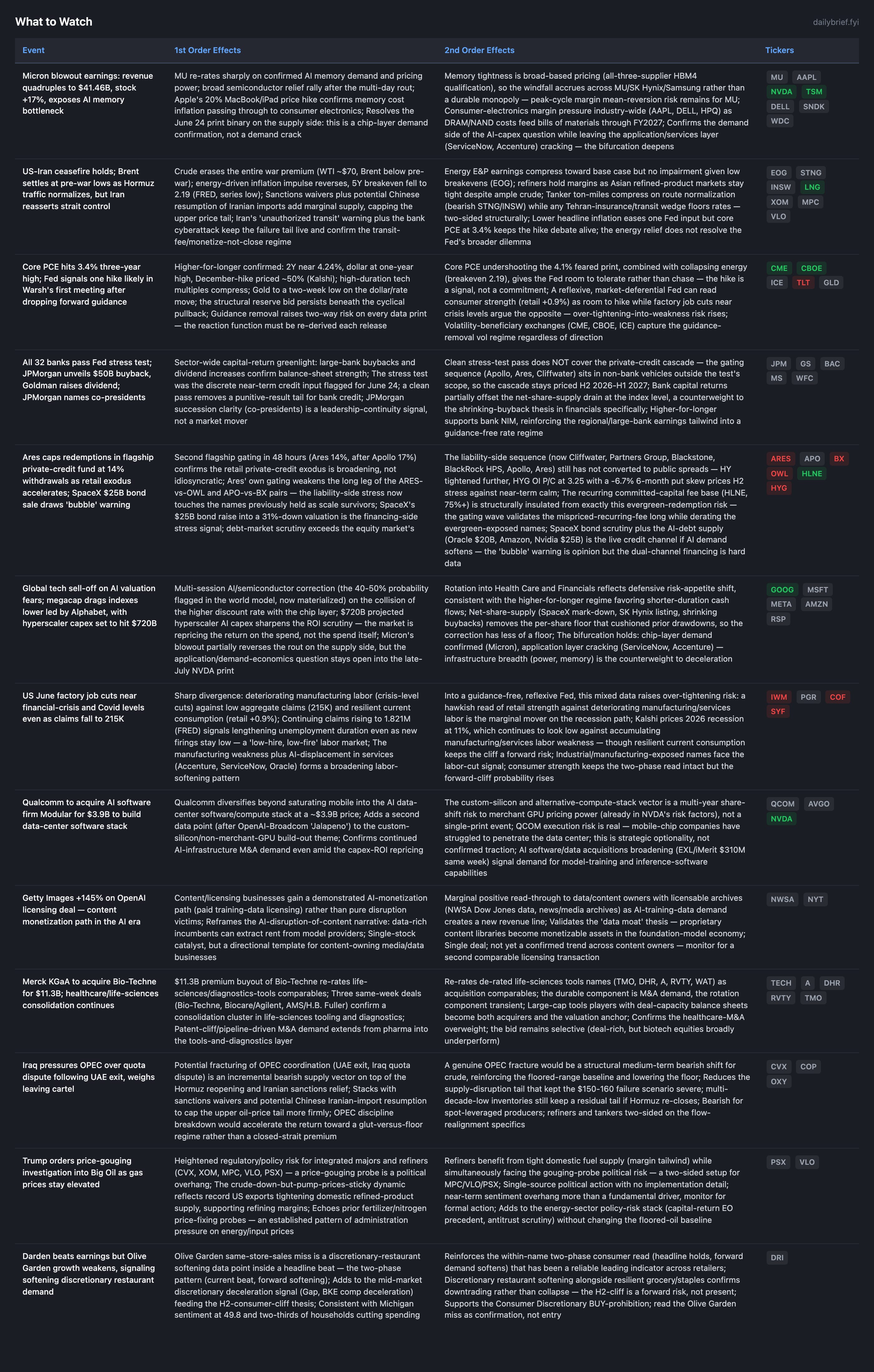

Micron's Blowout Confirms AI Memory Demand as the Application Layer Keeps Cracking

Ares becomes the sixth manager to gate redemptions — and the first scale survivor — even as all 32 banks pass a clean stress test that doesn't touch the private-credit cascade.

The two month-long binaries (Hormuz, the Warsh FOMC) are now fully resolved, and most of today’s batch is consequence. Brent settled at pre-war lows with the 5Y breakeven down to 2.19 (FRED, a series low), core PCE printed 3.4% — a three-year high but well below the feared 4.1% — and the dollar sits at a one-year high as the December-hike probability holds near 50% (Kalshi). The chip-layer correction the world model flagged at 40-50% probability materialized over multiple sessions and then partially reversed.

Three things are genuinely new. First, Micron’s blowout (revenue quadrupled to $41.46B, stock +17%) plus Apple’s 20% MacBook/iPad price hike on memory costs resolves the June 24 print binary on the supply side: AI memory demand is confirmed and tight, not cracking. The application layer (ServiceNow, Accenture) keeps cracking, deepening the bifurcation. Second, Ares capped its flagship private-credit fund at 14% withdrawals, the second flagship gating in 48 hours after Apollo’s 17%; this is a material new data point because Ares was the long leg of the ARES-vs-OWL pair, so the liability-side stress has now reached the scale survivors. SpaceX’s $25B bond raise into a 31%-down valuation, drawing an Allianz “bubble territory” warning, is the financing-side companion. Third, all 32 banks passed the Fed stress test (clean), greenlighting JPMorgan’s $50B buyback and Goldman’s dividend raise, but the test does not cover the non-bank private-credit cascade, so that stays priced H2 2026-H1 2027 with HY spreads still showing no conversion (HYG OI P/C 3.25, -6.7% six-month put skew).

Underneath, US June factory job cuts approached crisis levels against falling claims (215K) and resilient retail (+0.9%), sharpening the over-tightening-into-weakness risk into a guidance-free, reflexive Fed. Getty Images +145% on an OpenAI licensing deal is a small but novel signal: a demonstrated AI-monetization path for content owners.

Micron Resolves the Chip-Layer Demand Question on the Supply Side; the Bifurcation Deepens

Micron’s revenue quadrupled to $41.46B (CNBC/Bloomberg/FT, Tier 1-2, multi-source), the stock jumped 16-17%, and Apple raised MacBook/iPad prices ~20% citing the memory shortage (CNBC/FT, Tier 2). These are two corroborating data points: AI memory demand is robust and tight enough to pass through to consumer-device pricing. This resolves the June 24 print binary I held MU two-sided into; the supply side of the AI-capex question is confirmed, not cracking.

The mechanism matters for how far to extrapolate. Memory ran ~830% over twelve months, and the all-three-supplier HBM4 qualification means this is broad commodity pricing tightness, not a durable monopoly. So I read Micron as confirming AI infrastructure demand (supporting NVDA/TSM into the late-July prints) while leaving MU itself a two-sided HOLD at peak-cycle margins facing eventual mean-reversion. The blowout does not restore asymmetry at this multiple. Apple’s 20% price hike is the second-order tell: memory cost inflation now feeds consumer-electronics bills of materials through FY2027, a margin/demand headwind for AAPL, DELL, and HPQ.

The bifurcation is the durable read. The chip layer (Micron) confirmed demand while the application layer keeps cracking (ServiceNow’s drop on a strong print, Accenture -17%). The infrastructure-layer breadth (memory, power, materials) is the counterweight to the deceleration hypothesis.

Ares Gates Its Flagship — Liability-Side Stress Reaches the Scale Survivors

Ares capped redemptions in its flagship private-credit fund at 14% withdrawals (FT, Tier 2), the second flagship gating in 48 hours after Apollo’s 17% the prior day. This is a material new data point: Ares was held as the long leg of the ARES-vs-OWL pair on a scale-survivor thesis, so the liability-side stress has now reached the names previously considered insulated. The named-gating sequence is now six deep (Cliffwater, Partners Group, Blackstone, BlackRock HPS, Apollo, Ares).

I am downgrading the ARES leg of that pair to bearish pending evidence; the broadening retail exodus weakens the differentiation between “scale survivor” and “redemption-exposed” that the pair rested on. The cleaner expression of the cascade thesis is now HLNE long (recurring committed-capital fee base, 75%+, structurally insulated from evergreen redemptions) against the broadly evergreen-exposed complex. SpaceX’s $25B bond raise into a valuation down 31% from its high, with Allianz’s CIO warning of “bubble territory” and noting debt investors will scrutinize the company more than equity holders did, is the financing-side companion: the dual-channel debt-and-equity financing of capital-intensive ventures stacking on AI-purpose debt (Oracle $20B, Nvidia $25B, Amazon).

The sequence still has not converted: HY spreads tightened further, and HYG shows OI P/C 3.25 with a -6.7% six-month put skew, H2 stress priced against near-term calm. The first HYG spread move off tight levels remains the reflexivity tell.

Clean Stress Test Greenlights Bank Capital Returns — But Doesn’t Touch the Cascade

All 32 large banks passed the Fed’s annual stress test (Federal Reserve, Tier 1), confirming they can lend through a severe downturn. JPMorgan announced a $50B buyback and Goldman raised its dividend (CNBC, Tier 2). This was the discrete near-term credit input flagged for June 24, and the clean pass removes a punitive-result tail for bank credit.

The distinction that matters: the stress test covers bank balance sheets, while the gating sequence (Apollo, Ares, et al.) sits in non-bank private-credit vehicles outside the test’s scope. A clean bank pass does not de-risk the private-credit cascade; these are separate systems, and the cascade stays priced H2 2026-H1 2027. Bank capital returns do partially offset the net-share-supply drain at the index level within financials specifically, and higher-for-longer supports NIM into a guidance-free rate regime. JPMorgan’s co-president appointments (Petno, Rohrbaugh) are leadership-continuity signal, not a market mover.

Getty +145% on OpenAI Licensing — A Demonstrated AI-Monetization Path for Content

Getty Images surged 145% on an OpenAI partnership (Bloomberg, Tier 2) after being battered by the AI “scare trade.” The mechanism is new: data-rich content owners can extract licensing rent from foundation-model providers rather than being pure disruption victims. This is a single-stock catalyst, but it is a directional template: the “data moat” becomes a monetizable asset in the model economy. Marginal positive read-through to content/data owners with licensable archives (NWSA’s Dow Jones, NYT). One deal is a data point, not a trend; monitor for a second comparable transaction before building conviction.

What to Watch

Developing Themes

Iran/Oil: Floored-Range Baseline Firms as Supply Vectors Stack

Brent settled at pre-war lows (Reuters, Tier 1) as Hormuz traffic normalizes, both chambers of Congress voted to halt US involvement (reducing the escalation tail), and the supply side firmed bearishly: sanctions waivers authorizing Iranian imports through August, Chinese state refiners weighing resumption of Iranian crude, and Iraq pressuring OPEC over quotas after the UAE’s exit (a potential discipline-fracture vector). Against this, Iran warned ships against “unauthorized transit” and an Iran cyberattack hit three banks, keeping the failure tail live and confirming the transit-fee/monetize-not-close regime rather than a clean reopening. The net is a firmer floored-range baseline with a lower floor as supply vectors stack, but multi-decade-low inventories keep a residual tail if Hormuz re-closes. Asian refined-product markets stay tight despite ample crude, supporting refining margins (MPC, VLO, PSX), though Trump’s price-gouging probe into Big Oil adds a political overhang to the same names. STNG/INSW stay two-sided on ton-mile compression versus the insurance wedge. The 5Y breakeven at 2.19 confirms the deflating energy impulse pulling H2 headline toward ~3.5%.

Consumer: Two-Phase Read Intact, Forward-Cliff Tells Accumulating

Darden beat but Olive Garden same-store sales missed (CNBC, Tier 1), the two-phase pattern (headline holds, forward discretionary demand softens) that has been a reliable leading indicator. This stacks on the BKE comp deceleration and Gap mid-market crack. Against it, May retail rose 0.9% and existing home sales held, showing current-condition strength. The Reuters poll keeping mortgage rates elevated through 2027 and new-home-sales weakness confirm the housing rate-chain. The cliff remains a forward risk (Kalshi 2026 recession 11%, which looks low), not present. PGR over COF, extending to SYF; Consumer Discretionary BUY-prohibited.

De-Dollarization and Net-Share-Supply: Compounding Long-End Pressure

China’s yuan-internationalization measures plus fiscal austerity (deficit narrowed first time in two years) add to the de-dollarization cluster, structural upward pressure on the US long end compounding the carry-unwind and record AI-debt/IPO supply. SpaceX’s mark-down (now financing via $25B debt) confirms the no-passive-bid net-supply drain. The 30Y at multi-year highs and TLT’s -4.0% 12-month put skew confirm bearish duration; the structural gold bid persists beneath the cyclical pullback to a two-week low.

Continuing Themes

Rates: Higher-for-longer confirmed; one 2026 hike signaled, guidance removed. Do not pre-position into the reflexive Fed; let CME/CBOE/ICE carry the vol. Core PCE undershooting the feared 4.1% plus collapsing breakevens gives the Fed room to tolerate rather than chase.

Custom silicon: Qualcomm-Modular ($3.9B) is a second data point (after OpenAI-Broadcom Jalapeno) in the merchant-GPU share-shift watch — multi-year risk in NVDA’s risk factors, not a flip signal. QCOM execution unproven.

Power/electrical: Overweight intact; data-center load confirmed across utility hard data. GEV-vs-ORCL CORE. No material change today.

Healthcare M&A: Merck KGaA/Bio-Techne $11.3B plus Agilent/Biocare and H.B. Fuller/AMS extend the consolidation into life-sciences tooling; re-rates de-rated comparables (TMO, DHR, A, RVTY). The durable component is M&A demand.

Crypto: Bitcoin to multi-year lows (~$60K and below), options positioning bets on further downside; structural positives (Clarity Act) against waning momentum. No portfolio-relevant change.

The GLP-1 and Airlines theses got no fresh direct evidence; today’s lower-fuel read and the airline-route resumption marginally support the UAL/DAL-over-LUV lean by consistency. I continue to flag LMT (AVOID 4.9) for active re-examination given the US munitions-demand tailwind against its bottom-up rating.

The durable options signals tell a sharper story than the headline tape: QQQ’s -3.0% 12-month skew was held — not unwound — straight through Micron’s confirmation, while HYG sits at a 3.25 OI P/C with a -6.7% six-month put skew, pricing H2 cascade stress against near-term calm even as Ares became the sixth manager to gate. The EWJ +17.5% one-month put skew and EEM +16.6% one-week skew flag the carry-unwind and dollar/EM repricing that bled the South Korean plunge into US futures. Below, the portfolio playbook lays out exactly where to hold infrastructure conviction versus the application-layer shorts, how to position the private-credit cascade (downgrade ARES, hold HLNE), and where bearish duration and the structural gold bid sit — plus the seven risk scenarios that would convert these setups.

Full options positioning analysis, portfolio playbook, and risk scenario framework below for subscribers.

This publication is for informational and educational purposes only and does not constitute financial, investment, or trading advice. The analysis, opinions, and commentary presented here should not be interpreted as a recommendation to buy, sell, or hold any security. Always conduct your own research and consult a qualified financial advisor before making investment decisions. Past performance does not guarantee future results.