Labor Re-Acceleration Hardens the Hawkish Case as Private-Credit Gating Goes Mainstream

Cliffwater and Partners Group cap redemptions on named retail funds, confirming the liability-side stress that canonically precedes the asset-side cascade

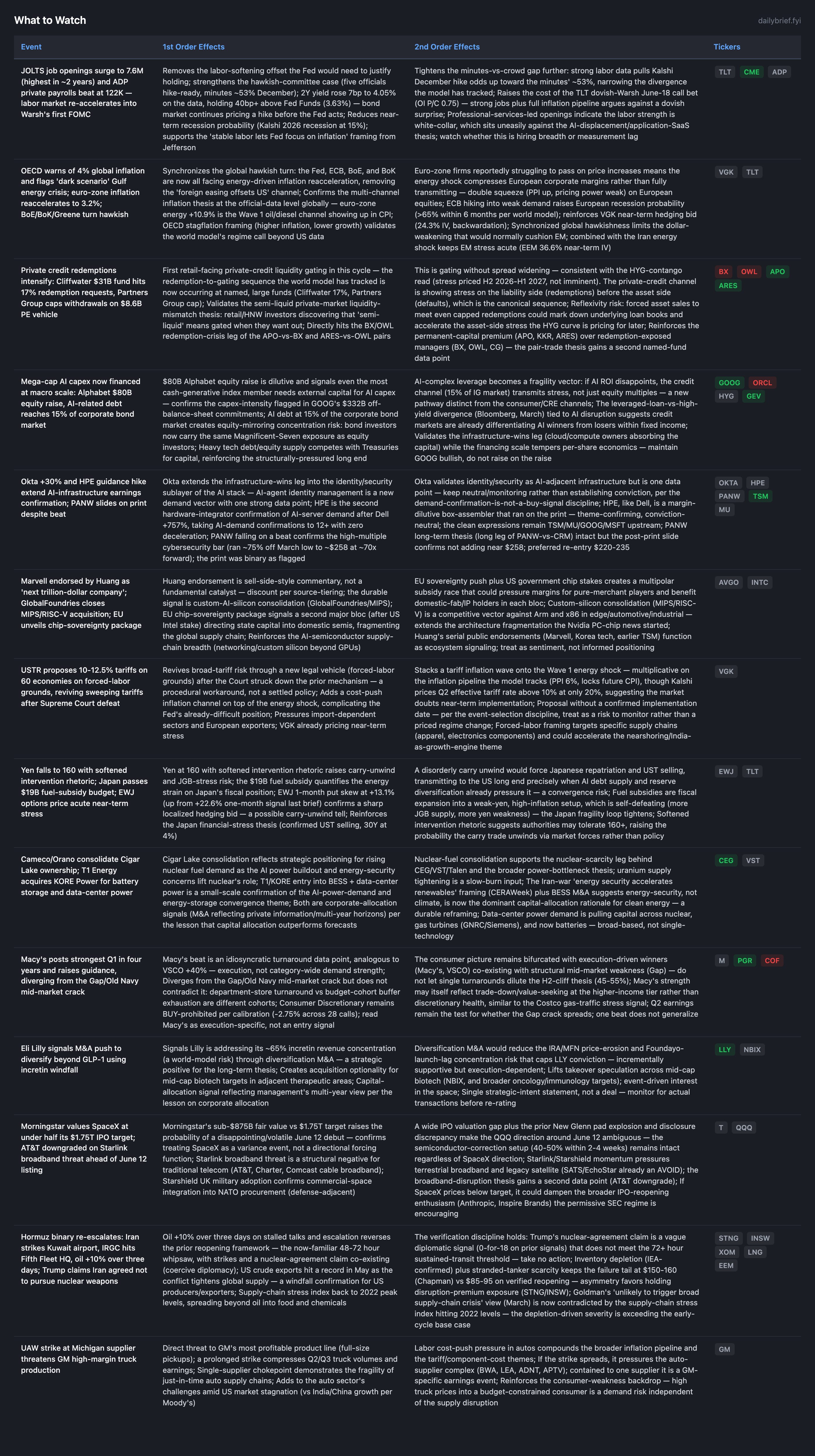

The macro landscape is largely unchanged, but three datasets sharpened the rate picture and one credit development crossed from forecast to fact. The labor market re-accelerated: JOLTS openings surged 731K to 7.6M (highest in nearly two years) and ADP printed 122K (strongest in 16 months, broad-based), removing the labor-softening offset the Fed would need to justify holding into Warsh’s June 16-17 inaugural FOMC. The 2Y rose to 4.05%, holding 40bp+ above Fed Funds. Combined with the OECD lifting its 2026 global inflation forecast to 4%, euro-zone inflation reaccelerating to 3.2% (energy +10.9%), and the BoE’s Greene plus the BoK turning hawkish, the global central-bank stance is synchronizing toward tightening. The minutes-vs-Kalshi gap (minutes ~53% December, Kalshi 37%) continues to narrow as the data validates the committee.

The credit development that matters: private-credit redemption stress moved from anonymous fund-bond selloffs to named gating. Cliffwater’s $31B retail fund hit 17% redemption requests with limited withdrawals, and Partners Group capped redemptions on its $8.6B PE vehicle. This is the liability-side stress (redemptions, gating) that canonically precedes asset-side stress (defaults, spread widening), and it is consistent with the HYG-contango read that prices the cascade for H2 2026-H1 2027 rather than now. It is the second named confirmation of the redemption crisis underpinning the APO-vs-BX and ARES-vs-OWL pairs.

The Hormuz binary re-escalated again (Iran struck Kuwait’s airport, IRGC hit the Fifth Fleet HQ, oil +10% over three days) against Trump’s vague claim that Iran agreed not to pursue nuclear weapons. This is the 18th-19th reversal in the 48-72 hour cadence; the verification discipline (0-for-18 on diplomatic signals) holds, take no action. The supply-chain stress index returned to 2022 peak levels, contradicting Goldman’s March view that the conflict was unlikely to cause a broad supply-chain crisis.

New Developments

Private-Credit Redemption Stress Reaches Named Funds

Two FT reports (Tier 2) confirm the redemption-to-gating sequence at large, named funds, following the February private-credit-fund bond selloff (Reuters) and earlier semi-liquid stress reports, making this a 3+ data-point pattern.

The mechanism matters for timing. This is liability-side stress: retail and HNW investors discovering that “semi-liquid” means gated when they try to exit. It precedes asset-side stress (loan defaults, NAV markdowns, spread widening). That sequencing is what the HYG curve has been pricing: contango (near 2.5% < 12-month 7.6%, OI P/C 3.91), stress 6-12 months out, not imminent. The credit-cascade-via-primary-closure pathway stays dormant (IG access wide open, $18B single-day issuance, May the busiest in six years). The live pathway is the HYG-contango window.

The reflexivity risk is the thing to watch: forced asset sales to meet even capped redemptions could mark down underlying loan books and pull the asset-side stress forward. It reinforces the permanent-capital premium (APO, KKR, ARES) over redemption-exposed managers (BX, OWL, CG). I am holding BX and OWL bearish-lean (3+ data points across the redemption series) and APO/ARES bullish-lean, with the calibration caveat that APO at a 7.55 score still lost 16.9% historically, so conviction is moderate.

Labor Re-Acceleration Tightens the Rate Picture

JOLTS (BLS, Tier 1) and ADP (Tier 1/2) are hard data, not commentary, and they remove the labor-softening case for holding rates. The 2Y rose 7bp on the data.

The effect is to narrow the minutes-vs-crowd gap the model has tracked: Kalshi’s December hike probability is now 37% (up from 18% two weeks ago, 31% last week), converging toward the minutes’ ~53% as the data validates the hawkish committee. Per the lesson that ADP is a poor BLS predictor this cycle (62K vs 178K previously), I weight JOLTS more heavily; the May payrolls report is the decisive input. One tension: professional-services led the openings, which is white-collar hiring breadth sitting uneasily against the AI-displacement thesis for application SaaS. Either the displacement is slower than the bifurcation thesis implies, or this is measurement lag worth monitoring.

The discipline holds: do not pre-position for June 16-17. The dovish-Warsh TLT June-18 call concentration (OI P/C 0.75) is now fighting both strong labor data and a full inflation pipeline; that bet is harder to justify than it was, but Warsh’s “patient hawk”/AI-disinflation framing keeps a dovish surprise live. Two-sided; let exchanges (CME, ICE) carry the vol.

Synchronized Global Hawkish Turn

The OECD (Tier 2) flagged a “dark scenario” if the Gulf energy crisis persists. South Korean inflation reached a two-year high, and the BoE’s Greene said the rate-hike case strengthens the longer the conflict lasts. This is the global version of the Wave 1 oil/diesel inflation channel showing up in official CPI across blocs (CNBC, Tier 2 for euro-zone).

The consequence is the removal of the foreign-easing offset: the Fed, ECB, BoE, and BoK now all face energy-driven reacceleration simultaneously. A separate Reuters report that euro-zone firms struggle to pass on price increases means the European version is a margin squeeze (PPI up, pricing power weak) rather than full pass-through, which raises European recession probability and is consistent with VGK’s near-term stress pricing (24.3% IV, backwardation, vs 15.6% HV). Synchronized hawkishness also limits the dollar weakening that would normally cushion EM, keeping EM stress acute.

What to Watch

Developing Themes

Hormuz: 18th-19th Reversal, Supply-Chain Stress Contradicts Goldman

Multiple Tier 1 Reuters reports confirm the strikes and the oil move as talks stalled. The cadence is unchanged (48-72 hour flips, 0-for-18 on signals). The new hard data point is the global supply-chain stress index returning to 2022 peak levels (Statista/Bloomberg), spreading into food and chemicals. Depletion-driven severity is exceeding the early-cycle base case. US crude exports hit a record in May (Reuters), a windfall confirmation for US producers. The asymmetry is unchanged: failure tail $150-160 (Chapman) vs $85-95 on verified reopening. Hold STNG/INSW and LNG (insulated via QatarEnergy force majeure to mid-August, plus the Inpex Ichthys strike threat adding LNG supply risk); do not reduce until 72+ hours sustained transit. The Kuwait airport strike raises the UAE/Saudi-infrastructure-retaliation tail.

AI Infrastructure: Two More Earnings Confirmations, Financing at Macro Scale

HPE raised guidance on AI-server demand (second integrator after Dell), and Okta surged 30% on AI-agent identity demand, taking AI-demand confirmations to 12+ with zero deceleration. Both are theme-confirming, conviction-neutral: HPE is a margin-dilutive integrator that ran on the print, and Okta is a single data point at a 30%-pop multiple. The clean expressions stay upstream (TSM BUY 7.4; MU now HOLD on valuation). Alphabet’s $80B equity raise and AI debt reaching 15% of the corporate bond market quantify that the buildout is now financed at a scale that competes with Treasuries and concentrates a new fragility vector into credit. Maintain GOOG bullish (do not raise on the dilutive raise); ORCL stays the leveraged-fragility short leg of GEV-vs-ORCL. AVGO earnings remain the key test for the first deceleration signal.

SpaceX June 12: Variance Event, Valuation Gap Widens

Morningstar values SpaceX at under half its $1.75T target, citing xAI uncertainty and an indeterminate moat. Combined with the New Glenn pad explosion and the disclosure discrepancy, the QQQ direction around June 12 is ambiguous; treat it as a variance event. AT&T’s downgrade on Starlink broadband competition and the UK’s Starshield military adoption add a second data point to the space-broadband-disruption theme (pressuring terrestrial broadband; SATS already AVOID). The semiconductor-correction setup (40-50% within 2-4 weeks) remains intact regardless of SpaceX direction.

Consumer: Macy’s Beat Is Execution, Not Demand Strength

Macy’s posted its strongest Q1 in four years and raised guidance, an idiosyncratic turnaround analogous to VSCO +40%, not category-wide demand strength. It diverges from but does not contradict the Gap/Old Navy mid-market crack (different cohorts) and may itself reflect higher-tier trade-down. Consumer Discretionary stays BUY-prohibited; H2 cliff 45-55%. Express via PGR over COF. Q2 earnings remain the test for whether the Gap crack spreads.

Continuing Themes

Small-cap: IWM OI P/C at 2.06 (highest among US-equity ETFs) with near-term IV normalized to 18.6% (fair vs 19.1% HV). Structural put dominance intact; July 2 $260 put thesis live. Continue to avoid.

Japan/yen: Yen at 160 with softened intervention rhetoric and a $19B fuel-subsidy budget; EWJ 1-month put skew +13.1% in backwardation. Carry-unwind/UST-repatriation risk intact. Financial-stress thesis unchanged.

Defense: Starshield UK adoption and the Kuwait intercept confirm multi-vector demand; overweight maintained (RTX, NOC, GD, LMT, MSI). No change.

Gold: GLD near-term IV cheap at 21.0% (vs 26.8% HV); real-yield channel dominates the safe-haven function as the strong dollar and rate-hike fears weigh. No thesis change.

CF Industries: No new data point; tactical HOLD (6.0). Clean exit if Hormuz physically reopens.

Crypto: Bitcoin below $70K plus Treasury sanctions on Iran’s largest crypto exchange and CLARITY Act progress; regulatory framework advancing but no portfolio-relevant change.

The options complex tells a layered story worth positioning around: EEM’s near-term IV at 36.6% against 20.0% HV (+16.6pp) in steep backwardation is the cleanest expression of the Hormuz binary, while HYG’s contango (2.5% near vs 7.6% 12-month, OI P/C 3.91) prices the credit cascade into H2 2026-H1 2027 — exactly the window the named private-credit gating now corroborates. TLT’s call-heavy OI P/C of 0.75 is the dovish-Warsh June-18 bet now fighting strong labor data, and a hike against a crowd priced at 37% would gap the 2Y toward 4.5%. The premium section maps how to hold energy through the whipsaw, express the redemption crisis via the permanent-capital pairs, and frame the eight risk scenarios — from the $150-160 oil failure tail to the Japanese carry unwind at 160 — into actionable positioning. Full options positioning analysis, portfolio playbook, and risk scenario framework below for subscribers.

This publication is for informational and educational purposes only and does not constitute financial, investment, or trading advice. The analysis, opinions, and commentary presented here should not be interpreted as a recommendation to buy, sell, or hold any security. Always conduct your own research and consult a qualified financial advisor before making investment decisions. Past performance does not guarantee future results.