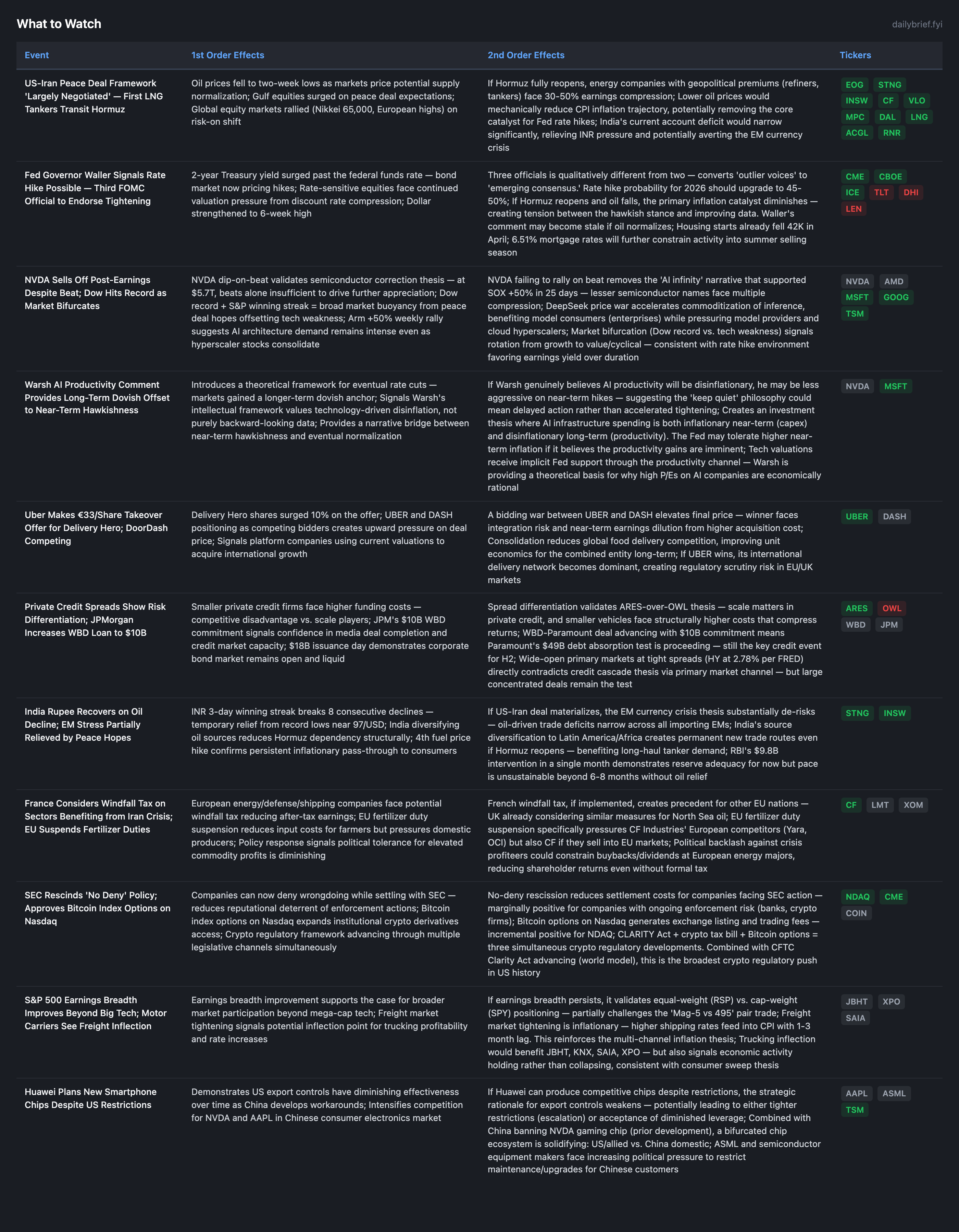

First Physical Hormuz Transit Signals Potential De-Escalation as Fed Hawks Consolidate

Governor Waller becomes third FOMC official to endorse rate hikes, but the very inflation catalyst driving hawkishness may be evaporating as LNG tankers cross the strait.

The dominant shift since the May 22 brief: physical evidence of Hormuz de-escalation has arrived for the first time in this conflict cycle. LNG tankers transiting Hormuz, combined with Reuters (Tier 1) reporting the deal framework is “largely negotiated,” represents a qualitatively different signal than the 15 prior failed diplomatic announcements. Per the analyst lesson (13x reinforced), we still require 72+ hours of sustained physical confirmation before changing the base case — but the first tanker transit is the most credible de-escalation indicator since the war began.

Simultaneously, Governor Waller became the third FOMC official to endorse rate hikes, upgrading the hawkish consensus from “two regional presidents” to “a Governor + two presidents” (Governors carry more institutional weight than regional presidents because they always vote). Rate hike probability for 2026 should upgrade to 45-50%. However, if Hormuz reopens and oil falls materially, the primary inflation catalyst diminishes — creating a tension where the hawkish consensus forms precisely as the data may begin reversing.

Three secondary developments merit attention: (1) NVDA beat-and-dip confirmed, with the Dow simultaneously hitting records — market bifurcation between AI exhaustion and cyclical/value strength, (2) DeepSeek’s permanent 75% model price cut escalates AI commoditization, benefiting infrastructure and consumers while pressuring model providers, and (3) France’s windfall tax discussion + EU fertilizer duty suspension signal political tolerance for crisis profiteering is ending.

Net assessment: The Hormuz transit introduces the first genuine counter-signal to the energy maximum overweight thesis (0-for-15 becomes 0-for-15 with a physical data point). I assign 25-30% probability this represents the beginning of actual de-escalation (upgraded from 8-12% in the world model). If sustained over 72 hours with additional ships, energy positioning must be reassessed. If it reverses per pattern, maximum overweight continues.

Physical Hormuz Transit: First Counter-Signal to Energy Thesis in 15 Attempts

This requires careful calibration. The world model contains 13x reinforcement that peace rhetoric should be discounted without operational specifics. Today we have the first operational specific: LNG tankers physically transiting Hormuz, confirmed by Bloomberg (Tier 1) and FT (Tier 1). This is categorically different from diplomatic rhetoric.

The causal chain for genuine de-escalation: (1) deal framework reportedly “largely negotiated” with Hormuz reopening provision, (2) Iran envoys in Qatar finalizing details, (3) physical ships transiting, (4) oil dropping to 2-week lows, (5) Gulf markets surging, (6) India’s rupee recovering. Six concurrent signals across price, diplomacy, physical operations, and EM currencies all pointing the same direction.

Counter-arguments: (1) Trump explicitly said “blockade remains in place for now,” (2) Iran denies agreeing to enriched uranium handover, (3) Israeli ministers calling for Lebanon escalation could derail any deal, (4) the physical transit may be a pre-arranged confidence-building measure during negotiations rather than full reopening. Jeff Currie’s “tank bottoms in Asia” warning suggests even if Hormuz partially reopens, existing inventory depletion creates sustained tightness.

Assessment: Upgrade peace deal probability to 25-30% (from 8-12%). Maintain energy overweight but reduce sizing conviction from “maximum” to “high” pending 72-hour confirmation. If 3+ additional tankers transit within 72 hours, begin reducing tanker/refiner positions (STNG, VLO, MPC) by 25-30%. If transit halts or reverses, maintain full positioning.

This is the first time in 15 signals where I’m recommending even contingent position adjustment .

Waller = Third FOMC Official: Rate Hike Consensus Solidifying

The prior brief tracked Collins (regional) + Paulson (regional) + committee majority documented in minutes. Waller is a Board Governor — institutionally more significant than regional presidents because Governors always vote, regional presidents rotate. Three named officials endorsing hikes, with one being a Governor, represents emerging consensus.

FRED data confirms the bond market’s response: 2Y yield at 4.08% (5/21), up from 3.64% Fed Funds Rate. The 2Y exceeding the funds rate is the bond market pricing in tightening rather than easing. The 10Y-2Y spread at 0.43% (falling) with both yields rising simultaneously = tightening expectations, not recession expectations.

However, Warsh’s AI productivity comment introduces an intellectual framework where the Fed Chair personally believes technology will be disinflationary. If Warsh genuinely views AI as structurally reducing inflation, he may resist near-term hikes in favor of waiting for productivity evidence — a “patient hawk” rather than an “immediate hawk.” This creates uncertainty about timing even as direction becomes clearer.

Assessment: Rate hike probability by year-end: 45-50% (upgraded from 40-45%). But conditional on oil: if Hormuz reopens and Brent drops to $90-95, the inflation data reverses over 2-3 months, removing the primary catalyst for hikes. The path dependency is: Hormuz stays closed → inflation persists → hikes happen. Hormuz opens → inflation moderates → hikes unnecessary.

DeepSeek 75% Permanent Price Cut: AI Commoditization Accelerates

DeepSeek making a 75% price cut permanent (not promotional) is a structural statement about AI inference economics. The marginal cost of running frontier AI models is declining faster than expected. This has differentiated effects:

Winners: Enterprises adopting AI (lower costs → faster adoption), infrastructure providers (volume increases offset price decline), companies using AI for productivity (Warsh’s thesis materializes faster).

Losers: Cloud providers competing on inference pricing (MSFT Azure AI, GOOG Cloud AI, AMZN Bedrock margins compress), standalone AI model companies without platform lock-in.

The mechanism: if DeepSeek at 75% discount can offer competitive quality, it forces OpenAI/Anthropic/Google to match or demonstrate sufficient quality premium to maintain pricing. This is the textbook commoditization pattern that destroys margins for undifferentiated providers while benefiting scale and infrastructure.

For NVDA specifically: if inference becomes cheaper, demand for inference compute could actually increase (Jevons paradox) — more organizations run more AI at lower unit costs. The training compute market remains constrained by NVDA. Net effect on NVDA: likely neutral to positive as volume growth offsets any future ASP pressure on inference chips.

SpaceX IPO + Mega-IPO Warnings as Market Top Signal

The prior brief identified SpaceX’s $350B+ offering creating forced rotation from existing tech holdings. Analyst commentary explicitly calls mega-IPOs (SpaceX + OpenAI) a historically reliable market-top contrarian signal. This doesn’t mean the market peaks tomorrow, but it introduces a medium-term structural headwind.

At BofA’s lowest cash since Feb 2024 + maximum equity exposure, allocation for SpaceX (June 12 expected) requires selling existing holdings. The compressed timeline (under 3 weeks) means institutional portfolio managers are making those allocation decisions now.

Consumer: Lowe’s Alarm + WMT Pattern Confirmed

Lowe’s “sounding alarm” about consumer behavior confirms the TGT/WMT pattern: Q1 spending held via tax refunds and credit expansion, but management commentary uniformly signals H2 deterioration. This is now the 4th major retailer (HD, TGT, LOW, WMT) providing this two-phase message. The consumer thesis has fully shifted from “imminent collapse” (eliminated) to “buffer-funded spending with H2 cliff” (management-confirmed, 4 data points).

Retail sales at $757B (FRED, +4.9% YoY) with CPI at 3.8% = real spending growth of ~1.1%. Michigan sentiment at 49.8 (falling) confirms consumer feelings are deteriorating faster than behavior — typically a leading indicator by 2-3 quarters.

EM Crisis: Partially Relieved but Not Resolved

Indian rupee’s 3-day winning streak on oil decline + RBI support breaks the 8-decline streak. If the peace deal materializes, the EM crisis thesis substantially de-risks: India’s current account deficit narrows, reserve drawdown slows, and the INR-100 threshold recedes. However, 27 countries seeking World Bank crisis funds demonstrates the stress is broader than India. Singapore’s lower inflation (1.8% vs 1.7% expected) is a positive EM data point but Singapore is not representative of oil-importing EMs.

Assessment: EM crisis probability downgraded contingent on Hormuz: if deal materializes → 10-15% (from 20-30%). If deal fails per pattern → 25-35% (upgraded due to reserves depletion pace).

Credit Markets: Open and Functioning

HY spread at 2.78% (FRED, -0.02 from prior) — continuing to tighten despite everything. $18B issuance day. JPM extending $10B for WBD-Paramount deal. Bond market pricing differentiation among private credit firms (quality dispersion) but not systemic stress. The credit cascade via primary market closure pathway remains dead. CRE pathway active but timeline extends if yields moderate from peace deal.

Continuing Themes

Semiconductor correction: NVDA beat-and-dip confirmed. 40-50% correction probability within 2-4 weeks unchanged. DeepSeek price cut adds commoditization pressure. Arm +50% shows architecture demand persists — divergence within semis rather than sector-wide collapse.

Exchange thesis: 7th catalyst added (Bitcoin index options on Nasdaq + CLARITY Act). CME maximum conviction maintained.

Enterprise software impairment: No new data point this scan. GOOG vs INTU pair stable at 9 data points.

Defense: Israel pushing Lebanon escalation introduces risk that peace deal could redirect rather than eliminate conflict. LMT/RTX thesis unchanged — 8 state actors, demand structural.

What to Watch

The options market is revealing positioning that cuts against surface-level narratives. TLT is showing massive deep out-of-the-money call buying (93.2x Vol/OI at the $79 strike) — someone is positioned for a violent Treasury rally if the peace deal triggers an oil crash and inflation expectations collapse within days. Meanwhile, IWM maintains structural put dominance with a 2.13x OI put/call ratio and institutions targeting a 6.4% small-cap decline by June 12 — precisely when SpaceX is expected to price. HYG put volume surged to 5.81x despite tight spreads, signaling fresh credit protection being purchased for a tail event the market hasn’t yet experienced. The conditional reduction framework for energy — triggered only by 3+ additional tanker transits within 72 hours — provides the specific decision rules that separate reactive trading from systematic positioning.

Full options positioning analysis, portfolio playbook, and risk scenario framework below for subscribers.

This publication is for informational and educational purposes only and does not constitute financial, investment, or trading advice. The analysis, opinions, and commentary presented here should not be interpreted as a recommendation to buy, sell, or hold any security. Always conduct your own research and consult a qualified financial advisor before making investment decisions. Past performance does not guarantee future results.