Europe's Three-Front Energy Crisis Deepens as Russia Suspends Kazakh Oil Flows to Berlin

ASML's guidance raise to €40B provides the strongest upstream validation of the AI capex cycle this quarter, even as global inflation data confirms energy-to-consumer price transmission is now active.

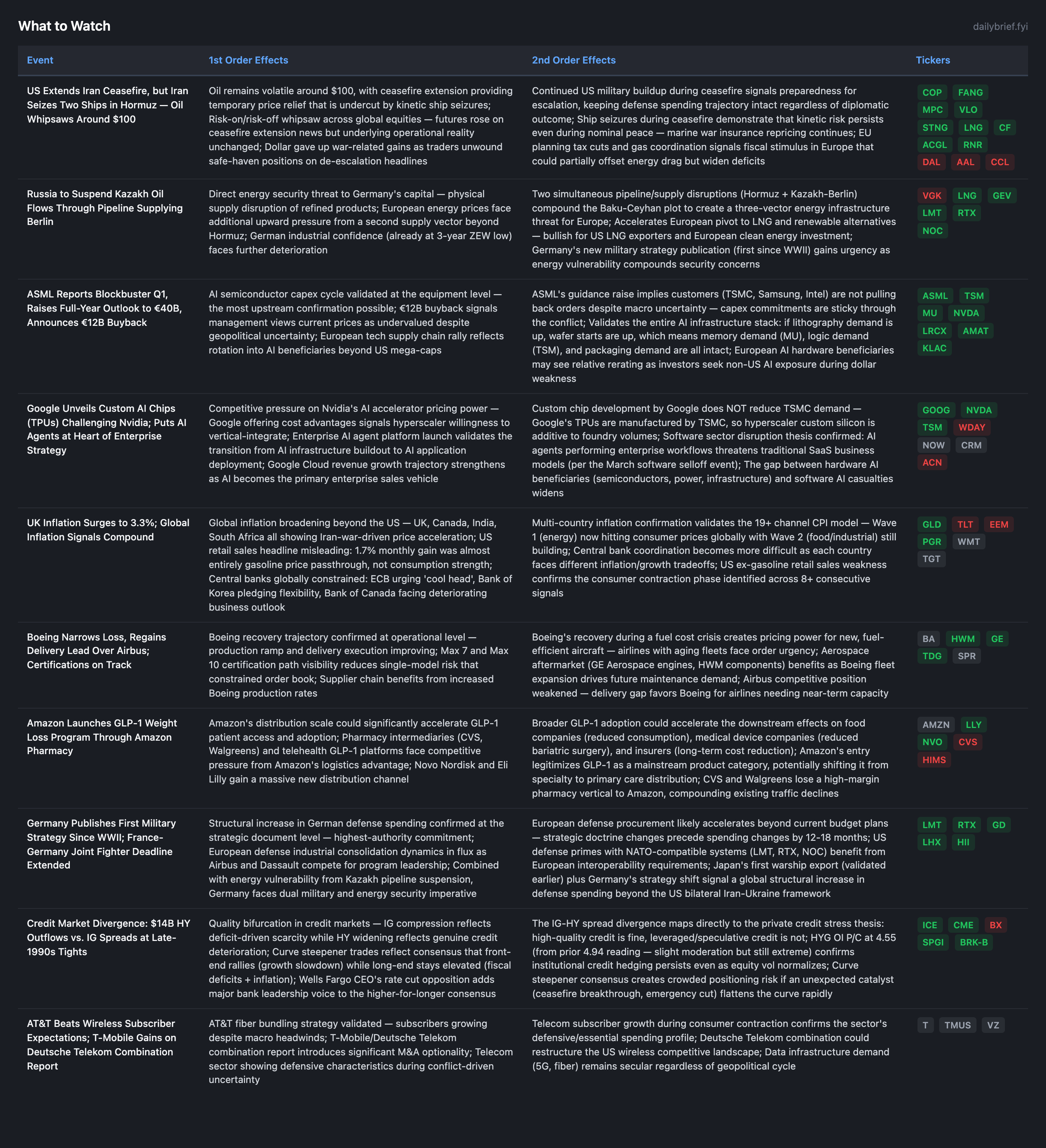

The ceasefire extended but nothing changed operationally. Iran seized two ships in Hormuz hours after Trump announced an extension he previously said he didn’t want. Oil touched $100, retreated, and remains volatile near that level. The IEA’s declaration of “the largest energy crisis in history” is now consensus. US military buildup continues with a third carrier group deploying despite the ceasefire.

Three genuinely new developments since yesterday’s brief: (1) Russia suspending Kazakh oil flows through the pipeline supplying Berlin creates a second energy supply vector threatening Europe, compounding Hormuz and the Baku-Ceyhan plot into a three-front energy infrastructure crisis. (2) ASML’s blockbuster Q1 with a guidance raise to €40B and €12B buyback provides the strongest upstream validation of the AI capex cycle this quarter. (3) Global inflation data confirms the energy-to-consumer price transmission is now active across developed economies: UK CPI at 3.3%, Canada at 2.4%, India swap rates 40bps above pre-conflict levels.

The credit-equity divergence persists: HYG OI P/C remains extreme at 4.55, equity indices are in backwardation (SPY 18.6% near-term vs 15.0% 12-month), and small-cap/EM stress signals intensified. The options market is pricing a more cautious environment than the headline ceasefire extension implies.

New Developments

Russia-Berlin Pipeline Suspension: Europe’s Three-Front Energy Crisis

This is the most consequential new development not covered in prior briefs. Moscow’s planned suspension of Kazakh oil flows through the pipeline supplying Berlin’s petrol, kerosene, and heating fuel creates a direct energy security threat to Germany’s capital that is geographically and politically independent from the Iran conflict.

Combined with (1) Hormuz closure disrupting Middle East energy flows, (2) the thwarted Baku-Ceyhan pipeline plot demonstrating Iranian intent to target non-Gulf infrastructure, and (3) the IEA’s 2-year recovery timeline, Europe now faces three simultaneous energy supply vectors under stress. The German ZEW investor morale index at a three-year low and Germany’s GDP forecast already halved to 0.5% were pricing a one-front energy crisis. A two-front crisis (Iran + Russia) is qualitatively different.

The investment implications are direct. European equities (VGK) face compounding headwinds — the options market already prices VGK in backwardation at 21.7% near-term IV (6.9pp above HV). US LNG exporters benefit structurally as European pipeline alternatives narrow. Germany’s simultaneous publication of its first military strategy since WWII gains urgency when energy vulnerability is acute. EU tax cuts and gas coordination plans signal fiscal stimulus that partially offsets but cannot eliminate the supply-side constraint.

For European-exposed US companies: this is bearish for firms with significant European revenue dependent on consumer spending (consumer discretionary exporters), and bullish for US energy infrastructure that provides alternatives (LNG, GEV gas turbines).

ASML Beat + Guidance Raise: AI Capex Cycle’s Strongest Upstream Confirmation

ASML’s Q1 beat and €40B full-year guidance raise (from prior €35-40B range) is the most important data point for the AI infrastructure thesis this week. Lithography demand growth means wafer starts are growing, which means every downstream segment (logic, memory, packaging, test) has sustained demand.

The €12B buyback through 2028 is a capital allocation signal: management views the stock as undervalued even at current levels, despite Hormuz supply chain risk to semiconductor logistics. This suggests ASML’s order book visibility extends well beyond any reasonable ceasefire timeline.

For the broader AI stack: ASML’s guidance raise implies TSMC, Samsung, and Intel are not pulling back fab orders. This validates NVDA (end-demand), MU (HBM memory at capacity), TSM (foundry volumes), and the entire equipment chain (LRCX, AMAT, KLAC). Google’s custom TPU announcement, while competitive for NVDA at the chip design level, is additive for TSMC and ASML — Google’s chips are manufactured at TSMC, so hyperscaler custom silicon increases total foundry demand.

Global Inflation Confirmation: Wave 1 Hitting Consumer Prices Across Developed Economies

UK CPI surging to 3.3% is the first hard data confirmation that Iran-war energy costs are transmitting through to consumer prices in major developed economies. Canada at 2.4%, Indian swap rates 40bps elevated, South African rand weakening on inflation fears, Philippines’ Fitch outlook cut to negative — the global breadth is striking.

US March retail sales at +1.7% monthly appear strong but decompose poorly: the 15.5% surge in gas station receipts explains virtually all the headline gain. Excluding gasoline, underlying consumer spending was modest. This confirms the pattern identified across 8+ consecutive signals: consumers are spending more but consuming less, with rising energy costs absorbing purchasing power.

The Fed implications are clear. Warsh’s inflation-first stance, Hammack’s “hold for a good while,” Waller’s conditional rate cuts only if the war ends quickly, and Wells Fargo CEO’s explicit opposition to pre-conflict-end rate cuts form a multi-voice consensus. Global inflation broadening strengthens the case that rate hikes (35-45% probability) are more likely than cuts (3-5%). The 5Y breakeven at 2.60% (rising, per FRED data) confirms the bond market is pricing persistent inflation.

Amazon GLP-1 Distribution Entry

Amazon launching GLP-1 weight loss programs through Amazon Pharmacy is material for the healthcare distribution chain. Amazon’s logistics scale and consumer trust could meaningfully accelerate patient access to Wegovy and oral GLP-1 options, benefiting drug manufacturers (LLY, NVO) while pressuring pharmacy intermediaries (CVS) and telehealth GLP-1 platforms (HIMS). This is a single data point for Amazon (monitoring) but an additive catalyst for the established LLY thesis.

Developing Themes

Defense: Germany’s Military Strategy Adds Another Structural Spending Vector

Germany publishing its first military strategy since WWII, committing to “more responsibility” for European defense, adds to Japan’s warship export validation from earlier this week. The global defense spending expansion now has independent data points from the US (dual-theater, $1.5T+ budget), Europe (Germany strategy + France-Germany fighter jet program), and Asia-Pacific (Japan export). LMT Q1 earnings remain the sector’s valuation anchor this week. RTX’s beat already validated the thesis.

Boeing Recovery Gains Credibility

Boeing narrowing its Q1 loss, regaining the delivery lead over Airbus (widest since 2018), and gaining FAA certification visibility for Max 7 and Max 10 are three positive data points in a single quarter. This doesn’t warrant a BUY yet — Boeing remains in recovery with negative FCF — but the trajectory is improving. The aerospace supply chain (HWM, GE, TDG) benefits directly from production rate increases. The $100+/flight fuel cost addition creates pricing urgency for fuel-efficient new aircraft orders, which benefits Boeing’s order pipeline.

Software Disruption Thesis Strengthens

Google’s enterprise AI agent platform launch at Cloud Next, combined with the March software selloff on AI disruption fears, adds another data point to the structural pressure on traditional SaaS models. The pair trades (GOOG/INTU, TSM/WDAY) reflect this thesis. Google’s move from infrastructure provider to enterprise application competitor via AI agents widens the competitive surface area against ServiceNow, Salesforce, and Workday.

Consumer Contraction: 9th+ Consecutive Signal

US retail sales decomposition (gasoline-driven), UK employer caution, German ZEW three-year low, Indian business confidence declining, and Goldman’s “challenging months” warning collectively extend the consumer weakness pattern. Discretionary AVOID maintained. No exceptions.

Continuing Themes

Iran conflict: Ceasefire extended but operationally irrelevant — ship seizures continue, Hormuz near-standstill. 0-for-8 on diplomatic signals producing operational change. All structural positions (energy, fertilizer, defense, insurance, tankers) maintained.

Fed policy: Unanimous hold at 3.64%. Tillis blocking confirmation. Hike probability 35-45%, cut 3-5%.

Credit cascade: HYG OI P/C at 4.55 (moderated from 4.94 but still extreme). $14B HY outflows. IG spreads at late-1990s tights while HY widens — quality bifurcation confirms private credit thesis. BDC NAV marks in May remain the key signpost.

Apple CEO transition: No new data. HOLD, BUY trigger $190-200.

What to Watch