Berkshire's Massive GOOG Bet and Buffett's Airline Contrarianism Reshape Positioning as Structural Bond Stress Deepens

Home Depot's earnings beat weakens the near-term credit cascade thesis, but Japan and China's confirmed Treasury selling locks in a higher-rates regime the Fed cannot escape

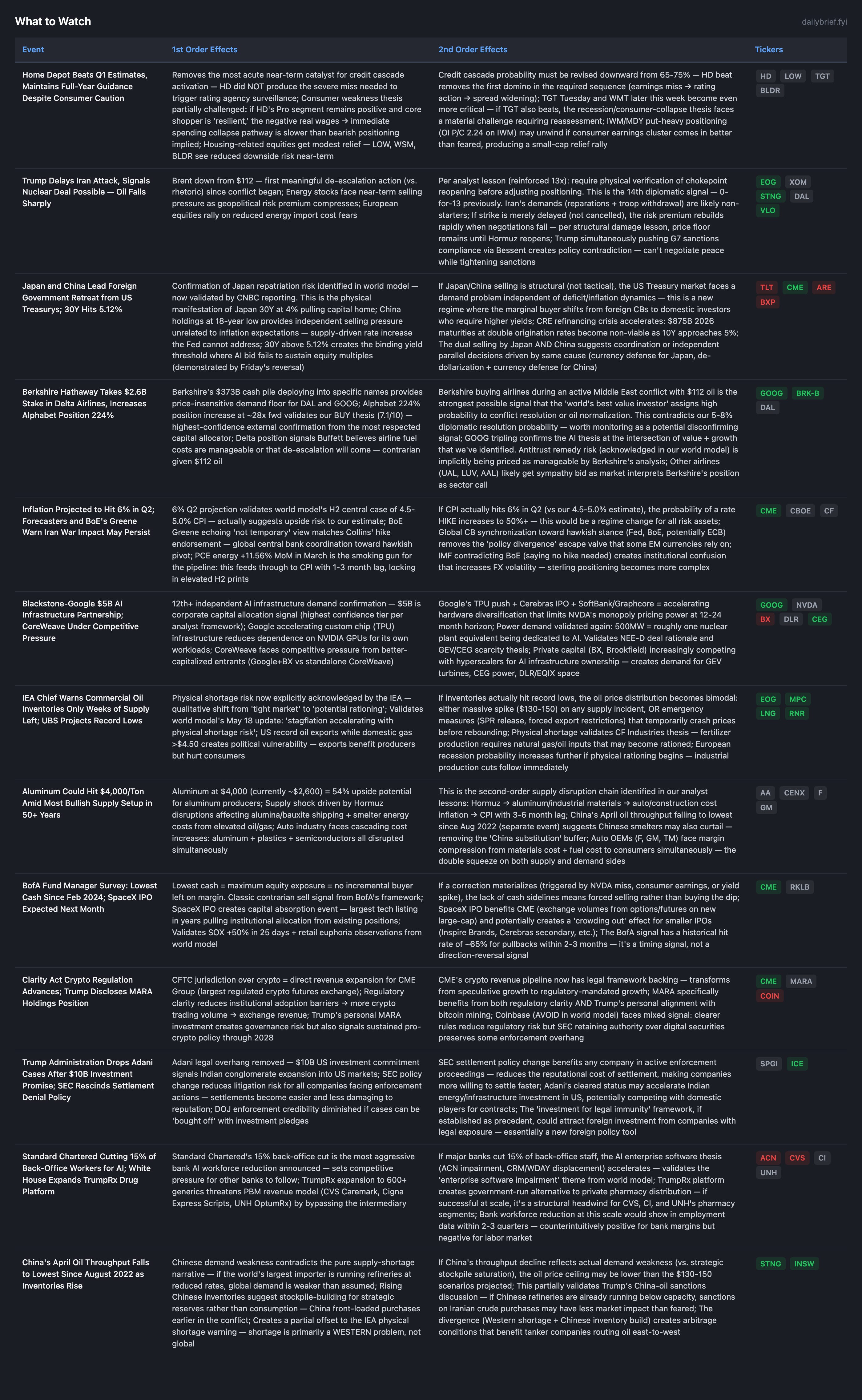

Two events today shift the near-term catalyst picture from the prior brief’s framework: Home Depot beat earnings estimates (contradicting our 55-65% miss probability) and Trump delayed a planned Iran strike citing nuclear deal prospects (the 14th diplomatic signal in the 0-for-13 streak). These developments weaken both legs of the near-term bear thesis — consumer collapse triggering credit cascade, and energy supply further tightening.

However, the structural picture worsened: Japan and China are confirmed actively selling US Treasurys (China at 18-year low), inflation forecasters project 6% in Q2, and the IEA chief confirms only weeks of oil inventory remain. The HD beat is a single data point against 22+ consumer weakness signals; the Iran pause is the 14th failed diplomatic signal. Neither reverses established theses but both reduce immediate catalyst probability.

The most actionable new signal: Berkshire’s 224% increase in Alphabet and $2.6B Delta position provides the highest-confidence external validation for GOOG’s BUY thesis and a potential disconfirming signal for our Iran conflict persistence view. When the world’s most disciplined capital allocator buys airlines during a $112 oil/Hormuz blockade, either they know something about resolution timing or they believe Delta’s economics can sustain current fuel costs. Either interpretation demands attention.

New Developments

Home Depot Beat: Credit Cascade Probability Revision Required

HD’s Q1 beat (sales +5%, EPS beat, maintained full-year guidance) directly contradicts the thesis that consumer earnings would trigger credit cascade activation. The prior brief assigned 55-65% miss probability; the outcome was a beat on reduced expectations. Management cited “core shopper resilience” despite $4.50+ gas, challenging the “negative real wages → immediate spending collapse” mechanism.

Credit cascade probability moves from 65-75% to 50-60%. HD was the first and most important domino; its failure to fall weakens the cascading repricing mechanism. TGT Tuesday becomes the remaining conversion test — if TGT also beats (estimates revised up 4.8% over 90 days), the consumer-collapse thesis faces a genuine challenge requiring material reassessment.

Qualification: HD’s Pro segment (positive 5 consecutive quarters) skews results toward commercial/contractor demand rather than consumer discretionary. Same-store sales still missed slightly. Homeowners are explicitly “deferring large projects” — suggesting weakness is deferred rather than absent. The bearish thesis survives but the timeline extends.

Japan/China Treasury Selling Confirmed

CNBC confirms Japan and China leading foreign government retreat from USTs, with China at 18-year holdings low. This validates the world model’s May 18 identification of “Japan 30Y at 4% → repatriation risk” as a genuine structural development. We now have hard reporting (not just mechanism theory) that the $1.1T Japanese and $0.8T Chinese UST holdings are declining simultaneously.

The mechanism chain: foreign selling → higher yields independent of inflation → wider Treasury auction tails → fiscal sustainability questions emerge → further selling. This is a reflexive loop the Fed cannot easily address because it cannot cut rates (inflation too high) or absorb supply (QE restart would be politically impossible with 6% PPI).

The 30Y at 5.12% is now confirmed as a structural threshold, not transient. The probability of 10Y breaking 5% within 60 days revised upward from 45-55% to 50-60%.

Trump Iran Pause: 14th Signal, Same Framework Applies

Trump delayed a Tuesday strike citing nuclear deal prospects. Iran’s counter-proposal demands reparations and full US troop withdrawal — conditions that are almost certainly non-starters. Per our analyst lesson (reinforced 13 times): “Discount vague diplomatic signals without operational specifics — require physical verification of chokepoint reopening.” This is signal #14 in a series that has produced 0 actual resolutions.

However, this signal differs from prior rhetoric in one respect: it’s an actual operational military decision (pausing a strike), not just words. Pakistan simultaneously deploying troops to Saudi Arabia, Bessent pushing G7 sanctions compliance, and IEA confirming weeks-of-supply remaining all contradict the de-escalation interpretation.

Assessment: 10-15% probability this pause leads to meaningful negotiations within 2 weeks. 85-90% probability the strike is merely delayed and escalation resumes.

Berkshire’s Dual Signals: GOOG Validation + DAL Contrarian

The 224% Alphabet increase is the strongest possible BUY validation from outside our system. Buffett/Combs allocating aggressively at ~28x forward into a company with $180-190B capex commitment and antitrust remedy risk means their analysis concludes the AI value creation exceeds these headwinds by a wide margin.

The Delta $2.6B position is more puzzling. At $112 Brent, airline fuel costs are at extreme levels. Either: (a) Berkshire assigns >50% probability to meaningful oil price decline within 12 months, (b) Delta’s pricing power/hedging strategy is more robust than market assumes, or (c) Berkshire is positioning for eventual normalization with a multi-year holding period accepting near-term pain. Per our framework, corporate capital allocation signals from the highest-quality allocators demand serious attention even when they contradict our thesis.

Aluminum $4,000/Ton Scenario: Second-Order Supply Chain Broadening

Analyst projections of aluminum at $4,000/ton (”largest supply shock in 50+ years”) quantify the Hormuz disruption’s non-oil inflation channel. This directly feeds our “multi-channel inflation” thesis — aluminum affects construction, autos, packaging, aerospace, and electronics simultaneously with 3-6 month lags to CPI.

Combined with Australian wheat production decline (farmers planting less due to fuel/fertilizer costs) and pharmaceutical supply chain delays, the supply disruption is now confirmed across 5+ distinct commodity/industrial channels: oil, aluminum, wheat, pharmaceuticals, plastics. Each has independent CPI lag characteristics, meaning inflation pressure arrives in waves through H2 2026 regardless of oil price direction.

Developing Themes

Credit Cascade: Probability Downgraded on HD Beat

HYG maintains contango (5.1% near vs 8.0% at 12-month), OI P/C at 3.79 (down from 3.66 in world model). Credit calm persists. TGT Tuesday is now the remaining high-confidence test.

Fed Policy: Hike Probability Rising

Kalshi pricing 38% probability of rate hike by Dec 2026 (up from 34% in prior reference). Forecasters projecting 6% Q2 inflation. Yardeni explicitly calling for July hike. Collins already endorsed. Warsh confirmed — sworn in Friday. The convergence of data (PPI 6%, CPI 3.8%, PCE energy +11.56% MoM) with personnel (hawkish Warsh + Collins) and market pricing (30Y >5.1%) makes a hike scenario more plausible than a cut.

Warsh Swearing-In Friday: Communication Regime Begins

World model identified Warsh’s “keep quiet” philosophy as structural regime change for rates vol. Any communication from his first week will carry amplified signaling power given the baseline expectation of silence. Markets will parse personnel choices, event attendance, and any prepared remarks with unusual intensity.

Continuing Themes

Iran conflict: 14th diplomatic signal (Trump pause); 0-for-13 prior record. Pakistan deploying to Saudi Arabia = institutionalizing. Physical shortage confirmed (IEA, UBS). Energy maximum overweight maintained pending physical verification of de-escalation.

AI demand: 12th+ confirmation (Google-BX $5B). Zero counter-signals. NVDA Wednesday = next test. Hardware diversification accelerating (Google TPU push + Cerebras + Graphcore).

European stress: VGK at 23.8% near-term IV (+8.3pp vs HV). Physical oil shortages expected within weeks. UK employer confidence near record low. Recession probability >60%.

Bond market: Japan/China selling confirmed. Structurally higher rates regime. TLT term structure flattened from prior extreme backwardation (now 14.1% near vs 15.3% far).

What to Watch

The options market is telling a more nuanced story beneath today’s headlines: EEM backwardation hit the most extreme level across all ETFs at +14.5pp over HV, signaling acute emerging market stress even as SPY vol compressed from 24.5% to 16.4% on the dual positive developments. QQQ’s 1-week put skew at -14.6% reveals extreme call buying ahead of NVDA Wednesday — a contrarian bearish signal when consensus expects a beat at $5.7T market cap. Meanwhile, GLD’s normalization from 43.9% to fair value confirms the gold exit thesis was correct, but the shift reflects rate hike expectations dominating safe-haven flows. The premium section below details how to position around these divergences, the specific hedge structures warranted by 50-60% credit cascade probability, and the five risk scenarios (including 6% Q2 inflation forcing a Warsh-era hike) that frame this week’s decision tree.

Full options positioning analysis, portfolio playbook, and risk scenario framework below for subscribers.

This publication is for informational and educational purposes only and does not constitute financial, investment, or trading advice. The analysis, opinions, and commentary presented here should not be interpreted as a recommendation to buy, sell, or hold any security. Always conduct your own research and consult a qualified financial advisor before making investment decisions. Past performance does not guarantee future results.