Higher-for-Longer Confirmed as 3.8% CPI Collides with Expanding Gulf Conflict and Retail Euphoria

Corporate treasuries are rushing to lock in rates at a six-year pace while retail investors buy calls at 2021 levels — the two sides of the market are pricing fundamentally different futures

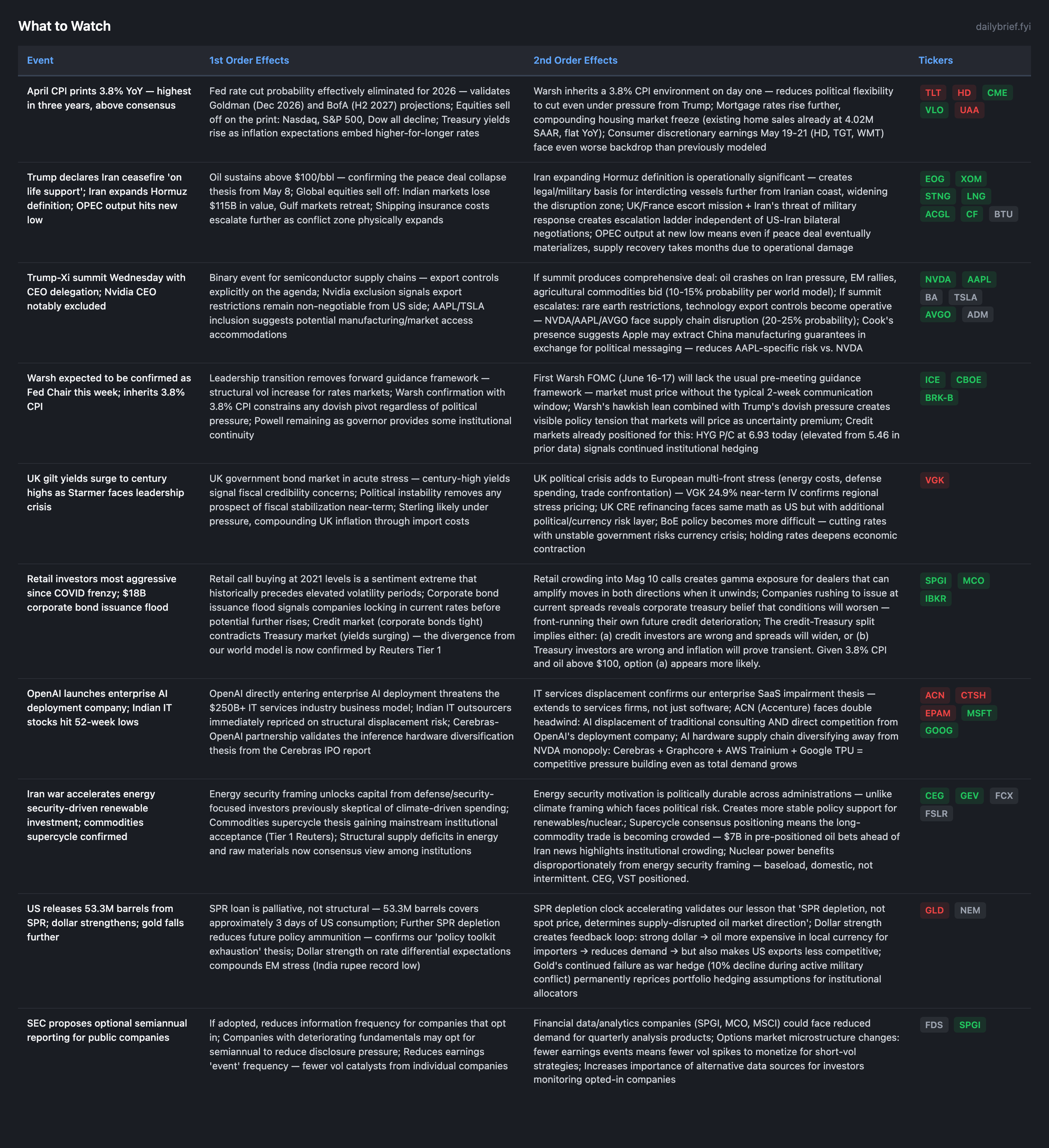

The dominant development since the May 11 brief is the April CPI print at 3.8% YoY — the highest in three years, confirming our >80% probability estimate and validating the persistent inflation thesis. This arrives simultaneously with Trump declaring the Iran ceasefire “on life support,” Iran physically expanding its Hormuz zone definition, and OPEC output hitting a new low. The trifecta eliminates any remaining ambiguity about the rate path: higher-for-longer is confirmed, the inflation pipeline remains full, and Warsh inherits a 3.8% CPI environment when confirmed this week.

Retail call buying in Mag 10 stocks is at the highest level since the 2021 COVID frenzy (per Cboe’s own data), while $18B in corporate bonds were issued in a single day as companies rush to lock in current rates. Corporate treasuries are front-running future deterioration while retail equity positioning reflects euphoria — the two sides of the market are pricing fundamentally different futures.

April CPI at 3.8%: The Prior Brief’s >80% Probability Realized

The world model estimated >80% probability of April CPI exceeding 4.0%. The actual print of 3.8% is slightly below that threshold but above the 3.7% consensus — confirming the directional thesis while landing in the “hot but not panic-inducing” zone. FRED data shows CPI at 332.41 (April), up 2.11 from March, with Core CPI at 335.42 (+1.26 MoM). Five-year breakevens at 2.67% (+0.05 on May 11) confirm markets embedding continued inflation.

The “persistent” interpretation dominates over “peak” because (a) the peace deal collapsed, (b) oil remains above $100, (c) Iran expanded its Hormuz zone, and (d) no policy mechanism exists to suppress energy prices. The world model’s H2 central case of 4.5-5.0% CPI remains intact. Warsh’s first FOMC (June 16-17) will face a choice between acknowledging the inflation reality (potentially hiking) or preserving political flexibility (holding and hoping). Either choice has market consequences.

Iran Expands Hormuz Definition: Operational Escalation

Iran’s IRGC redefining the Strait of Hormuz as a “far larger zone” is operationally significant in ways the headline understates. This creates a legal and military basis for interdicting vessels further from the Iranian coast, physically widening the disruption zone. Combined with Kuwait intercepting hostile drones, Qatar reporting vessel attacks, and the UK/France planning a multinational escort mission that Iran has explicitly threatened to resist militarily — the conflict is expanding geographically even as diplomatic channels close.

The mechanism: wider interdiction zone → more vessels require alternative routing or escort → higher insurance costs → more supply disruption → higher prices even without additional military strikes on infrastructure. This is an escalation of capability, not just rhetoric.

Retail Euphoria at 2021 Levels: A Contrarian Warning

Cboe’s data showing retail call buying in “Mag 10” stocks at the heaviest 10-day clip since 2021 is the single strongest sentiment extreme indicator in today’s data. Historically, retail options euphoria of this magnitude has preceded drawdowns within 2-6 weeks (2021 peak preceded Feb correction; March 2000 peak preceded April-May selloff). The mechanism: retail call buying forces dealers to buy stock as delta hedges → when sentiment reverses, dealers sell, amplifying the move down.

This does not guarantee imminent decline. But it confirms that the current AI-driven equity rally is being powered by speculative positioning rather than fundamental value discovery alone. Combined with SOX +50% in 25 trading days and the UBS “largely priced in” call from last week, the probability of a 10-15% semiconductor correction within 2-4 weeks rises from our prior 30-40% estimate toward 40-50%.

$18B Corporate Bond Issuance: Companies Front-Running Their Own Deterioration

Reuters reporting the largest single-day corporate bond issuance since Meta’s April 30 sale, with the busiest May in six years expected, reveals corporate treasury teams’ private assessment of the future. Companies lock in rates when they believe rates will rise or access may deteriorate. This issuance flood occurring while HY spreads remain tight (2.79% per FRED) and credit positioning is at record defensive levels (HYG P/C ratio now 37.09x in daily volume, 6.93x in OI) confirms the credit-equity disconnect is widening further.

Corporates agree with the credit market (conditions will deteriorate) while equity markets disagree (pricing in optimism). When the companies themselves are signaling urgency to borrow now, the credit repricing catalyst is closer than spreads currently reflect.

OpenAI Enterprise Deployment: IT Services Structural Disruption

OpenAI launching a dedicated enterprise AI deployment company is a new competitive threat to the $250B+ IT services industry. This represents a named market entrant with the largest AI model suite, $1B+ in deployment capital (Brookfield), and direct enterprise relationships. Indian IT stocks hitting 52-week lows is the market’s immediate verdict.

The chain: OpenAI enterprise deployment → direct competition with Accenture, Cognizant, Infosys for AI implementation work → reduces the “translation layer” value that services firms charge → compresses margins and growth rates structurally. This strengthens our existing ACN short thesis (Pair Trade #2) with a third independent data point.

What to Watch

Full options positioning analysis, portfolio playbook, and risk scenario framework below for subscribers.

This publication is for informational and educational purposes only and does not constitute financial, investment, or trading advice. The analysis, opinions, and commentary presented here should not be interpreted as a recommendation to buy, sell, or hold any security. Always conduct your own research and consult a qualified financial advisor before making investment decisions. Past performance does not guarantee future results.