NATO Fracture and Enterprise Software Impairment Emerge as Twin Structural Risks

HYG put skew hits conflict highs as credit markets diverge sharply from equities touching record levels.

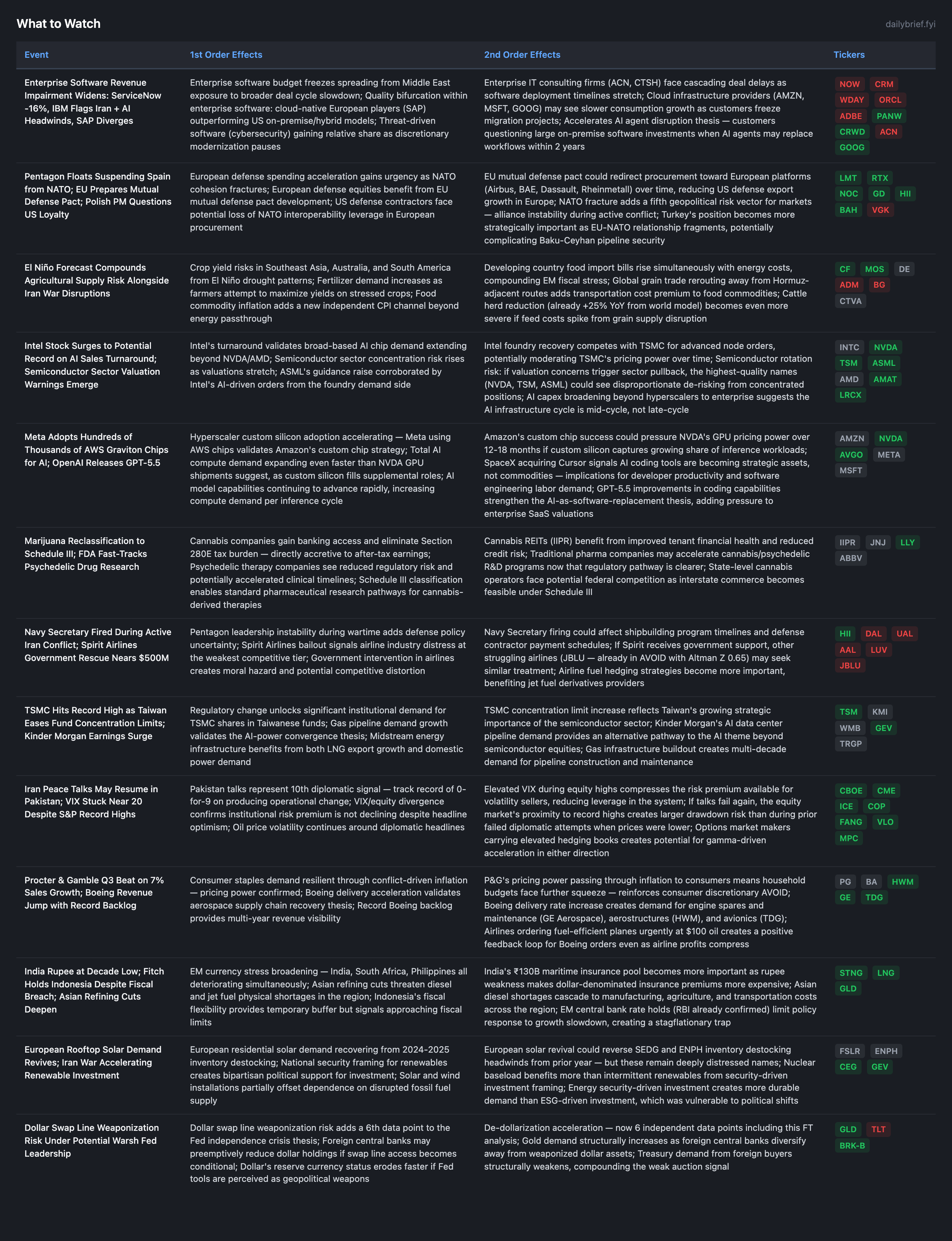

Two material shifts since yesterday’s brief. First, the enterprise software revenue impairment thesis escalated from early signal to confirmed pattern: ServiceNow’s 16% drop on Iran-war deal delays, corroborated by IBM CEO flagging identical headwinds, now has a quality bifurcation dimension — SAP beat the same week, showing European cloud-native platforms are more resilient than US hybrid/on-premise models. This is the third independent data point (ServiceNow, IBM, and the broader sympathy selloff in CRM/WDAY/ORCL) and justifies moving from monitoring to active positioning.

Second, NATO fracture emerged as a new geopolitical vector. A leaked Pentagon email discussing Spain’s suspension from NATO, the EU drafting a mutual defense pact, and Poland’s PM publicly questioning US defense commitment collectively represent a qualitative shift in transatlantic security architecture. Prior briefs covered European defense spending increases as a fiscal response to the energy crisis, but NATO institutional fracture during an active US military conflict is a different category of risk. The investment implication cuts both ways: near-term bullish for US defense contractors (domestic demand unaffected, European spending accelerating regardless of alliance structure) but creates a multi-year headwind for US defense export growth if EU procurement autonomy gains traction.

The Iran conflict continued its pattern: ceasefire operationally irrelevant for the 10th signal, Iran’s foreign minister traveling to Pakistan for potential talk resumption, VIX stuck near 20 despite S&P touching record highs. Oil remains volatile near $100.

NATO Institutional Fracture: A Fifth Geopolitical Risk Vector

The Pentagon floating Spain’s NATO suspension, the EU drafting a mutual assistance pact, and Poland questioning US defense loyalty represent three independent signals in a single 48-hour window. This is qualitatively different from the German military strategy or Japan warship export — those were spending signals within existing alliance frameworks. NATO fracture during an active US military conflict with Iran is a structural threat to the post-Cold War security order.

US defense demand is domestically driven (dual-theater, $1.5T+ budget) and not dependent on NATO cohesion. European defense spending accelerates regardless — whether under NATO or an EU mutual defense framework, Europe needs to rearm. The beneficiaries shift: European contractors (Rheinmetall, BAE, Dassault, Airbus Defence) gain relative share over time if EU procurement autonomy becomes policy.

For tracked US names (LMT, RTX, NOC, GD, HII, LHX, KBR, LDOS), the multi-year European export growth assumption needs monitoring. Current backlogs ($193.6B LMT, $268B RTX, $53.1B HII) are overwhelmingly US domestic and Middle East, so near-term earnings are insulated. Downgrade export growth assumptions by 5-10% for FY2028+ if EU defense pact materializes.

Enterprise Software: From Early Signal to Confirmed Revenue Impairment

ServiceNow’s 16% decline represents the sharpest single-session loss for a best-in-class enterprise software name since 2022. The cause — delayed Middle East on-premise subscription deals — was corroborated within 24 hours by IBM’s CEO citing identical Iran-war headwinds. SAP’s simultaneous Q1 beat creates a quality bifurcation with investment implications.

The mechanism: enterprises with Middle East exposure are freezing large-ticket software deployments during geopolitical uncertainty. This is classic risk-aversion behavior where CIOs delay discretionary modernization spending when the operating environment is unstable. The AI disruption layer compounds this — why commit to a $50M ServiceNow implementation when AI agents may restructure the workflows within 2 years?

SAP’s divergence suggests European companies with entrenched ERP positions are more resilient because their revenue is more recurring and less dependent on new large-deal bookings. The pair trade implication is clear: the GOOG/INTU and TSM/WDAY short legs should see continued pressure. PANW, CRWD, and FTNT as threat-driven demand beneficiaries gain relative share as enterprise budgets rotate from modernization to security.

For IT consulting (ACN, the short leg in two active pair trades), ServiceNow/IBM deal delays cascade directly to implementation revenue. ACN’s India labor-cost model faces simultaneous pressure from rupee weakness (positive for cost basis) and deal volume decline (negative for revenue). The net effect is negative.

El Niño: Independent CPI Channel Activation

The strong El Niño forecast adds an independent, non-energy inflationary channel to the existing 19+ CPI vectors. El Niño affects crop yields in Southeast Asia, South America, and Australia through precipitation pattern shifts. Combined with Iran-disrupted agricultural trade routes and Hormuz-proximate fertilizer shipments, the food inflation pipeline now has three independent supply-side pressures.

For CF Industries (MAX CONVICTION), this is the 17th confirmation: El Niño-driven crop stress increases fertilizer demand as farmers need maximum yield from stressed acreage. The counter-signal from China’s coal-based urea production remains the single bearish data point against 17 bullish ones. For MOS, the same logic applies to potash and phosphate.

Food prices represent ~14% of the CPI basket. If El Niño reduces global crop yields by 3-5% (typical for strong events), food CPI could add 50-80bps to headline inflation over a 6-12 month lag. Combined with the energy channel already active at 3.3% CPI (FRED: 330.29 March), the probability of April CPI exceeding 4.0% increases from 65-75% to 70-80%.

AI Infrastructure Broadening: Custom Silicon Gains Traction

Three signals: Meta adopting hundreds of thousands of AWS Graviton chips for AI, Intel’s potential record daily gain on AI-driven sales turnaround, and OpenAI releasing GPT-5.5. Together these confirm the AI compute demand curve is expanding faster than any single company’s supply can capture. Intel’s turnaround, if sustained, validates that AI silicon demand is broad enough to support multiple foundry/design winners simultaneously.

The competitive risk for NVDA is real but slow-moving. Custom silicon (Graviton, Google TPU, Meta’s custom chips) captures inference workloads, while NVDA retains training dominance through CUDA. NVDA at 23x FY2027E remains reasonable if training demand continues growing. Intel’s recovery primarily competes with AMD in data center CPU, not with NVDA in GPU/accelerator.

BTIG’s warning about semiconductor valuations approaching “parabolic” levels (Tier 2 source) deserves attention. ASML’s €40B guidance + €12B buyback provides fundamental backing, but valuation multiples across the sector are pricing perfection. Any disappointment in upcoming NVDA (May) or TSM (next quarter) earnings could trigger a significant rotation. The appropriate response is not to exit positions but to monitor for signs of capex commitment softening. KMI’s earnings surge from gas pipeline demand for AI data centers provides a second confirmation that the AI power/infrastructure buildout is mid-cycle, not late-cycle.

Dollar Swap Line Weaponization: 6th De-Dollarization Data Point

The FT analysis of Warsh potentially aligning with Bessent’s geoeconomic agenda to weaponize dollar swap lines is the 6th independent data point for de-dollarization: (1) FT energy trade from USD, (2) Iran crypto tolls, (3) China yuan payments, (4) India/ICICI yuan settlements, (5) Russia crypto legislation, (6) FT swap line weaponization analysis. This signal is analytical (FT commentary, Tier 2) rather than hard data, but it reflects institutional thinking at the highest levels of financial journalism. The structural gold thesis continues to strengthen.

Developing Themes

Credit Markets: HYG Stress Configuration Persists. HYG OI P/C at 4.37 (moderated slightly from 4.42 yesterday). The 1-week put skew surged to 83.0% — the most extreme single-tenor skew reading of the entire conflict, up from 59.5% yesterday. Contango structure maintained (5.8% → 10.9%). Concentrated near-term put buying is intensifying as May BDC NAV reporting approaches. Upgrade probability of a localized credit event within 4 weeks to 60-70%.

Consumer Contraction: 11th Signal. UK consumer confidence at lowest since 2023 (Reuters Tier 1), Trump economic approval at lowest of both terms (CNBC Tier 2), Nike cutting 1,400 more jobs (Tier 2), P&G beating via pricing power (meaning consumers paying more for essentials). Four new data points extending the pattern to an 11th consecutive signal. All consumer discretionary remains AVOID.

Boeing Recovery Gains Third Data Point. Boeing revenue jump, narrowing losses, and record backlog adds to the prior brief’s assessment of delivery lead and FAA certification visibility. Three positive data points in a single reporting cycle. Still not BUY — negative FCF — but monitoring confidence increases. Aerospace supply chain (HWM, GE, TDG) benefits are confirmed.

US PMI: Stagflation Configuration. S&P Global flash PMI shows US business activity recovering in April while input prices rise on Iran conflict. This is the textbook stagflationary configuration: improving activity (preventing rate cuts) paired with war-driven cost pressures (preventing policy normalization). Aligns with the rate path: 35-45% hike, 3-5% cut, 52-60% no action.

Continuing Themes

Iran conflict: 0-for-9 on diplomatic signals producing operational change. Pakistan talks may resume — 10th signal to monitor. Ship seizures continue. Three-front European energy crisis persists. All structural positions maintained.

Fed policy: Unchanged. Warsh inflation-first + Tillis blocking. FRED data: Fed Funds 3.64%, 10Y at 4.30%, 2Y at 3.79%, 10Y-2Y spread 0.51%.

Defense: LMT Q1 earnings remain the sector valuation anchor. NATO fracture adds European spending urgency but creates long-term export risk.

AI infrastructure: ASML guidance validated by Intel turnaround and KMI gas pipeline demand. Sector valuation warnings emerging (BTIG). Mid-cycle, not late-cycle.

What to Watch

The options data beneath today’s surface calm tells a sharply different story than equities at record highs. HYG’s 1-week put skew accelerated to 83.0% — the most extreme single-tenor reading of the entire conflict — while SPY vol normalized for the fifth time to just 17.2%. This credit-equity divergence is the widest of the conflict, and credit historically leads equity with a ~70% base rate. Meanwhile, EWJ Japan near-term IV exploded to 41.6% (21.6pp above realized), the largest single-ETF richness reading tracked, signaling significant reversal risk in a crowded trade. The premium section below breaks down exactly how to position around the HYG credit event threshold, which pair trades to add to, and the specific risk scenarios — including a 60-70% probability localized credit event — that could reprice this market within weeks.

Full options positioning analysis, portfolio playbook, and risk scenario framework below for subscribers.

This publication is for informational and educational purposes only and does not constitute financial, investment, or trading advice. The analysis, opinions, and commentary presented here should not be interpreted as a recommendation to buy, sell, or hold any security. Always conduct your own research and consult a qualified financial advisor before making investment decisions. Past performance does not guarantee future results.