Ceasefire Unravels in 24 Hours as Hormuz Standstill Persists and $20 Billion in Private Credit Redemptions Surface

Fed minutes reveal growing openness to rate hikes on the same day markets reprice to 43% cut probability — the largest disconnect in current pricing.

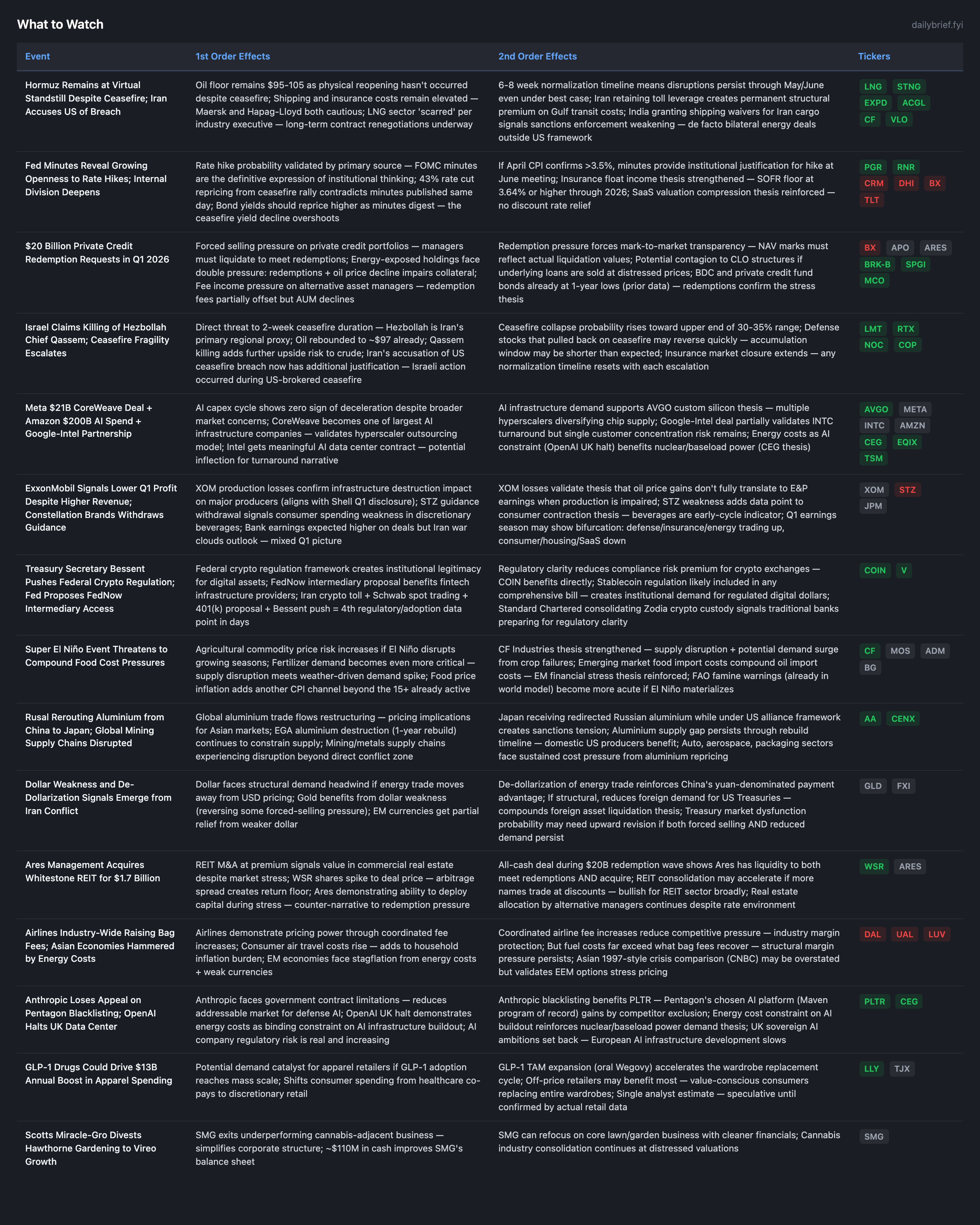

The ceasefire rally is unwinding within 24 hours. Oil rebounded above $97 as Iran accused the US of breach, Israel claimed killing Hezbollah chief Qassem, and Reuters confirmed shipping through Hormuz remains at a virtual standstill. The ADNOC CEO stated the strait is “effectively shut.” Hapag-Lloyd estimated 6-8 weeks for normalization even under a stable peace. These developments validate the world model’s 30-35% ceasefire collapse probability and confirm the ceasefire is functioning as a pause in hostilities, with supply disruption unresolved.

The most important new data point since yesterday’s brief is the FT report that $20 billion in redemption requests hit private credit funds (Apollo, Ares, Blackstone) in Q1 2026. The 16th+ independent data point supporting the credit cascade thesis, it is also the most operationally concrete: actual redemption demands create forced selling pressure that converts paper losses into realized losses. Combined with HYG’s 33.3% near-term IV spike yesterday and today’s normalization to 7.1% (now in contango), two interpretations compete. Either the 33.3% spike was a technical distortion that has resolved, or the event it was pricing has been deferred by a single day. The shift from backwardation to contango in HYG is the largest change in the options data since the crisis began.

The Fed released March FOMC minutes showing growing openness to rate hikes, published the same day markets repriced to 43% cut probability. These signals collide: the bond market is pricing one thing (ceasefire → rate cuts), while the institution that sets rates is signaling the opposite (inflation persistence → potential hikes). Core PCE at 3.0% in February was already rising for a third consecutive month before the war. Super El Niño risk adds a potential 16th CPI channel. I maintain the assessment that the 43% cut repricing is the most likely error in current market pricing and will reverse over the next 2-4 weeks as April CPI data arrives.

Hormuz Standstill: Supply Disruption Persists Through Ceasefire

Fewer tankers are passing through Hormuz than during the fiercest days of fighting (FT, Tier 2). ADNOC CEO Al Jaber stated the strait must reopen “without conditions” (Reuters, Tier 1). Hapag-Lloyd estimated 6-8 weeks for shipping normalization once stability is achieved (Reuters, Tier 2), meaning even under the best case, disruptions persist through late May.

Iran’s toll booth structure prevents normalization. Reuters analysis (Tier 1) describes Iran’s ability to impose de facto tolls as structurally embedding higher energy prices regardless of diplomatic progress. The crypto payment requirement makes P&I club re-entry operationally impossible — no major insurer can authorize payments to a sanctioned entity without regulatory risk. Iran’s coercive leverage persists through and beyond the ceasefire.

Supply chain disruption has now extended well beyond oil. Multiple industry sources confirm impacts on Indian pharmaceutical exports, Asian semiconductor shipments, oil-derived chemical products, and fashion/textiles (IBJ, PharmExec, ZAWYA, Manila Standard — all Tier 3 but collectively forming a pattern across 4+ independent sources). The 6-8 week normalization applies to all these supply chains, not just crude.

Russia’s oil revenue doubling to $9 billion in April (Reuters, Tier 1) is a second-order factor. Moscow has a financial incentive to prolong Hormuz disruption. Combined with China’s preferential access through yuan payments, two major geopolitical actors benefit from the current disruption, reducing the probability that either will push aggressively for resolution.

Fed Minutes vs. Market Pricing

The March FOMC minutes (Federal Reserve, Tier 1 — primary source) published April 8 show a “growing faction” open to rate hikes. Officials stated they need to remain “nimble” on war impacts. The same institution’s rate futures market simultaneously repriced to 43% cut probability.

The disconnect is explained by what the minutes capture vs. what the market is pricing. The minutes reflect pre-ceasefire deliberation (March 17-18 meeting). The 43% cut probability reflects post-ceasefire euphoria. Which proves more durable? I assess the minutes are more informative because: (1) Core PCE at 3.0% was rising before the war and the war’s inflationary channels haven’t been reversed by a 2-week ceasefire; (2) diesel at $5.29/gallon is embedded in trucking costs through existing contracts; (3) 14+ non-oil CPI channels remain active; (4) Musalem, IMF, Wells Fargo, and now the minutes themselves all signal hold-or-hike.

The 5Y breakeven at 2.56% (FRED, April 8) actually dropped 5bps — the market is pricing less inflation after the ceasefire. The world model’s central case for H2 2026 core inflation remains 3.8-4.3%. The gap between market-implied inflation (2.56%) and model-expected inflation (3.8-4.3%) is 120-180bps. This is either the largest inflation mispricing since 2021 or the world model is wrong. I maintain the model because 15+ active channels support it and only one (oil) has partially eased.

Private Credit: Redemptions Make the Cascade Operational

The FT’s $20 billion redemption report moves the private credit cascade from a positioning thesis to an operational reality. Prior data points were directional indicators (HYG OI P/C, Dimon warning, private credit bond declines). Redemption requests force managers to either liquidate assets at potentially distressed prices or gate investors, creating further confidence damage.

The timing matters. These are Q1 requests being processed now, meaning they were filed before the ceasefire and before oil crashed from $115 to $94. The oil decline creates an additional impairment vector: E&P borrowers who were generating strong cash flows at $115 face covenant pressure at $95-100, reducing the recovery value on exactly the assets that need to be sold to meet redemptions.

Ares’ simultaneous $1.7 billion Whitestone REIT acquisition demonstrates that not all alternative managers are equally stressed — Ares has sufficient liquidity to both meet redemptions and deploy capital. This differentiates ARES from BX, where gating + CLO exposure + energy-exposed private credit creates a more concentrated risk profile.

Bill Ackman exploring a “complacency fund” (FT, Tier 2) is an additional signal: a major macro investor who generated returns during COVID by betting on tail risk sees similar conditions now. Combined with Muddy Waters’ credit short (MarketWatch, Tier 2 from prior brief), two independent prominent investors are positioning for credit stress. Both are experienced macro practitioners with track records in tail-risk positioning.

Credit cascade probability: maintained at 55-65%. The $20 billion redemption figure is the most concrete data point yet. Write-downs <3% → 48-55%. >8-10% → 68-75%.

AI Capex: $220 Billion Committed

Meta’s $21 billion CoreWeave deal, Amazon’s $200 billion AI spend defense, and Google’s Intel chip partnership were all disclosed within 24 hours. Total committed capital now approaches $300 billion across hyperscalers.

The Google-Intel partnership is the novel signal. Prior AI infrastructure deals routed through TSMC (AVGO, AMD, custom silicon). Google committing to multiple generations of Intel CPUs and custom chips for AI data centers represents the first major hyperscaler diversifying fabrication away from TSMC dependency. This is strategically rational (Taiwan risk) but doesn’t immediately solve Intel’s fundamental problems (106x FY2026E, negative FCF, Altman Z 1.48). A single customer deal does not constitute a turnaround. I move Intel from AVOID to monitoring on this development but require Q1 earnings confirmation before any conviction shift.

OpenAI halting its UK Stargate data center over energy costs and regulatory uncertainty is the key negative signal. Energy costs are becoming a binding constraint on AI infrastructure expansion globally. This directly supports the nuclear baseload thesis (CEG) and explains why AI companies are concentrating buildout in US locations with reliable, affordable power.

Ceasefire Fragility: Three Threats in 48 Hours

Three distinct events threaten the ceasefire within its first 48 hours: (1) Saudi pipeline attack during the ceasefire (already documented); (2) Iran accusing the US of violating terms; (3) Israel claiming to have killed Hezbollah chief Qassem. The Qassem killing is the most destabilizing because Hezbollah is Iran’s primary regional proxy, and Iranian domestic politics make it difficult to continue negotiations while a major ally’s leader has been killed.

Combined with Trump warning military to “stay near Iran” and his “next conquest” rhetoric (CNBC/FT, Tier 2), the ceasefire reads as a tactical pause. The Senate vote on Iran war powers resolution could provide a domestic political constraint on re-escalation, but its passage is uncertain.

I revise ceasefire collapse probability upward to 35-40% (from 30-35%) based on the Qassem killing adding a third destabilizing event.

What to Watch

The options data beneath these headlines tells a more complex story than the ceasefire narrative suggests. Japan’s EWJ is now printing 58.6% near-term IV — the highest reading for any market tracked during the entire crisis — and it’s increasing each day even as ceasefire euphoria supposedly reduces risk. HYG’s dramatic shift from 33.3% backwardation to 7.1% contango in a single session is either the resolution of a credit scare or the deferral of one, and the $20 billion redemption report arriving the same day makes the latter interpretation hard to dismiss. Meanwhile, TLT call buyers are piling in at a 0.08 volume put/call ratio — 94% calls — betting aggressively on lower yields at the exact moment FOMC minutes signal hike openness. Full options positioning analysis, portfolio playbook, and risk scenario framework below for subscribers.

This publication is for informational and educational purposes only and does not constitute financial, investment, or trading advice. The analysis, opinions, and commentary presented here should not be interpreted as a recommendation to buy, sell, or hold any security. Always conduct your own research and consult a qualified financial advisor before making investment decisions. Past performance does not guarantee future results.