Higher Discount Rate Collides With the Chip Layer as Custom Silicon Codifies the GPU-Disruption Threat

Germany's F126 frigate cancellation confirms the European defense-funding unwind in hard data, even as US munitions-shortfall demand bifurcates cleanly toward the primes.

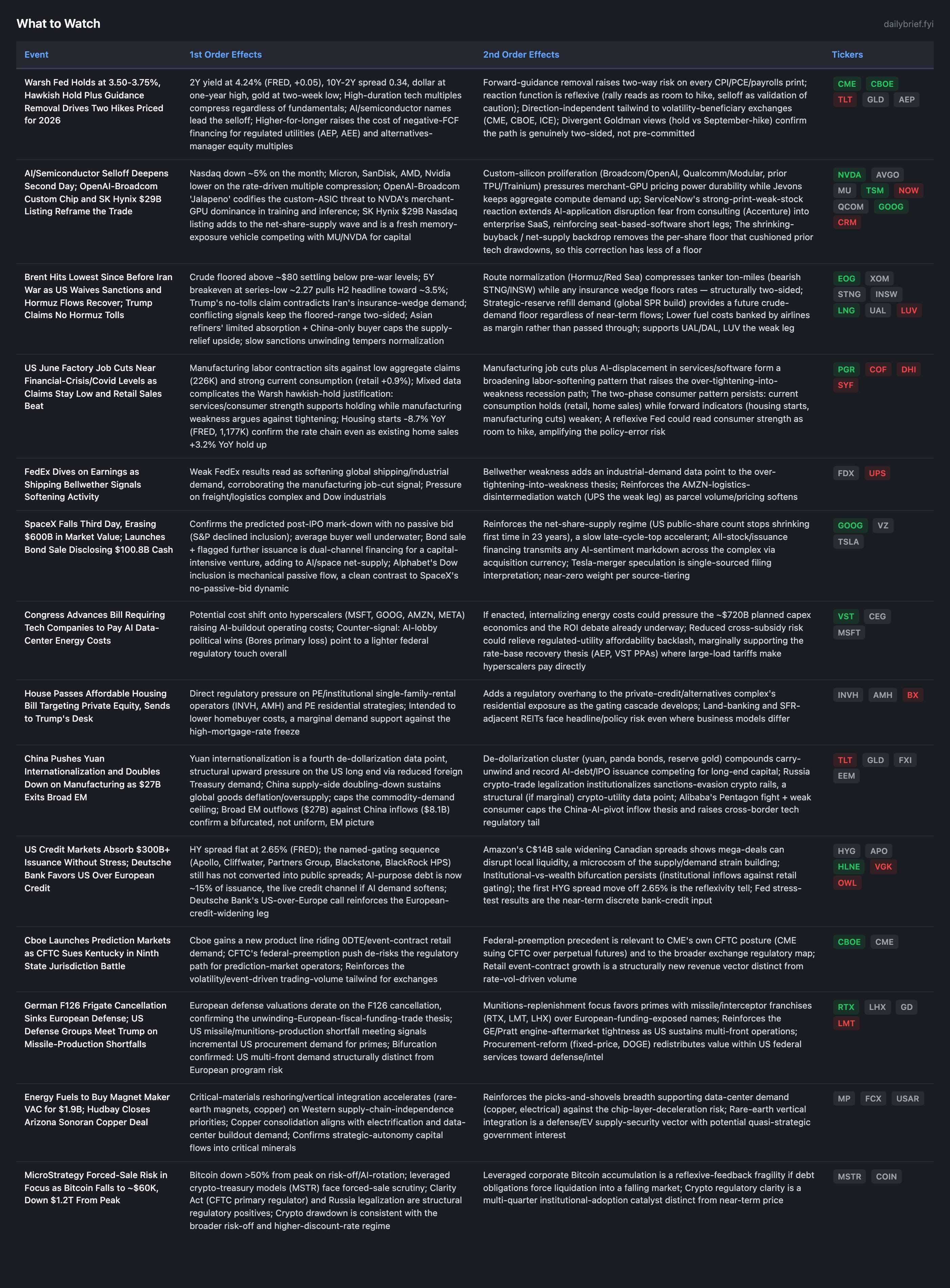

The landscape is largely a continuation of the two binaries that resolved last week (Hormuz reopened, Warsh delivered a hawkish hold plus forward-guidance removal), and most of today’s batch is consequences playing out.

The 2Y sits at 4.24% (FRED), the dollar at a one-year high, Brent below pre-war levels with the 5Y breakeven at a series-low ~2.27, and the AI/semiconductor trade is correcting into its second session as the higher discount rate collides with the chip layer. None of that is new information; it confirms the higher-discount-rate-on-deflating-energy regime called last week.

Three things are genuinely new. First, the OpenAI-Broadcom “Jalapeno” custom chip and Qualcomm’s $3.9B Modular acquisition codify the custom-silicon threat to merchant GPUs the same week ServiceNow fell on a strong print, extending the AI-application-disruption signal from consulting into enterprise SaaS.

Second, US June factory job cuts approached financial-crisis/Covid levels even as claims stayed at 226K and retail rose 0.9% — a sharpening of the over-tightening-into-weakness risk into a reflexive, guidance-free Fed.

Third, the German F126 frigate cancellation (Rheinmetall -17%) confirms the European-defense-funding-trade unwind as a hard data point, cleanly bifurcated from US munitions-shortfall procurement demand.

Underneath, the conflicting Hormuz signals (Trump’s no-tolls claim vs Iran’s insurance demand) keep the floored-oil range two-sided, and the private-credit cascade still has not converted (HY 2.65%, FRED).

Custom Silicon Codifies the GPU-Disruption Threat; Application-Layer Fear Spreads to ServiceNow

OpenAI and Broadcom unveiled their first joint custom chip, “Jalapeno,” eight months after announcing the partnership, and Qualcomm acquired AI software startup Modular to build a data-center software stack (CNBC, Tier 2; corroborated). These are two independent data points in one day pointing the same direction: the largest AI buyers and chip challengers are building around merchant GPUs. The mechanism is the ASIC threat already codified in NVDA’s own risk factors (TPU, Trainium): custom silicon for inference and training erodes merchant-GPU pricing-power durability over time, while aggregate compute demand keeps rising (Jevons). This is not a reason to flip NVDA, whose established BUY rests on ~16.5x next-year EPS, $96.7B FCF, and a 3+ data-point thesis; the custom-silicon vector is a multi-year share-shift risk, not a single-print event. The cleaner read for AVGO is positive — “Jalapeno” validates the custom-ASIC franchise and partially offsets June’s AI-revenue guide cut, though it remains one data point against that miss, so I keep AVGO neutral rather than re-establishing a bull case.

The more decision-relevant signal is ServiceNow falling despite a strong print on AI-disruption concerns (Yahoo, Tier 3). Per the standing lesson to weight demand-side and application-layer AI signals heavily, this extends the impairment fear from labor-arbitrage consulting (Accenture -17% last week) into enterprise SaaS, where AI agents threaten seat-based licensing. It reinforces the short legs of the GOOG-vs-INTU, TSM-vs-WDAY, and PANW-vs-CRM pairs. The honest caveat: ServiceNow beat, so this is sentiment/multiple compression on a single name, an early signal (1-2 data points), not yet confirmed earnings-level deterioration like the Accenture revenue-guide miss.

Factory Job Cuts Near Crisis Levels Into a Guidance-Free Fed

The headline manufacturing index beat on inventory rebuild (S&P, via CNBC, Tier 2), while weekly claims fell to 226K (Reuters, Tier 1) and May retail sales rose 0.9% versus 0.5% expected (Reuters/Invezz, Tier 1-3). FedEx, a shipping bellwether, fell on disappointing earnings (IBD, Tier 2-3). The data are genuinely mixed: resilient current consumption and low aggregate claims against deteriorating manufacturing labor and softening freight.

The reason this matters more than a typical mixed-data week is the reflexive, guidance-free reaction function. With the dot plot and forward guidance removed, the Fed must re-derive its reaction to each print, and a market-deferential Fed could read consumer strength as room to hike while the manufacturing/freight weakness argues the opposite. Manufacturing cuts plus AI-displacement in services/software (Accenture, ServiceNow, Oracle’s prior layoffs) form a broadening labor-softening pattern that raises the over-tightening-into-weakness recession path. Kalshi prices 2026 recession at 12%, which continues to look low against this accumulating evidence, though the strong current-consumption data (retail, existing home sales +3.2% YoY per FRED) is the genuine counterweight that has kept the cliff a forward risk rather than a present one.

European Defense-Funding Unwind Confirms in Hard Data; US Munitions Demand Bifurcates

Germany will scrap the multi-billion-euro F126 frigate program, sending the European defense complex lower (CNBC, Tier 2). Separately, US defense groups are meeting Trump over struggles rebuilding conventional weapons and missile stockpiles (FT, Tier 2). This is a clean confirmation of the world-model bifurcation: the European defense valuation run-up rested partly on a fiscal-funding trade that is now visibly reversing, while US multi-front demand (Middle East, NATO/Russia, Israel-Lebanon) plus a concrete munitions-production shortfall sustains procurement demand for US primes. The munitions-replenishment focus favors missile/interceptor franchises (RTX, LHX), with the caveat that LMT’s bottom-up AVOID (reach-forward losses, capital-return-EO risk) complicates the long leg of the LMT-vs-ACN pair even as the ACN short leg stays strongly confirmed.

What to Watch

Developing Themes

Iran/Oil: Floored Range Stays Two-Sided on Conflicting Hormuz Signals

The floored-oil regime called last week holds, but today added a contradiction worth flagging: Trump claimed Iran assured no tolls or insurance charges on Hormuz (CNBC, Tier 2), directly contradicting Iran’s prior Tehran-approved-insurance demand. Brent fell to its lowest since before the war on sweeping US sanctions waivers and authorization of Iranian sales through August (Reuters, Tier 1), but Asian refiners have little room for Iranian crude (China the key buyer), and Reuters reports the sanctions unwinding is slow — both cap the supply-relief downside in price. The conflicting toll/insurance signals are the open variable: if the no-tolls claim holds, the floor is lower; if Iran’s insurance wedge prevails, crude is floored higher and tanker rates supported. STNG/INSW stay two-sided for that structural reason. The Ras Laffan LNG blast (13 dead) and Qatar’s “normal output within weeks” keep US contracted-LNG relatively advantaged (LNG). The Senate joining the House to halt the war reduces the escalation tail at the margin; Treasury overseeing released Iranian funds (routed to US agriculture/medicines) is a manageable mechanism, not a market mover.

Private Credit: Still No Conversion at 2.65%; Stress Tests the Near-Term Input

HY spread is flat at 2.65% (FRED), confirming the named-gating sequence (Apollo flagship, Cliffwater, Partners Group, Blackstone, BlackRock HPS) has not converted into public spreads; the cascade stays priced H2 2026-H1 2027. The MarketWatch framing that $300B+ of issuance was absorbed without stress, much of it AI-tied, is the same no-conversion state, now with AI-debt at ~15% of issuance as the live channel if demand softens. Amazon’s C$14B loonie sale widening Canadian spreads is a microcosm of mega-deal supply straining local liquidity. Deutsche Bank’s US-over-European credit call reinforces the euro-widening leg. Fed stress-test results are the near-term discrete input; the first HYG move off 2.65% remains the reflexivity tell. Hold APO/ARES over BX/OWL; HLNE the mispriced recurring-fee long, now with the House anti-PE-housing bill adding a marginal residential-PE overhang to BX.

Net-Share-Supply: SpaceX Mark-Down Confirmed, SK Hynix Adds Supply

SpaceX fell a third day, down 23% over three sessions and erasing $600B, then launched a bond sale disclosing $100.8B cash (Bloomberg/CNBC, Tier 2). This is the predicted no-passive-bid mark-down (S&P declined inclusion) playing out, plus dual-channel debt-and-equity financing for a capital-intensive venture. SK Hynix’s planned ~$29.65B Nasdaq listing as soon as July 10 adds another large supply event and a fresh memory-exposure vehicle. Alphabet replacing Verizon in the Dow on June 29 is the mechanical-passive-flow contrast (a tailwind for GOOG, an outflow for VZ). The Tesla-merger speculation is single-sourced filing interpretation; near-zero weight.

Continuing Themes

Rates: Higher-for-longer confirmed; two 2026 hikes now priced (Seeking Alpha), Goldman split (hold vs September-hike). Do not pre-position into the reflexive reaction function; let CME/CBOE/ICE carry the vol.

De-dollarization: Yuan internationalization is a fourth data point; structural long-end pressure compounding carry-unwind and AI-debt/IPO supply. Bearish duration, structural gold bid intact through the near-term pullback.

Consumer: Two-phase read intact — current strength against housing starts -8.7% YoY, manufacturing cuts, FedEx. PGR over COF, extending to SYF/RDN. Consumer Discretionary BUY-prohibited.

Power/electrical: Overweight intact; critical-materials reshoring (Energy Fuels/VAC, Hudbay copper) adds picks-and-shovels breadth against chip-layer deceleration. GEV-vs-ORCL CORE.

Crypto: Bitcoin ~$60K, MSTR forced-sale risk in focus; Clarity Act and Russia legalization structural positives against waning momentum. No portfolio-relevant change.

A note on the staleness alert: the Maximum Conviction, Key HOLDs, and AVOIDs sections (last new evidence May 28, now ~27 days stale) received no new company-level evidence today. The GLP-1 and Airlines theses (15 days stale) also got no new direct evidence; today’s lower-fuel read marginally supports the UAL/DAL-over-LUV airline lean by consistency, not fresh confirmation. I reaffirm these by consistency while acknowledging the staleness, and continue to flag LMT (AVOID 4.9) for active re-examination given the US munitions-demand tailwind sits against its bottom-up rating.

The options structure has flipped broadly into backwardation — QQQ deep at 49.4% near vs 24.2% far while holding its -3.0% 12-month AI-tail skew into the late-July NVDA print, IWM carrying a 2.43 OI P/C and the steepest -3.3% skew on the small-cap consumer-cliff thesis, and HYG’s 3.08 OI P/C with a -7.3% 12-month skew pricing the H2 credit window against near-term calm. Untangling the same-day-expiry artifacts from the durable hedges is what tells you whether the chip rout is a rotation or the leading edge of a demand crack. The premium section maps how to hold high-conviction AI infrastructure through the correction without resolving the demand question on a tape day, where the floored-oil and private-credit two-sided ranges actually break, and which of seven risk scenarios — from a reflexive Fed over-tightening to a net-supply wave deepening the drawdown — carries the highest leverage.

Full options positioning analysis, portfolio playbook, and risk scenario framework below for subscribers.

This publication is for informational and educational purposes only and does not constitute financial, investment, or trading advice. The analysis, opinions, and commentary presented here should not be interpreted as a recommendation to buy, sell, or hold any security. Always conduct your own research and consult a qualified financial advisor before making investment decisions. Past performance does not guarantee future results.