Investment Research Report: Assured Guaranty Ltd (AGO)

Executive Summary

Assured Guaranty is a financial guaranty insurer trading at approximately 46% of its Adjusted Book Value ($186.43/share vs. ~$87 market price), with a near-monopoly position in structured finance guarantees and 58% market share in U.S. municipal bond insurance. The company has retired 81% of shares outstanding since 2013 at an average cost of $37.73/share, and continued purchasing $500M (11.5% of shares) in 2025 alone at ~$86/share.

The stock has declined over the past three months, coinciding with broader municipal credit concerns as 30-year Treasury yields have breached 5% and tightening credit spreads that compress premium pricing. Options market data suggests elevated near-term volatility expectations relative to realized volatility, indicating possible catalyst concerns.

Despite these headwinds, the magnitude of the discount to intrinsic value (approximately $100/share gap to ABV), the mechanical compounding from aggressive buybacks, and the embedded $3.4B in net deferred premium revenue in excess of expected losses provide a sufficient margin of safety to recommend the stock as a BUY at current levels, with a base case target of $100-105.

Company Overview

Assured Guaranty Ltd is a Bermuda-domiciled, U.K. tax-resident holding company that provides unconditional and irrevocable guarantees on debt instruments, primarily U.S. municipal bonds, U.K./international infrastructure debt, and structured finance transactions. The company collects premiums upfront or over time in exchange for guaranteeing scheduled principal and interest payments if an issuer defaults.

Business Segments:

Insurance (core): Financial guaranty across U.S. public finance ($265.6B net par outstanding), non-U.S. public finance (primarily U.K. regulated utilities), and global structured finance ($11.5B net par)

Asset Management: ~30% ownership in Sound Point Capital ($44B+ AUM), contributing fee-based income

Life & Annuity Reinsurance (new): Acquired Assured Life Re in January 2026 for $158M, entering U.K. pension risk transfer and U.S. guaranteed annuity reinsurance

The company operates with approximately 360-370 employees managing $277B in total net par outstanding and an $8.5B investment portfolio.

Financial Analysis

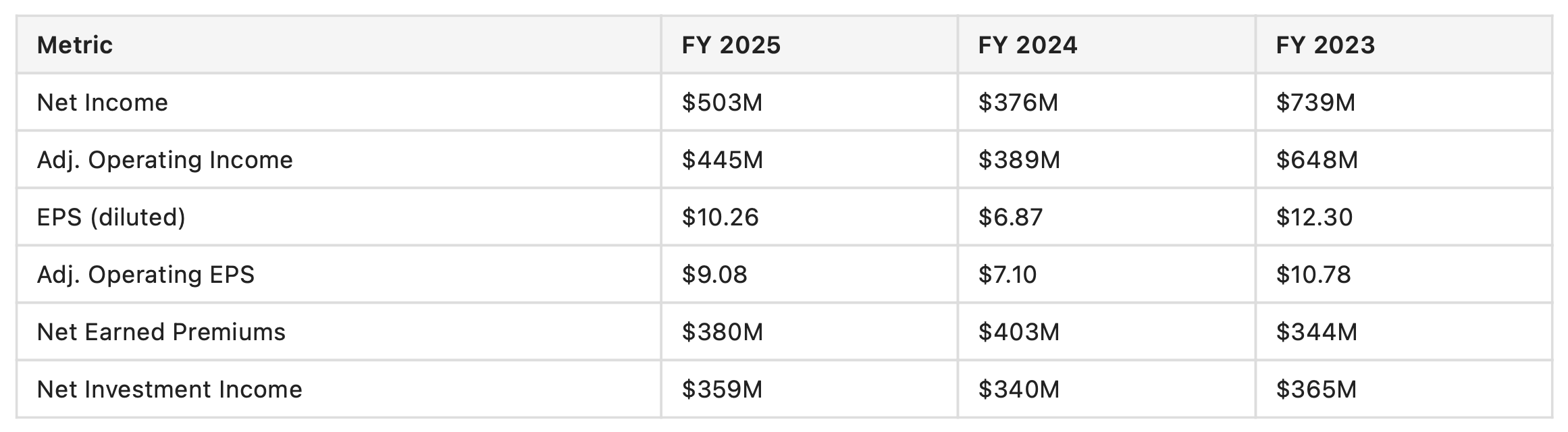

Headline earnings volatility is misleading. GAAP results include FX remeasurements, fair value changes on consolidated VIEs, and litigation recoveries ($103M LBIE settlement in 2025). Underlying scheduled premiums are growing steadily: U.S. public finance scheduled premiums rose from $252M → $264M → $279M over 2023-2025. Net investment income benefits from rising portfolio yield (4.76% vs. 4.57% prior year).

The recent earnings beat/miss pattern shows 3 beats in 4 quarters. The Q2 2025 miss coincided with a period where adjusted operating income declined to $50M ($1.01/share) from $80M ($1.44/share) in Q2 2024, reflecting credit reserve additions and lower production economics rather than fundamental business deterioration.

Balance Sheet:

At December 2025: shareholders’ equity of $125.32/share, Adjusted Book Value of $186.43/share. The gap between market price (~$87) and ABV ($186) reflects: (1) $3.367B in net deferred premium revenue on financial guaranty contracts in excess of expected losses to be expensed, (2) net present value of future installment premiums ($194M), and (3) embedded investment income on reserves yet to run off. The company notes that actual realization of these amounts may differ materially due to FX fluctuations, prepayments, terminations, credit defaults, and other factors.

Long-term debt stands at $1.7B against a $12.2B asset base and $8.5B investment portfolio. The company recently gained access to $300M in FHLB collateralized borrowings, adding liquidity flexibility.

Capital Return — The Core Value Creation Mechanism:

Since 2013, AGO has repurchased 157 million shares for $5.9B at an average price of $37.73/share. This has compounded ABV per share by approximately $117. In 2025 alone, the company retired 5.82M shares ($500M at avg $85.92) — 11.5% of outstanding. Authorization remaining as of February 2026: $204M, with the board regularly authorizing additional tranches ($300M in August 2025, $100M in November 2025).

At current prices well below ABV, buybacks are accretive to remaining shareholders: each share retired at a discount to ABV distributes the differential across the remaining share base. This mechanical accretion continues as long as the stock trades materially below book value, and has been the primary driver of per-share value growth over the past decade.

Growth Analysis

Growth at AGO comes from three sources: (1) new premium production, (2) investment portfolio returns, and (3) per-share compounding via buybacks.

New Business Production:

Gross par written grew 13.5% over two years, but premium value declined because tighter credit spreads reduced per-par pricing. The BBB-AAA municipal spread averaged only 89bps in 2025 (vs. 101bps in 2023). This is the primary cyclical headwind: tight spreads reduce the economic value proposition of insurance.

However, the current macro environment — with 30-year rates above 5% and rising recession probability — is likely to widen municipal credit spreads over the coming 6-12 months. Wider spreads historically increase both insurance penetration rates and premium pricing. Municipal insurance penetration by par declined from 8.8% to 7.5% (2023-2025) during the tight-spread environment; a reversal in spreads could push penetration back toward historical averages (10-12% during stressed periods).

Diversification Initiatives:

Sound Point ownership (~$44B AUM) provides fee income independent of the insurance cycle

Assured Life Re ($158M acquisition) opens U.K. pension risk transfer and U.S. annuity reinsurance — early stage but additive if executed well

Australia/Singapore offices expanding geographic reach for infrastructure guarantees

Fund finance developing as a “flow business” in structured finance

Estimate Revisions:

Current-year EPS estimates have seen modest downward revisions over recent months, reflecting reduced premium expectations from tight credit spreads and potentially modest credit reserve additions. The negative revision momentum is a near-term headwind to sentiment but modest in absolute terms.

Valuation Assessment

Absolute Valuation:

P/E: approximately 8.5-9.5x trailing, ~12.5x forward consensus

P/ABV: approximately 0.46-0.47x (~$87 / $186.43)

P/Book: approximately 0.69x (~$87 / $125.32)

Dividend yield: ~1.7%

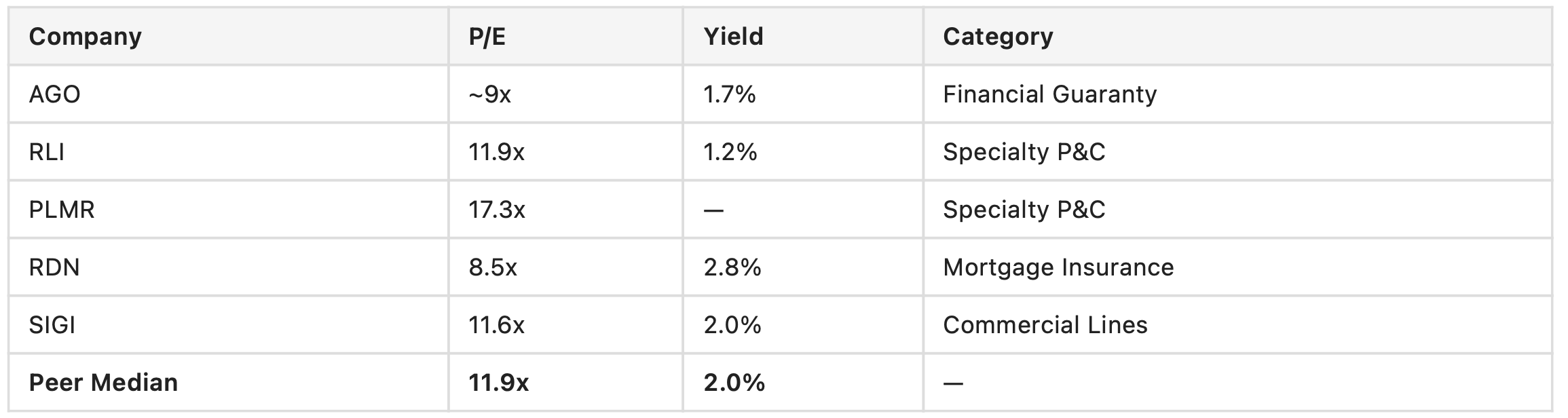

Relative to Peers:

AGO trades at a meaningful discount to specialty insurance peer median P/E. This discount is partially structural — financial guaranty insurers carry long-tail credit risk that P&C insurers don’t, and the peer set is imperfect given AGO’s unique business model — but the current magnitude appears excessive given: (1) the company has $3.4B in deferred premium revenue in excess of expected losses yet to be recognized, (2) the insured portfolio has survived Puerto Rico, Detroit, and multiple stress periods, and (3) annual credit loss development has been modest relative to par outstanding.

Why the Market May Be Wrong: The stock trades as though material credit losses are probable, yet the company’s loss experience remains low relative to par outstanding. The buyback program creates mechanical per-share value growth of 10-12% annually at current pace and pricing. Analyst consensus targets imply meaningful upside — and these targets don’t assume spread widening benefits.

The most comparable metric is P/ABV: at approximately 0.46x, the market prices in either substantial future losses or a permanent inability to monetize the embedded value. Given that the company distributes value through buybacks (not requiring the stock to trade at book), the embedded value is accessible regardless of the market’s valuation.

Competitive Landscape

AGO operates in a near-duopoly in U.S. municipal bond insurance (58.5% market share, BAM at approximately 42%) and a monopoly in global structured finance guarantees. Barriers to entry are extreme: a new entrant would need multiple AA-level ratings, billions in capital, decades of claims-paying track record, and regulatory approvals across multiple jurisdictions.

The competitive position is stable to slightly improving:

No new competitor has entered since 2012

AGO maintains ratings from three agencies (S&P AA, KBRA AA+, Moody’s A1) vs. BAM’s single S&P rating

The company’s track record of claims payment and recovery through Puerto Rico and Detroit provides credibility that would take years for any new entrant to build

Structured finance guaranty business has no active competitor

Trajectory: The company is expanding into new geographies (Australia, Singapore) and adjacent business lines (life/annuity reinsurance, fund finance) without losing share in core markets. Competitive position is improving through diversification while maintaining dominance in the core.

Risk Assessment

1. Thames Water ($2.4B net par, rated B internally): The largest identifiable concentration risk. Thames Water faces severe financial stress with owners withdrawing support and potential government intervention. Loss development of $33M was recorded for U.K. regulated utility exposures in 2025. A full default scenario on $2.4B would consume significant capital and depress earnings for multiple years. While the company has substantial claims-paying resources, the report does not have sufficient visibility into debt-service timing, recovery assumptions, reinsurance offsets, or rating-agency capital impact to fully quantify the downside. This remains a material tail risk that warrants close monitoring.

2. Rising Long-term Rates and CRE/Municipal Stress: With 30-year Treasuries above 5%, municipalities face higher refinancing costs. This creates a dual effect: wider spreads increase insurance demand and pricing (positive), but also increase the probability of actual credit losses on the insured portfolio (negative). Net effect is likely positive for AGO given the low historical loss rates in municipal finance, but tail risk is elevated.

3. PREPA ($464M net par): The sole remaining unresolved and defaulting Puerto Rico exposure with $106M in net par amortization and $126M in scheduled debt service due in 2026. While AGO successfully resolved other Puerto Rico credits, PREPA remains outstanding with $537M in total scheduled net debt service. Resolution has been perpetually delayed, and additional reserve development is possible.

4. Credit Spread Sensitivity: If spreads tighten further (unlikely given macro), premium pricing and penetration would continue declining.

5. Bermuda CIT (15%): New permanent tax headwind for AG Re effective 2025. Phase-in provides temporary relief but represents structural margin compression.

6. New Business Execution: Assured Life Re ($158M) enters competitive annuity reinsurance with different risk characteristics (longevity, mortality). Integration and underwriting discipline in unfamiliar territory are legitimate concerns.

Options Market Signal

Available market data suggests elevated near-term implied volatility relative to realized volatility, with put-heavy positioning indicating defensive sentiment. The term structure appears to be in backwardation, suggesting a specific near-term catalyst concern rather than structural deterioration.

This diverges from the fundamental thesis. Possible explanations include concern over municipal credit deterioration from rising rates, or specific hedging around Thames Water developments. For outright equity holders, the near-term volatility is informational but shouldn’t override the deep value thesis given a 12-month horizon.