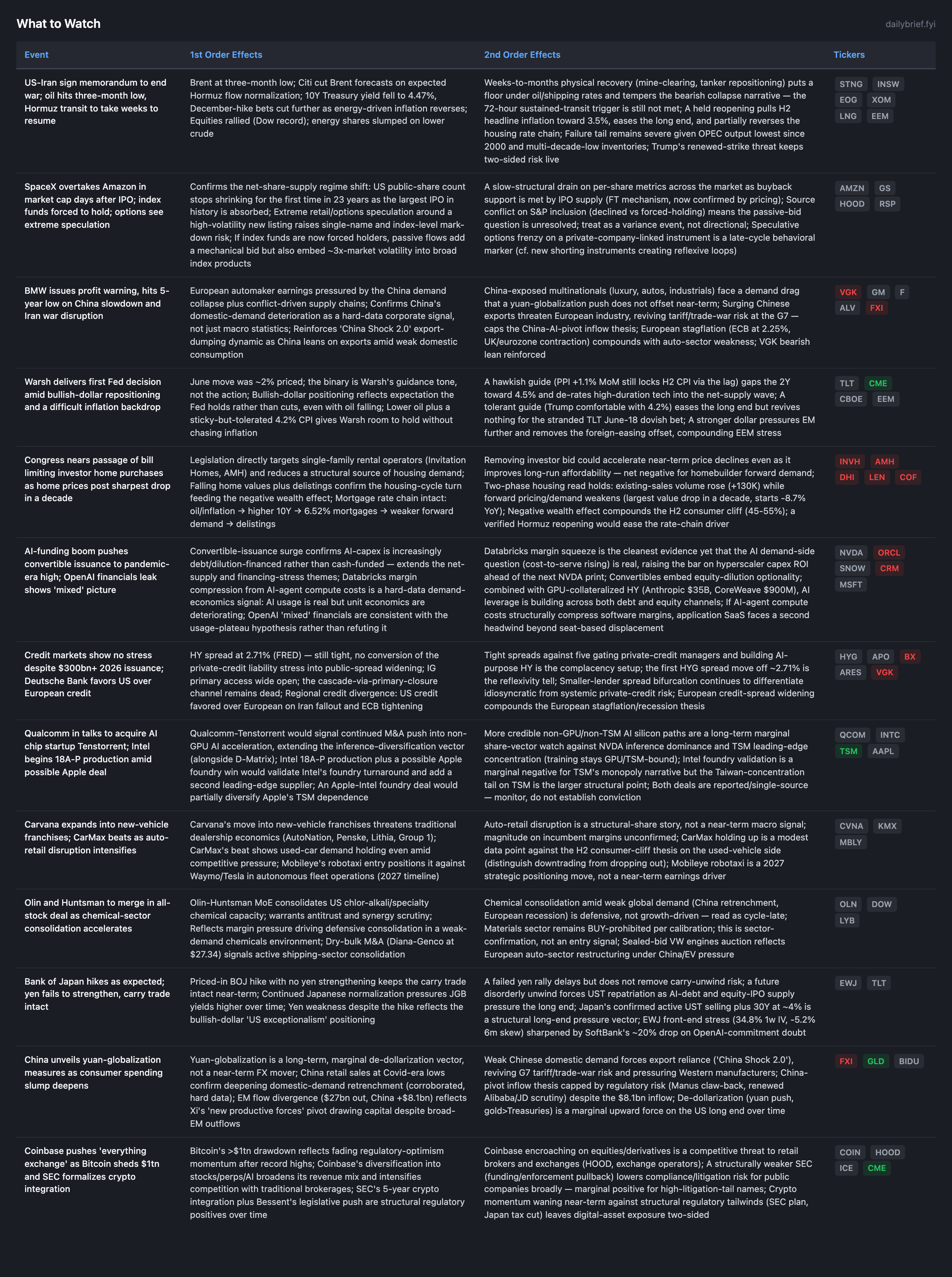

Iran War Memorandum Triggers First Verifiable Tanker Exit in 23 Cycles, But Hormuz Transit Stays Weeks Away

The two binaries that dominated last week resolved further in the directions the briefs positioned for, though neither is fully closed. On Iran, a signed memorandum to end the war arrived alongside the first genuinely verifiable action in 23 cycles: three Iranian tankers carrying ~5M barrels physically exited the US blockade, and Brent settled at a three-month low. The verification discipline still holds because the world’s largest tanker operator says normal Hormuz transit will take weeks and regional output recovery weeks to months, so the 72-hour sustained-transit trigger is not yet met, and Trump simultaneously threatened renewed strikes and disavowed the reported $300bn fund. The distribution has shifted materially toward a held reopening, but energy stays HOLD until physical transit verifies. On rates, Warsh’s inaugural FOMC arrived with the June move ~2% priced and the binary on guidance tone; the new wrinkle is a bullish-dollar “US exceptionalism” trade betting the Fed holds even as oil falls.

The new signal is on the AI demand side. Databricks reported >80% revenue growth to $6.9B annualized but explicitly flagged that AI-agent usage is significantly increasing costs and compressing margins. This is the cleanest hard-data evidence yet that the AI demand-economics question (rising cost-to-serve) is real, and it stacks on the single-source OpenAI usage-plateau hypothesis and “mixed” leaked OpenAI financials. Per the lesson to weight demand-side AI stress more heavily than financing-side stress, this is the higher-leverage development of the day, and it raises the bar further on the next NVDA print. Convertible issuance hitting a pandemic-era high confirms AI-capex is increasingly debt/dilution-financed. A new regulatory vector also emerged: Congress is near passage of a bill restricting investor home purchases, directly threatening single-family rental REITs into an already-turning housing market.

Databricks Margin Compression Is the Cleanest AI Demand-Economics Signal Yet

Databricks reported revenue growth exceeding 80% to $6.9B annualized, driven by AI-agent activity, while flagging that the same AI-agent usage is significantly increasing costs and compressing margins (CNBC, Tier 2). This is a single hard-data point, but it is the first that directly addresses the demand-side economics question rather than the financing side. The mechanism: AI agents consume far more compute per query than traditional software, so revenue growth that looks healthy at the top line carries a rising cost-to-serve that compresses unit margins.

This cuts two ways, and the distinction matters. For compute and memory demand, more agent usage means more inference cycles, which is demand-positive for silicon (the Jevons leg). For the AI application and software layer, structurally rising compute cost-to-serve is a second margin headwind beyond seat-based displacement, and it pressures the ROI math underwriting ~$920B of projected hyperscaler capex. This does not confirm the OpenAI usage-plateau hypothesis (Databricks usage is growing, not plateauing), but it confirms the adjacent and arguably more important point that AI-agent economics are margin-dilutive. The next NVDA/hyperscaler print now tests three things: chip-order supply, end-demand durability, and whether the unit economics support the capex. The leaked OpenAI financials (”not bad but not great”) and the pandemic-era-high convertible issuance round out a picture of an AI sector whose revenue is real, whose capital intensity is rising, and whose unit economics are under fresh scrutiny.

No position change: TSM, MSFT, GOOG remain the clean expressions, integrators stay neutral, NVDA stays HOLD with existing holders retaining and new capital waiting for the print. SNOW is confirmed on the infrastructure-wins side of the bifurcation; CRM weakens further as the application-layer short leg if compute cost-to-serve compresses SaaS margins.

Congress Near Passage of Investor-Home-Purchase Restriction

Top lawmakers reached agreement on a housing bill restricting investor ownership of single-family homes, clearing a path through both chambers (CNBC, Tier 2). This is a new regulatory vector that lands directly on single-family rental REITs (Invitation Homes, American Homes 4 Rent) into an already-deteriorating housing market. The mechanism is direct: removing the institutional-investor bid eliminates a structural source of demand, which can accelerate near-term price declines even as it improves long-run affordability.

The timing compounds the existing housing thesis. Home values posted their largest decline in nearly a decade, sellers are delisting at the fastest pace since 2020, and FRED shows housing starts falling to 1,177K (-215K MoM, -8.7% YoY) against the 30Y mortgage at 6.52%. The two-phase read holds: existing-home-sales volume rose to 4,170K (+130K) while forward pricing and starts weaken. For SFR REITs the bill is an asset-side and growth-model impairment; for homebuilders (DHI, LEN) it removes a demand source on top of the rate-chain drag. This reinforces the negative-wealth-effect leg of the H2 consumer cliff. A verified Hormuz reopening that pulls the 10Y and mortgage rates lower is the offsetting force to watch.

Trade-War Risk Revives as China Demand Collapses and Exports Surge

Three corroborated data points firmed the China-weakness cluster. BMW slashed guidance to a five-year low citing China slowdown plus Iran disruption (Reuters/CNBC, Tier 1-2); Chinese retail sales fell unexpectedly to Covid-era levels (NYT, corroborated, hard data); and surging Chinese exports raised “China Shock 2.0” fears at the G7. The causal chain is coherent: weak domestic demand forces China to lean on exports, which threatens European industry and revives tariff/trade-war risk. BMW is the corporate confirmation of the macro statistic, and it adds an auto-supply-chain read-through (ALV, GM, F).

This caps the China-AI-pivot inflow thesis. The $8.1bn that flowed into China in May (against $27bn out of broad EM) reflects Xi’s “new productive forces” high-tech-manufacturing pivot, but regulatory risk (the Manus claw-back, renewed Alibaba/JD scrutiny) and now demonstrably weak domestic demand limit how far that rotation runs. FXI options corroborate with a -7.8% 12-month put skew pricing demand-softening as longer-dated downside. Soft Chinese crude demand also caps the oil ceiling even on a Hormuz failure.

What to Watch

Developing Themes

Iran: Signed MoU and Physical Tanker Movement, But Transit Verification Still Weeks Away

The signal escalated in quality: a signed memorandum plus three tankers physically exiting the US blockade, the first verifiable action paired with a document in 23 cycles. Citi cut its Brent forecast. The discipline holds for a specific, evidence-based reason: normal transit takes weeks, regional output recovery takes weeks to months (mine-clearing, repositioning), and Trump both threatened renewed strikes and disavowed the fund. The weeks-to-months physical lag puts a floor under oil and shipping rates, which is why STNG/INSW stay two-sided rather than outright bearish. Energy remains HOLD, no add, no reduce. A held reopening pulls H2 headline inflation toward 3.5% and eases the rate chain; failure reopens the $150-160 tail given OPEC output at its lowest since 2000.

AI Capital-Markets Wave: Convertibles Join the Debt/Dilution Build

Convertible issuance hit a pandemic-era high (WSJ, Tier 2), adding equity-dilution-optionality financing to the GPU-collateralized HY (Anthropic $35B, CoreWeave $900M) and straight debt (Oracle $20B, Amazon C$14B) already tracked. AI-capex is increasingly funded by debt and dilution rather than cash flow across all three channels. Sify’s paused $391M India data-center IPO signals selective cooling in data-center capital appetite. The net-supply theme is confirmed by SpaceX overtaking Amazon in market cap days after its IPO, though today’s report that index funds are “forced to hold” SpaceX conflicts with the prior brief’s report that the S&P committee declined inclusion; treat the passive-bid question as unresolved and the event as variance rather than directional.

Private Credit: Spreads Still Tight, Complacency Setup Intact

FRED HY spread at 2.71% (-0.05) confirms no conversion of the five-manager gating sequence into public-spread widening. MarketWatch explicitly flags complacency given $300bn+ of 2026 issuance absorbed on AI optimism. Deutsche Bank’s US-over-European credit call adds a regional dimension that reinforces the European-weakness thesis. The first HYG spread move off ~2.71% remains the reflexivity tell; Fed stress-test results June 24 are the near-term bank-credit input. Hold APO/ARES over BX/OWL.

Continuing Themes

Rates: Do not pre-position into the Warsh FOMC outcome. June move ~2% priced; binary is guidance tone. 10Y at 4.47%, 2Y at 4.07% (FRED). Bullish-dollar positioning bets the Fed holds. Let CME/CBOE carry the vol.

European stagflation: ECB at 2.25%, UK/eurozone contraction, BMW warning, Deutsche Bank flagging euro-credit widening. VGK bearish lean reinforced; options rich at 25.2% near-term in backwardation.

Power/electrical: GEV, CEG, VST, ETN overweight intact (Siemens Energy AI gas-turbine demand, Eaton-Dana). GEV-vs-ORCL pair CORE; Oracle’s negative FCF confirms the short leg.

Consumer: Housing rate chain plus the new investor-purchase bill against the existing-home-sales counter-point (4,170K) — two-phase read. BofA card data shows discretionary spending holding (counter-point); CarMax beat (used-car demand holding). H2 cliff 45-55%. PGR over COF, extending to SYF/RDN. Consumer Discretionary BUY-prohibited.

Crypto: Bitcoin down >$1tn from highs; momentum waning against structural regulatory positives (SEC 5-year plan, Japan tax cut). No portfolio-relevant change.

Defense: US multi-front demand intact and separate from the unwinding European fiscal-funding trade. Watch autonomy share-shift (AVAV, KTOS).

Healthcare M&A: LLY/4E Therapeutics (non-opioid pain) and Altaris/Simulations Plus continue the consolidation bid; supports LLY and differentiated mid-caps (NBIX).

The options structure sharpens where the actionable edge sits: EEM is the most-stressed complex at 44.9% near-term IV against 21.9% HV — a 23.0pp spread, the widest in the set — and still has not bought the signed Iran MoU, making it the cleanest binary relief vector. Beneath the FOMC front-end noise, the durable signals are small-cap structural put OI (IWM P/C 2.49), the H2 credit window (HYG OI P/C 3.84) sitting against a deceptively tight 2.71% spread, the stranded TLT dovish bet, and an EWJ carry-unwind watch sharpening to a -5.2% 6-month put skew. The premium section maps these into a ten-point portfolio playbook — where to hold, where the bearish leans reinforce, and where not to pre-position — alongside an eight-scenario risk framework headlined by the widening AI demand-economics crack. Full options positioning analysis, portfolio playbook, and risk scenario framework below for subscribers.

This publication is for informational and educational purposes only and does not constitute financial, investment, or trading advice. The analysis, opinions, and commentary presented here should not be interpreted as a recommendation to buy, sell, or hold any security. Always conduct your own research and consult a qualified financial advisor before making investment decisions. Past performance does not guarantee future results.