikes → June 16-17 meeting becomes a live event. The 10Y-2Y spread at 0.53% (FRED) with both yields rising simultaneously signals the market expects tightening rather than recession.

SpaceX IPO Filing: Capital Markets Rotation Pressure

SpaceX filing for Nasdaq listing under SPCX with Goldman as lead underwriter is the most significant IPO event since Alibaba (2014) or Saudi Aramco (2019). At $350B+ valuation, this creates mechanical rotation pressure on existing tech holdings as institutional mandates require allocation.

Combined with SEC rule changes making IPOs cheaper/faster and Inspire Brands’ confidential filing, the H2 2026 IPO pipeline is building rapidly. Paramount’s $49B debt sale + SpaceX’s equity offering + Inspire’s IPO = unprecedented capital markets absorption requirement at 30Y 5.2%.

BofA’s survey showed fund managers at lowest cash since Feb 2024. SpaceX allocation money must come from existing equity positions. The largest IPO in history arriving during maximum positioning creates forced selling of current holdings regardless of fundamentals.

$2B Federal Quantum Computing Investment

The government taking equity stakes in nine quantum companies represents a novel policy instrument worth monitoring but not yet actionable. Quantum computing remains 5-10+ years from commercial viability at scale. The Trump family connection flagged by FT introduces governance risk that could create volatility in the category.

For large-cap positioning: Google (Willow chip) and IBM (largest commercial quantum program) have the most direct exposure. Insufficient for conviction change but worth tracking as government capital allocation increasingly picks technology winners.

Anthropic Profitability: AI Lab Economics Maturing

Anthropic reaching profitability ahead of OpenAI and xAI is meaningful for two reasons: (1) it validates that AI model companies can achieve sustainable unit economics at current pricing, and (2) Google is a major Anthropic investor/partner, making this directly relevant to GOOG’s thesis.

If Anthropic (smaller scale, fewer products) is profitable, OpenAI and the major cloud providers’ AI inference businesses are likely at or near profitability as well. This removes the “AI revenue but no AI profit” objection that has constrained valuations for some cloud names.

What to Watch

Today’s convergence of NVDA’s beat-and-dip, FOMC majority hawkishness, and WMT’s management-confirmed consumer weakness creates a complex positioning challenge. Our options data scan failed for this session — meaning we cannot verify whether QQQ’s bearish put skew (which flipped from -14.6% to +8.6% on May 20) intensified further post-NVDA, or whether EEM’s extreme 36.2% near-term IV widened on the rupee’s continued deterioration. The semiconductor correction thesis is now active with 40-50% probability, the H2 recession probability has been upgraded to 55-60%, and rate hike probability approaches 40-45% — each requiring distinct hedging approaches. Full options positioning analysis, portfolio playbook, and risk scenario framework below for subscribers.

This publication is for informational and educational purposes only and does not constitute financial, investment, or trading advice. The analysis, opinions, and commentary presented here should not be interpreted as a recommendation to buy, sell, or hold any security. Always conduct your own research and consult a qualified financial advisor before making investment decisions. Past performance does not guarantee future results.