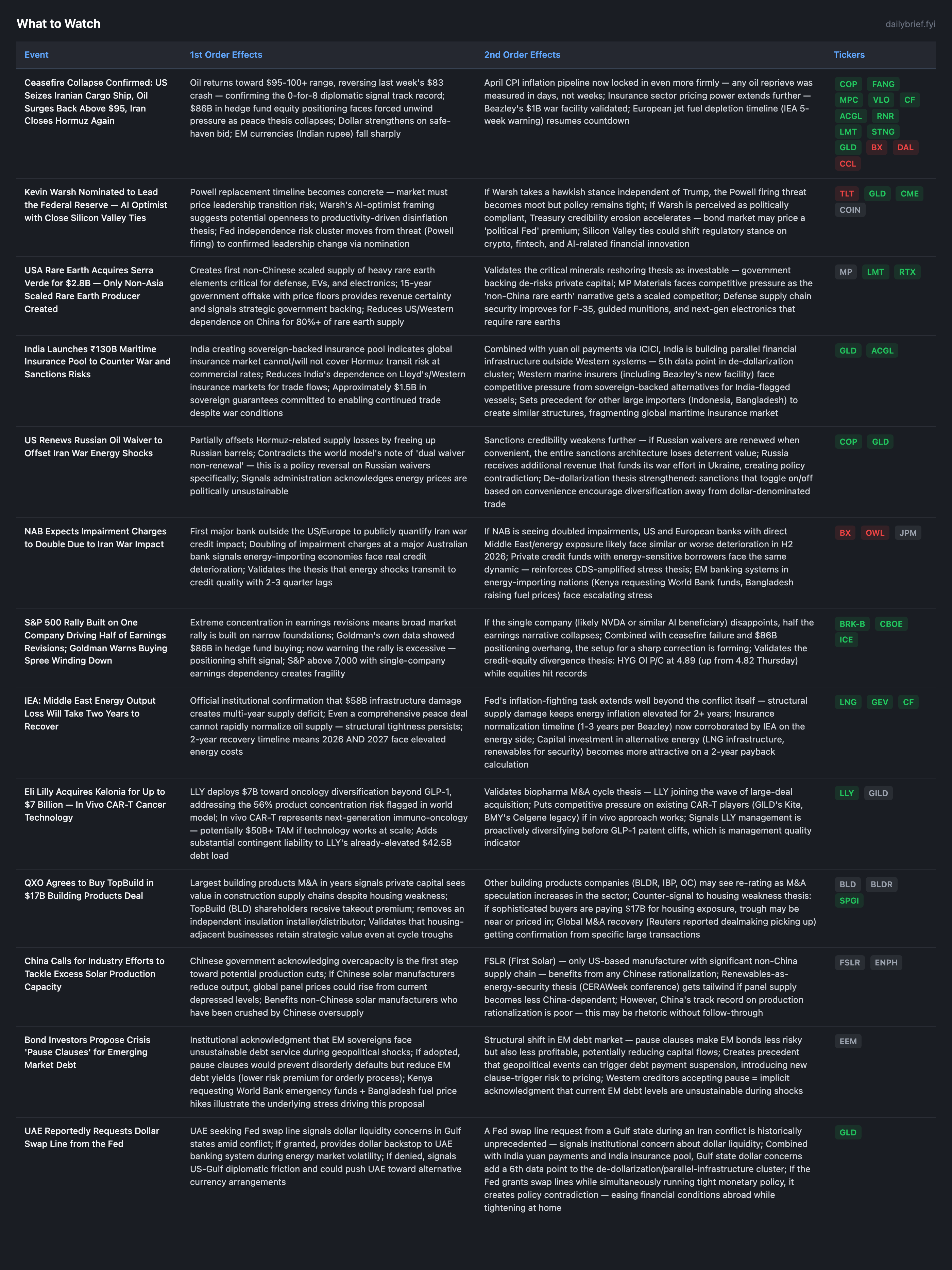

Ceasefire Collapses in 72 Hours as US Seizes Iranian Ship; $86B Hedge Fund Unwind Looms

Kevin Warsh's Fed nomination and IEA's 2-year recovery timeline add structural dimensions to a crisis the options market is rapidly repricing.

The 10-day ceasefire lasted approximately 72 hours in practice. The US seized an Iranian cargo ship on April 19, Iran vowed retaliation, closed the Strait of Hormuz again, and rejected further peace talks. Oil surged back above $95. The 8th optimistic diplomatic signal has now reversed, maintaining the 0-for-8 track record within the stated 24-72 hour window. The market has $86B in hedge fund equity positioning to unwind, creating mechanically severe downside risk as the peace thesis collapses.

The options market has snapped back to pricing imminent stress: SPY near-term IV jumped from 12.8% (Thursday) to 21.4% today. HYG OI P/C reached 4.89 — six consecutive sessions of widening. Credit investors who maintained their positions through the entire ceasefire-to-collapse cycle were correct. The institutional credit community’s refusal to participate in the rally is the most persistent signal of this crisis.

Two genuinely new developments demand attention: Kevin Warsh’s nomination to replace Powell at the Fed (adding a fourth dimension to the Treasury credibility erosion thesis), and the IEA’s official confirmation that Middle East energy output will take two years to recover regardless of diplomatic outcomes. Both operate on timelines far longer than any ceasefire window.

Ceasefire Collapse: The Pattern Holds, but Scale Is Different

The US seizure of an Iranian cargo ship — with reports of shots fired — followed by Iran’s refusal to attend peace talks and closure of Hormuz represents a qualitatively different failure than prior diplomatic reversals. Previous collapses involved rhetorical escalation. This involved kinetic action during what was nominally a ceasefire period. The US military is preparing to board additional Iran-linked vessels in coming days (WSJ), suggesting deliberate escalation rather than an accident.

The investment consequences are immediate and mechanical. Goldman’s $86B hedge fund equity buying was predicated on peace; that thesis has failed within 72 hours. The unwind creates selling pressure beyond normal geopolitical risk aversion because it’s concentrated, leveraged, and directional. Prior oil round-trips during this conflict (April 9: $107→$94→$97) produced 2-3 day periods of elevated equity volatility. This time, the entry point is from higher prices (S&P at all-time highs, 7,000+) and the positioning is larger.

The multinational Hormuz security mission (12+ countries, per UK PM Starmer) provides a structural framework for eventual stabilization but cannot prevent near-term operational disruption. The gap between “countries volunteering to participate” and “operational naval presence enforcing safe passage” is measured in months.

Kevin Warsh Nomination: Fourth Vector of Treasury Credibility

Warsh’s nomination transforms the Fed independence risk from a hypothetical (Trump threatening Powell) to a concrete leadership transition. The FT reports he seeks major changes at the central bank but faces potential confrontation with Trump over rates. This creates several simultaneous uncertainties:

Confirmation timeline uncertainty (months of Senate process)

Policy direction uncertainty (Warsh has not stated rate views for current conditions)

Political pressure uncertainty (will he resist Trump on rates?)

Institutional change uncertainty (what “major changes” does he seek?)

For positioning purposes: the Fed leadership transition adds a fourth vector to the Treasury credibility assault previously identified (political, institutional, market-based). TLT, which last week priced zero risk at 9.8% near-term IV, has already moved to 17.2% near-term in backwardation. The options market is beginning to price the disconnect our structural analysis identified.

IEA 2-Year Recovery Confirmation

The IEA’s statement that energy production capacity lost during the conflict will require approximately two years to recover is the most important structural data point of the weekend. It transforms the investment timeline: even a comprehensive peace deal signed tomorrow cannot normalize energy supply until 2028. This makes the ceasefire cycle analytically less relevant for structural positions. CF Industries at 9.3x with 40% of nitrogen through Hormuz, LNG infrastructure plays, and energy producers all benefit from 2-year supply deficit confirmation rather than day-to-day diplomatic noise.

Reuters separately quantified $50 billion in lost oil supply over 50 days of conflict, providing a per-day loss rate of approximately $1B. Each additional day of Hormuz disruption compounds the structural damage.

$760M Oil Short Ahead of Hormuz Announcement — Informed Trading Signal

The $760 million bet on falling oil placed ahead of Friday’s Hormuz reopening announcement raises significant questions about information asymmetry. Either (a) someone had advance knowledge of Iran’s announcement, or (b) it was a speculative bet that happened to be right for 48 hours before being wrong. The reversal means these shorts are now losing money as oil surges back above $95. If this was informed trading, it suggests the diplomatic channel has significant leakage, which reduces the surprise value of future announcements to well-connected capital.

Credit-Equity Divergence: Day 6, Resolution Underway

The resolution appears to be happening in the direction the credit signal predicted: equities are repricing toward the risk environment that credit investors never stopped hedging. Historical base rate (~70%) for credit signal winning continues to hold.

The private credit CDS instruments launched last week now have their first test case: how do spreads behave during an escalation cycle with live trading available? March 31 NAV marks are entering reporting pipelines this week. The combination of active CDS trading + NAV disclosures + escalated geopolitical stress creates peak catalyst density for the next 2-3 weeks.

Consumer Spending: $4 Gas Pulling Back Entertainment and Dining

CNBC reports consumers are measurably reducing entertainment and dining spending due to fuel costs. March retail sales showed 6.59% YoY growth, but this was supported by larger-than-usual tax refunds — a one-time factor that fades in April. With Hormuz re-closed and oil above $95, the consumer spending headwind intensifies. This confirms the 6th+ consecutive consumer weakness signal and reinforces the AVOID mandate for all discretionary names.

Argentina Wheat Threatened by Fertilizer Costs

The Reuters report on Argentina’s wheat crop being threatened by urea fertilizer prices provides the 16th+ confirmation of the CF Industries thesis. The causal chain now spans multiple continents: Hormuz closure → Iran petrochemical halt → urea doubles globally → Argentina farmers reduce wheat planting → global grain supply tightens → food CPI rises worldwide. Each geographic data point reinforces the same underlying dynamic.

Continuing Themes

Iran conflict: Ceasefire reversed within 72 hours (0-for-8). Oil back above $95. Hormuz closed again. No framework agreement exists. Physical damage requires 2 years to rebuild (IEA). Structural positions in energy, fertilizer, defense, and insurance maintained and reinforced.

Fed policy: Unanimous hold at 3.64%. Warsh nomination adds transition uncertainty. Rate cut probability remains 3-5%. No change to the inflation pipeline analysis — April CPI captures full month of $100+ oil regardless of this week’s price action.

AI infrastructure: No new data this weekend. TSMC/ASML validation from last week unchanged. CoreWeave leveraged-edge concern persists within the broader credit stress context.

Defense: US weapons delivery delays to European allies confirmed. Japan’s first warship export deal (Mitsubishi Heavy to Australia) validates the global defense spending thesis from a new geography. LMT Q1 earnings this week remain the key catalyst.

What to Watch

The options market repricing is telling a clear story beneath the headlines. SPY near-term IV nearly doubled in a single session to 21.4%, IWM hit 36.4% — its highest since the initial blockade — and GLD’s extreme call-heavy OI (0.46 P/C) with 38.3% near-term IV shows institutional safe-haven rotation accelerating. Meanwhile, the credit market’s persistent signal (HYG OI P/C at 4.89, six consecutive sessions widening) is being validated as equities reprice toward the risk environment credit investors never left. With March 31 private credit NAV marks entering reporting pipelines this week alongside live CDS trading, the next 2-3 weeks represent peak catalyst density for the credit cascade thesis. Full options positioning analysis, portfolio playbook, and risk scenario framework below for subscribers.