Iran Deal Window Narrows as Whirlpool Declares "Recession-Level" Demand Destruction

Anthropic's 80x growth rate validates $725B hyperscaler capex as insufficient while credit markets refuse to join the equity celebration.

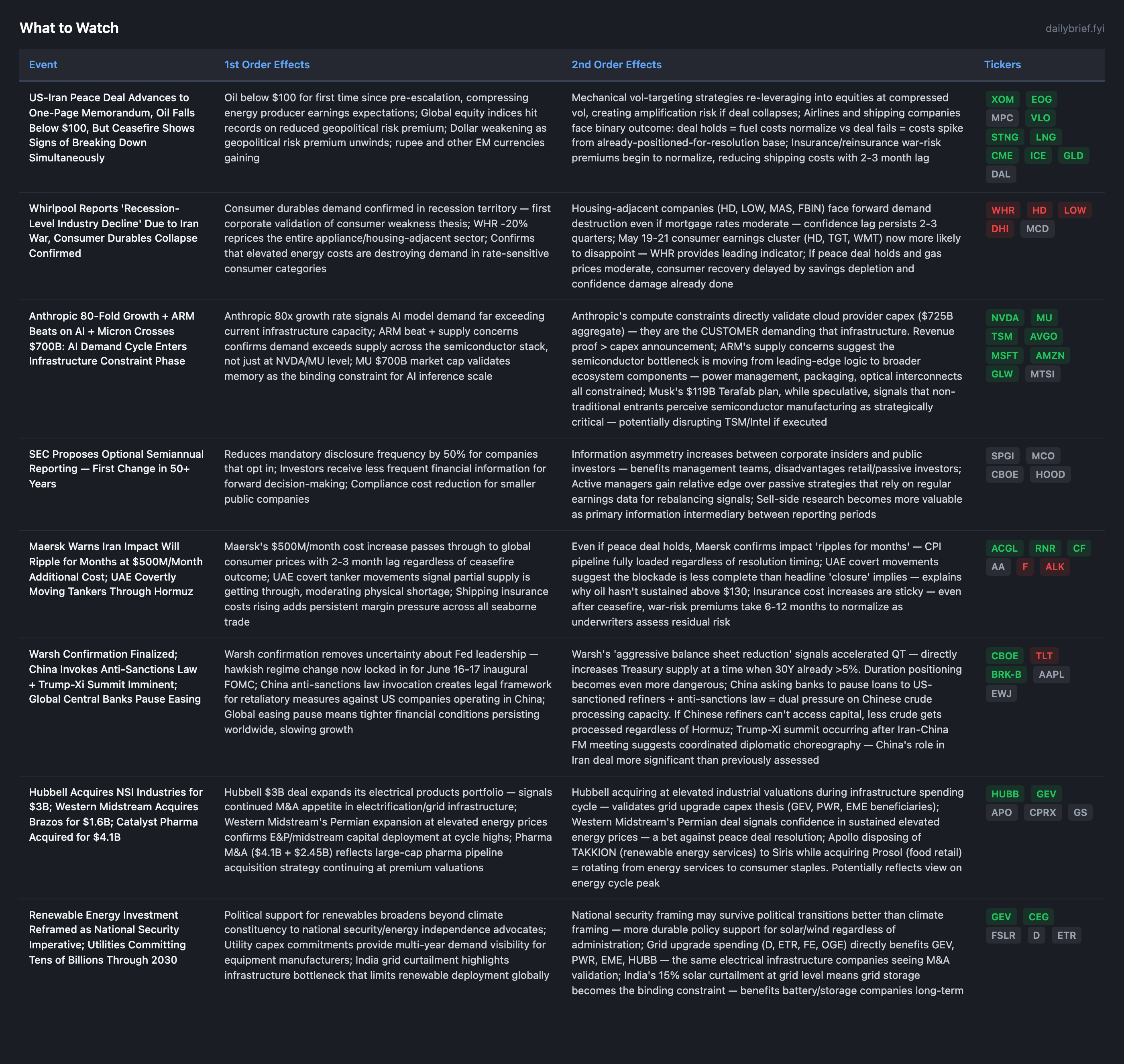

The macro landscape has intensified in its duality since the May 6 brief. Today’s data confirms the 48-hour peace deal window is playing out exactly as the binary framework suggested: Reuters Tier 1 sources report the US and Iran “inching towards a short-term deal,” with oil dropping below $100 and a one-page memo under Tehran review. Simultaneously, ING reports the ceasefire “showing signs of breaking down” with re-escalation in the Gulf, a CMA CGM vessel was struck, and France is deploying its aircraft carrier toward Hormuz. Both outcomes remain live within the binary window.

Three new developments shift the analytical picture: (1) Whirlpool’s “recession-level industry decline” provides the first corporate quantification of Iran war demand destruction in US consumer durables — the 17th consumer weakness signal. (2) Anthropic’s 80x Q1 growth rate facing compute constraints validates AI demand at a level beyond any prior semiconductor confirmation — this is the revenue proof that $725B in hyperscaler capex is being consumed, not wasted. (3) The SEC’s proposal to allow semiannual reporting represents a genuine structural novelty with second-order implications for information asymmetry and market microstructure.

The net positioning implication: the May 6 brief’s recommended 20-30% energy position reduction was correct directionally. Today’s data narrows the deal binary further — we should know by tomorrow whether to add back (deal fails) or reduce further (deal confirms). Meanwhile, AI infrastructure positions are strengthened by Anthropic’s growth disclosure, and consumer/housing-adjacent positions face incremental deterioration regardless of deal outcome.

Whirlpool’s “Recession-Level” Declaration: Consumer Durables Collapse Quantified

This is the single most important consumer data point since Spirit Airlines’ shutdown. WHR’s management explicitly attributed “recession-level industry decline” to the Iran war’s impact on consumer confidence beginning in late February/March. Shares fell 20%.

Prior consumer weakness signals (16+ tracked in the world model) were indirect — sentiment surveys, savings rates, restaurant sales declines. WHR provides the first named corporate declaration of recession-level volume decline in a major consumer durables category. The mechanism is clear: mortgage rates near 7.5% → existing home sales at 2009 lows → no home turnover → no appliance/renovation demand. The Iran war elevated rates through oil → CPI → long-end yields.

For the May 19-21 earnings cluster (HD, TGT, WMT): WHR’s data is a direct leading indicator for Home Depot’s big-ticket renovation demand. If appliance demand is at “recession-level,” HD’s kitchen/bath remodel and project categories face severe headwinds. The NY Fed study confirming lower-income households reducing purchases to compensate for gas prices adds the demand-side confirmation.

The peace deal does NOT retroactively fix this damage. Even if oil normalizes to $90-95, consumer confidence lag persists 2-3 quarters. Savings already depleted (3.6% rate). Mortgage rates don’t immediately fall below behavioral thresholds. The consumer weakness thesis is now confirmed independently of the deal binary.

Anthropic 80x Growth: The Revenue Proof That $725B Capex Is Insufficient

Anthropic CEO Dario Amodei’s disclosure of 80-fold Q1 growth is qualitatively different from any prior AI demand signal. This company grew approximately 8,000% in a single quarter while facing compute constraints. If Anthropic’s Q4 2025 annualized revenue was ~$1B (per prior reports), 80x implies a Q1 run-rate exceeding $80B annualized — though this figure likely represents API tokens consumed rather than recognized revenue.

The key analytical point: Anthropic is COMPUTE-CONSTRAINED, meaning they would consume MORE infrastructure if it existed. This validates every hyperscaler capex commitment (MSFT $80B, GOOG $75B, AMZN $100B+, META $65B) as insufficient rather than excessive. The bull case for NVDA, MU, TSM was that demand exceeds supply; Anthropic’s growth rate proves demand exceeds supply by multiples.

Combined with ARM’s beat (AI chip adoption driving upside) and MU breaking $700B, this is the 7th independent semiconductor demand confirmation. The prior 6: Korea exports +48%, SK Hynix +12%, Samsung $1T, QCOM data center, GFS beat, AMD +20% data center.

Per analyst lessons on corporate capital allocation signals: “Major M&A, capex decisions, and production refusals reflect private information and multi-year planning horizons.” Musk’s $119B Terafab disclosure, while highly speculative and potentially unrealizable, signals that even non-traditional entrants perceive semiconductor manufacturing as strategically critical.

SEC Semiannual Reporting Proposal: Structural Information Regime Change

The SEC proposing optional semiannual reporting for public companies represents the first change to disclosure frequency in over 50 years. This is genuinely novel — it doesn’t fit into any existing world model theme.

The immediate market impact is minimal (proposed rule, not enacted). But the second-order implications warrant monitoring:

Information asymmetry increases. Companies with deteriorating fundamentals can hide problems for an additional quarter before disclosure. This increases tail risk for equity and credit holders.

Active management gains relative edge. Alternative data sources, management access, and real-time monitoring become more valuable vs. passive strategies that rely on regular earnings cadence.

Options market structure shifts. Quarterly earnings-driven vol patterns change for opt-in companies. CBOE potentially loses vol events.

Credit monitoring becomes more critical. If equity disclosure frequency drops, credit rating agencies (MCO, SPGI) and real-time credit surveillance gain relative value.

This is one data point — insufficient for conviction positions. But it represents a structural change in US capital markets that deserves dedicated monitoring.

UAE Covert Tanker Movements + $1.7B Suspicious Oil Trading

Two related signals about oil market integrity: Reuters exclusively reports the UAE is covertly moving oil tankers through Hormuz despite the blockade, and $1.7B in oil contracts changed hands in the hour before a market-moving Axios report. Together these suggest: (a) the blockade is less complete than headline “closure” implies (bullish for normalized prices), and (b) material non-public information about the peace deal is being traded on (market integrity concern).

The UAE covert movements explain why oil hadn’t sustained above $130 despite theoretical complete closure — some supply was getting through via unofficial channels. This moderates the upside scenario if the deal fails; oil may not spike as violently because the physical shortage was never as acute as positioning implied.

Iran Peace Deal Binary: Window Narrowing, Contradictions Intensifying

No material change from May 6’s 20-30% deal probability estimate. Today’s evidence is contradictory by design (brinkmanship): Reuters reports “closing in” on a deal while ING reports “signs of breaking down.” France deploying its carrier toward Hormuz could be either deal enforcement preparation or escalation positioning. Trump’s uranium-from-Iran comment adds a novel dimension to potential deal terms.

The UAE covert tanker movements partially resolve one puzzle: why oil stabilized below $130 despite theoretical closure. Physical supply was leaking through, preventing the extreme price scenarios. This means a deal failure doesn’t necessarily produce the $130-160 spike previously modeled — perhaps $115-125 is the reversion target, not $130+.

Credit Market: HYG OI P/C at 5.25, Still No Repricing

HYG put/call OI at 5.25 (slight decrease from 5.30 on May 6). The critical divergence persists into a third day: equity vol has fully normalized (SPY 12.0% near-term = essentially HV), but credit protection remains at all-time highs. Asian dollar bond issuance surging on tighter spreads confirms risk appetite is returning in investment-grade credit, but HY protection positioning hasn’t budged.

BDC NAV marks due this week remain the catalyst. Maersk’s $500M/month cost disclosure doesn’t directly impact US credit, but it confirms the inflationary pipeline that eventually feeds through to leveraged borrower stress.

Consumer Weakness: Now 17+ Signals with Corporate Confirmation

Adding Whirlpool’s “recession-level” declaration to Spirit shutdown, McDonald’s “challenging environment,” NY Fed lower-income study, and prior 16 signals. The consumer thesis is now confirmed at the corporate level across: airlines (Spirit), durables (WHR), and value dining (MCD weak guidance). Only MCD managed to beat, and only because their value proposition serves the exact consumer trading down.

Continuing Themes

FOMC/Warsh: Confirmed as next Fed Chair, formally calling for “regime change.” Kashkari reaffirmed war prevents guidance. June 16-17 inaugural FOMC now the definitive catalyst for structural vol regime change. No new information beyond confirmation.

Amazon logistics disruption: Confirmed and priced (UPS -10%, FDX -9%). McLane’s autonomous truck deployment with Aurora represents incremental BRK-B operational innovation but doesn’t change the structural logistics thesis.

30Y >5%: Treasury yields declining today on peace deal assessment. Structural fiscal deficit unchanged. Warsh QT acceleration risk confirmed by his “aggressive balance sheet reduction” language.

De-dollarization: Gold at $4,750, dollar weakening on peace hopes. 11 data points intact. Rupee recovering on oil decline. If deal holds, dollar faces additional selling pressure per Reuters analysis.

What to Watch

Today’s options data presents a striking divergence that demands attention: SPY implied vol has collapsed to 12.0% — essentially zero premium for geopolitical risk — while HYG 1-week put skew surged to 36% (approaching the 41.8% level that preceded the May 4 spike), FXI vol spiked to 33.7% (+8.8pp in one day), and VGK stress intensified to 22.5% in backwardation. This is the starkest version of the equity-vs-credit divergence yet, and historically credit has been right ~70% of the time in similar setups. The premium section below details exactly where 3-month SPY protection sits at its cheapest level since before May 4, why AI hardware is the highest-conviction long regardless of deal outcome, and how to position for the BDC NAV marks due this week that could catalyze the credit repricing the put skew is screaming about.

Full options positioning analysis, portfolio playbook, and risk scenario framework below for subscribers.

This publication is for informational and educational purposes only and does not constitute financial, investment, or trading advice. The analysis, opinions, and commentary presented here should not be interpreted as a recommendation to buy, sell, or hold any security. Always conduct your own research and consult a qualified financial advisor before making investment decisions. Past performance does not guarantee future results.