Escalation Reasserts in Hormuz as Nvidia Storms the PC Market

Q1 retail strength revealed as a tax-refund-and-BNPL mirage, sharpening the consumer cliff thesis just as Warsh inherits a stagflation committee.

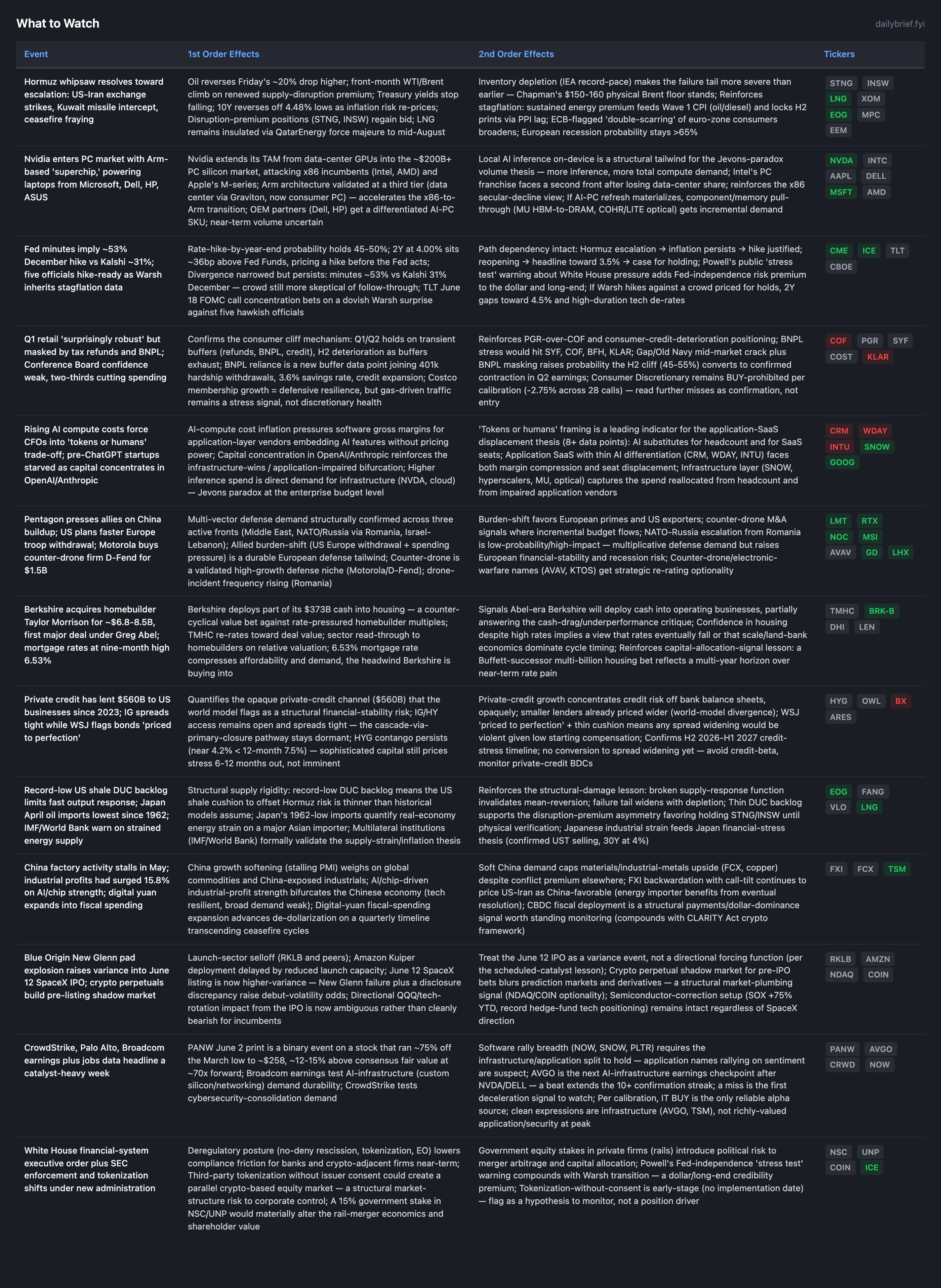

The Hormuz binary resolved toward escalation over the weekend, the 17th reversal in a sequence that has flipped every 48-72 hours. Friday’s reopening framework (oil -20%, 10Y to 4.48%) has been overtaken by fresh US-Iran strikes, a US interception of Iranian missiles aimed at American forces in Kuwait, Trump declaring he is in no “hurry” for a deal, and new US sanctions on Iran’s military oil sales. Oil reversed higher; yields stopped falling. The verification discipline held again: anyone who reduced energy on Friday’s framework would be caught flat, and the pre-committed posture of holding the overweight through both directions remains correct. The next trigger is unchanged: 72+ hours of sustained uninterrupted commercial transit.

The genuinely new development is Nvidia’s entry into the PC market with an Arm-based “superchip” (RTX Spark), partnering with Microsoft, Dell, HP and ASUS, a direct attack on x86 (Intel/AMD) and Apple silicon. This extends Nvidia’s TAM into consumer PCs, validates Arm at a third tier (data center to PC), and supports the local-inference leg of the Jevons-paradox volume thesis. The other new, durable signal is a CNBC report that Q1 retail strength was masked by tax refunds and BNPL financing, a fresh buffer-depletion data point joining the 401k hardship withdrawals from last week. On rates, the minutes-vs-crowd gap narrowed but persists (minutes ~53% December vs Kalshi 31%, up from 18% last week), and Powell publicly warned that White House pressure is a “stress test” on Fed credibility as Warsh approaches his June 16-17 inaugural meeting.

The macro regime is unchanged: stagflation in official data (Q1 GDP 1.6%, core PCE near 3.3-4%, headline 3.8%), AI-infrastructure overweight intact, consumer cliff thesis strengthening, energy overweight maintained through the whipsaw.

Nvidia Enters the PC Market: Arm-Based Superchip Attacks x86 and Apple Silicon

Nvidia unveiled its first Arm-based PC chip to run AI applications locally. This is corroborated across three Tier 2 sources (CNBC, FT, MarketWatch) and lifted Arm, IBM and HP on the announcement.

Causal chain: Nvidia extends from data-center GPUs into the ~$200B+ PC silicon market, directly attacks x86 incumbents (Intel, AMD) and Apple’s M-series, and validates Arm architecture at a third tier (data center via Graviton, now consumer PC, after mobile/edge). The world model already flagged the $6B Snowflake-Graviton commitment as enterprise-scale Arm validation; this is the consumer-scale confirmation.

The second-order effect that matters most is on the Jevons-paradox thesis. On-device local inference is a new vector of inference demand, reinforcing the view that cheaper, more pervasive inference raises total compute volume rather than cannibalizing it. This is consistent with the established NVDA-neutral-to-positive-on-DeepSeek reasoning. For Intel, this is a second competitive front after data-center share loss, reinforcing the secular x86-decline view, though it is a single data point on the PC franchise specifically and I am keeping INTC at neutral/monitoring rather than establishing a bearish conviction.

Position discipline holds: confirming demand is not a buy signal. NVDA stays a HOLD (7.19); do not add into record hedge-fund tech positioning at the multiple. DELL gains a differentiated AI-PC SKU but remains a margin-dilutive integrator at ~32x forward (HOLD 5.6). MSFT (BUY 7.3) is the cleaner expression as the OS partner.

Q1 Retail Strength Was Masked by Tax Refunds and BNPL

CNBC reports Q1 retail sales and profits were “surprisingly robust” but propped up by elevated tax refunds and buy-now-pay-later financing, with the real demand test ahead as refunds dry up. This slots into the established sequence: excess savings (depleted), credit (active), savings rate (3.6%), 401k hardship withdrawals (confirmed last week), now tax refunds and BNPL identified as the Q1 prop.

This explains the apparent contradiction between resilient headline retail sales (+4.9% YoY per FRED, ~1.1% real against 3.8% CPI) and the Gap/Old Navy mid-market earnings crack. The strength is transient and buffer-funded; the deterioration is structural. The H2 cliff probability (45-55%) is reinforced. It also sharpens the consumer-credit-deterioration positioning: a BNPL/refund unwind hits SYF, COF, BFH, and KLAR, strengthening the PGR-over-COF pair. Consumer Discretionary remains BUY-prohibited per calibration (-2.75% across 28 calls); read further misses as confirmation, not entry points.

AI Compute Cost Inflation: “Tokens or Humans”

A CNBC report that AI inference/infrastructure costs are running far above CFO expectations, forcing a “tokens or humans” budget trade-off, is a new framing of the application-SaaS displacement thesis. It cuts two ways and both favor the established bifurcation. First, AI substitutes for headcount, which is the displacement mechanism for application SaaS that sells seats (WDAY, CRM, INTU). Second, higher inference spend is direct demand for infrastructure (NVDA, hyperscalers, SNOW), Jevons paradox at the enterprise budget level. Capital concentration in OpenAI/Anthropic ($250B+) reinforces that the infrastructure layer captures the spend. The pair trades (GOOG vs INTU, TSM vs WDAY, PANW vs CRM) remain CORE and earnings-validated.

What to Watch

Developing Themes

Hormuz: Escalation Reversal Confirms the 17th Signal Failed

The reopening framework reversed within the same 48-72 hour cadence as the prior 16. The strikes, Kuwait intercept (third-party Gulf state now in the perimeter), “no hurry” stance, and military-oil sanctions all point to a sustained conflict. SPY near-term IV has spiked back to 18.5% and QQQ to 30.2% (both backwardation), consistent with the lesson that equity vol normalization during active conflicts overstates resolution; the front-end spike reflects the weekend escalation plus the binary catalyst week ahead. The asymmetry favors holding disruption-premium exposure: the failure tail is $150-160 (Chapman, on record-low DUC backlog and IEA-confirmed depletion) versus $85-95 on reopening. Hold STNG/INSW and LNG; do not reduce until 72+ hours of sustained transit.

Rate Path: Divergence Narrows, Stays Live Into Warsh’s First FOMC

The minutes-vs-crowd gap narrowed but persists, with June at 3% and year-end hike probability holding 45-50%. Five officials are hike-ready; Jefferson called policy “well positioned” amid upside risks. The independence premium rises as Warsh inherits 1.6% growth, 3.8% headline inflation, and a hawkish committee. The TLT June 18 FOMC call concentration bets on a dovish Warsh surprise against that consensus. Do not pre-position; the outcome is path-dependent on whether oil escalation keeps headline inflation elevated (hike justified) or a reopening pulls it toward 3.5% (case for holding). Two-sided into June 16-17; let exchanges carry the vol.

Credit: Private Credit at $560B, Access Open, Contango Persists

The $560B private-credit figure quantifies the opaque non-bank lending channel the world model flags as a structural risk. IG spreads stay tight, issuance heavy, and WSJ warns bonds are “priced to perfection” with thin cushion. HYG remains in contango (near 4.2% < 12-month 7.5%, OI P/C 3.87), stress priced 6-12 months out, not imminent. The cascade-via-primary-closure pathway stays dormant while access is open; only the HYG-contango pathway (H2 2026-H1 2027) is live. No action; avoid credit beta.

Defense: Three Fronts Plus Allied Burden-Shift and Counter-Drone M&A

The Pentagon’s allied-spending push, reports of a faster US Europe troop withdrawal, the Romania drone strike, and Motorola’s $1.5B acquisition of counter-drone firm D-Fend all reinforce multi-vector demand. Counter-drone is a validated niche where incremental budget is flowing. Overweight maintained: LMT, RTX (Kuwait intercept directly validates interceptor demand), NOC, GD, LHX; MSI gains counter-drone exposure.

Continuing Themes

Small-cap: IWM OI P/C at 2.05 with near-term IV back to 32.8% (backwardation); structural put dominance intact, July 2 $260 put thesis live. Continue to avoid.

Semiconductor correction: SOX +75% YTD, record hedge-fund tech positioning; 40-50% correction probability within 2-4 weeks maintained. June 12 SpaceX now a variance event, not a directional forcing function.

CF Industries: No new data point; maintain tactical HOLD (6.0). China urea resumption and antitrust/probe overhang persist; clean exit if Hormuz physically reopens.

Gold: GLD at $417 with near-term IV 39.5% (backwardation) but real-yield channel still dominates the safe-haven function. No thesis change.

Japan: April oil imports at a 1962 low quantify real-economy energy strain; financial-stress thesis (UST selling, 30Y at 4%) intact.

The options tape is telling a sharper story than the headlines: QQQ near-term IV at 30.2% (vs 15.9% HV) with a 24.8% one-week put skew sits against constructive 20.6% twelve-month vol, EEM is the most stressed risk complex at +15.9pp over HV with a -7.4% six-month put skew expressing the Hormuz binary through both tails, and TLT’s call-heavy 0.75 OI P/C is the dovish-Warsh bet running into five hawkish officials. The premium section maps how to weight these structural readings against the front-end spike, where to set energy positions for the range rather than the headline, and how to size the AI-infrastructure overweight without adding into record crowding. It also lays out the seven risk scenarios — from a $150-160 oil failure tail (30-40%) to a Warsh hike against a crowd priced for holds, to the consumer cliff accelerating through Q3 (45-55%). Full options positioning analysis, portfolio playbook, and risk scenario framework below for subscribers.

This publication is for informational and educational purposes only and does not constitute financial, investment, or trading advice. The analysis, opinions, and commentary presented here should not be interpreted as a recommendation to buy, sell, or hold any security. Always conduct your own research and consult a qualified financial advisor before making investment decisions. Past performance does not guarantee future results.