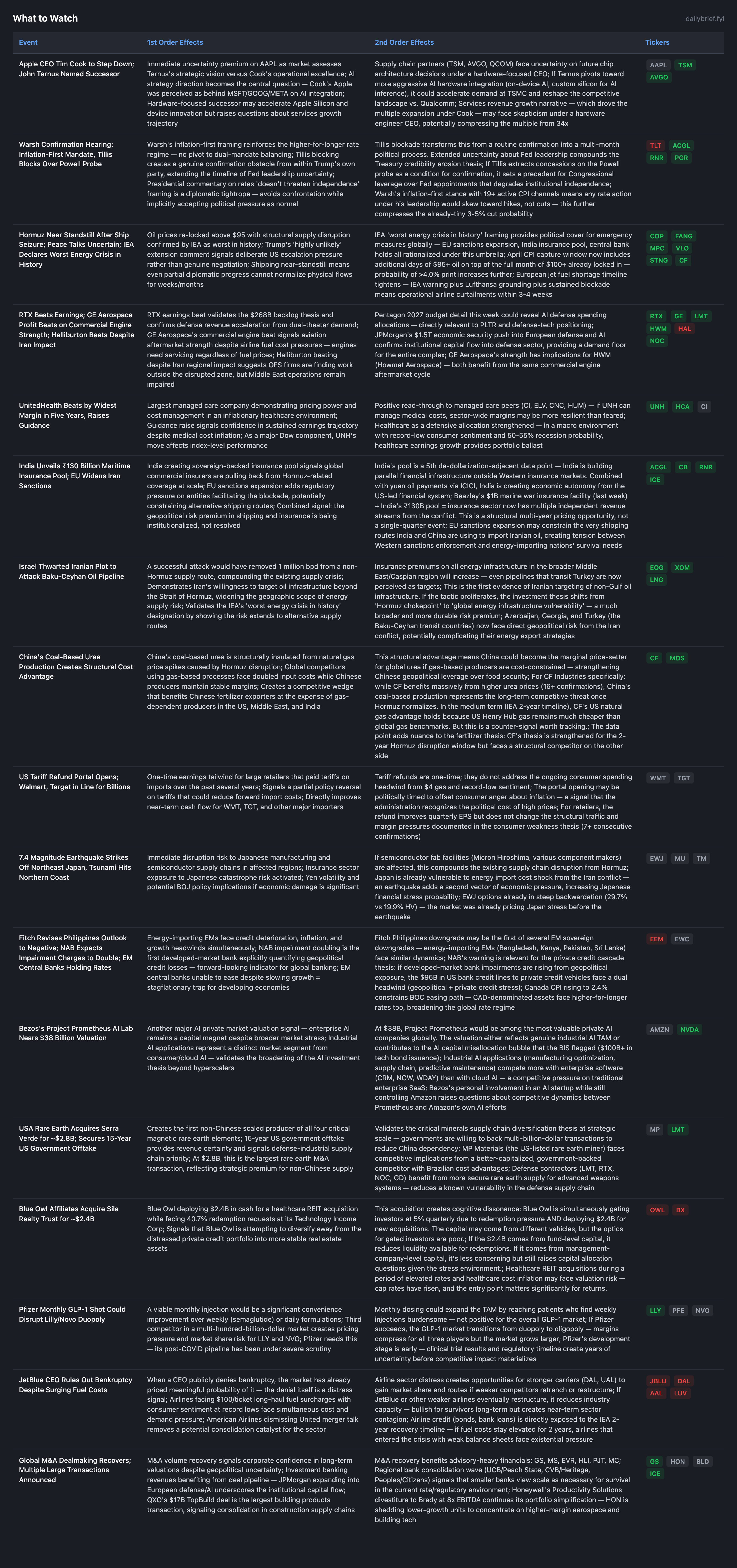

Apple's Largest Leadership Change in a Decade, Fed Confirmation Crisis and a Widening Energy War

Iran's attempted sabotage of the Baku-Ceyhan pipeline reveals infrastructure targeting beyond Hormuz as credit stress signals hit their seventh consecutive daily escalation.

The macro landscape shifted in two material ways since yesterday’s brief. First, the Apple CEO transition — Tim Cook stepping down for hardware chief John Ternus — is the largest mega-cap leadership change in a decade and introduces strategic uncertainty around AI positioning at the world’s most valuable company. Second, Warsh’s confirmation hearing revealed both an inflation-first mandate and a new political obstacle: Republican Senator Tillis blocking the nomination over Trump’s Powell probe, extending the Fed leadership uncertainty from months to potentially a year or more.

Trump described ceasefire extension as “highly unlikely” without a deal, Vance has not departed for Pakistan, and Israel revealed it thwarted an Iranian plot to attack the Baku-Ceyhan pipeline — the first evidence of Iranian targeting of non-Gulf oil infrastructure, which widens the geographic scope of energy supply risk beyond Hormuz. Meanwhile, RTX, GE Aerospace, and Halliburton all beat earnings expectations, validating the defense and aviation aftermarket theses while confirming that OFS firms are impaired by regional disruption. UnitedHealth posted its largest earnings beat in five years and raised guidance, strengthening the healthcare defensive allocation.

New Developments

Apple CEO Succession: The AI Strategy Question

Tim Cook transitioning to executive chairman and John Ternus becoming CEO introduces strategic discontinuity at a $3.4 trillion company. Ternus is a hardware engineer who led Apple’s chip and device engineering. The FT specifically flags that Cook leaves AI strategy “as an unresolved challenge.”

The market implications bifurcate. A hardware-focused CEO could accelerate Apple Silicon development and on-device AI inference capabilities, which would be bullish for TSMC (Apple accounts for roughly 25% of revenue), Broadcom, and the advanced packaging supply chain. Apple’s Neural Engine in its custom chips could be more aggressively developed under someone who understands the physics.

The risk is to the services narrative. Cook’s Apple achieved a 75%+ gross margin services business generating $85B+ annually. The stock’s multiple expansion from ~15x to 34x over the past decade tracked the transformation from a hardware company to a services platform. Ternus’s track record is in product engineering, not platform economics. If the market concludes that services growth trajectory is at risk, the multiple should compress. At 34x, AAPL is in the world model at HOLD with a BUY trigger at $195-210. The succession creates execution risk that pushes any BUY trigger further out.

Warsh Hearing: Inflation-First With a Tillis Complication

Warsh’s Senate testimony produced the expected inflation-first framing, but the genuinely new development is Tillis’s block. A Republican senator opposing a Republican president’s Fed nominee over the Powell investigation creates an internal party conflict that could delay confirmation by months. This transforms the four-vector Treasury credibility assault (political, institutional, market-based, leadership transition) from a theoretical framework into a practical governance problem: who runs the Fed if Warsh is delayed and Trump follows through on the Powell probe?

The inflation-first stance, combined with minimal labor market mention, signals that a Warsh-led Fed would be structurally hawkish. For the rate path: the 3-5% cut probability is confirmed, the 35-45% hike probability is maintained, and the confirmation process itself becomes a source of uncertainty that the market must price for longer. Insurance companies (ACGL, RNR, PGR, CB) benefit from the extended certainty that float income remains elevated.

Baku-Ceyhan Pipeline Plot: Geographic Escalation of Energy Risk

Israel’s disclosure that it thwarted an Iranian attack on the Baku-Ceyhan pipeline is the most consequential new security signal today. This pipeline carries 1 million bpd of Caspian crude through Azerbaijan, Georgia, and Turkey to Mediterranean markets — a non-Hormuz supply route that was supposed to be a diversification hedge.

Iranian targeting of pipelines outside the Persian Gulf shifts the investment thesis from “Hormuz chokepoint risk” to “global energy infrastructure vulnerability.” The former is bounded by the geography of the Strait; the latter has no geographic bound. This raises the structural risk premium on all energy infrastructure and strengthens the case for US domestic production (COP, FANG, EOG), which faces no pipeline targeting risk, and for LNG exports, which transit by tanker rather than fixed pipeline.

The insurance implications are direct: marine war insurance pricing now must account for pipeline and infrastructure targeting beyond the traditional war zone. Beazley’s $1B marine war facility and India’s ₹130B sovereign insurance pool both make more sense in a world where Iranian targeting extends to pipelines in Turkey.

China’s Coal-Based Urea: A Counter-Signal Worth Tracking

Reuters’ analysis of China’s coal-based urea production provides the first genuine counter-signal to the CF Industries thesis. Chinese producers use coal (cheap, domestically available) rather than natural gas (expensive, Hormuz-exposed) to make urea. Chinese fertilizer output is therefore structurally insulated from the supply disruption that benefits CF.

This does not change the 2-year thesis. US Henry Hub natural gas remains the cheapest gas feedstock globally, giving CF a cost advantage over all gas-based competitors. During the IEA’s 2-year recovery timeline, gas-based producers outside the US face ruinous input costs while CF’s US operations benefit from cheap domestic gas and elevated urea prices. But post-normalization, China’s coal-based production represents the structural competitive threat that caps CF’s long-term pricing power. Logging this as counter-signal #1 against 16+ confirmations — the thesis is unchanged but the analytical burden now includes monitoring Chinese urea export policy and coal pricing.

Blue Owl’s Sila Realty Acquisition: Contradictions Compound

Blue Owl affiliates deploying $2.4B to acquire a healthcare REIT while simultaneously gating investors at 5% quarterly due to 40.7% redemption requests crystallizes the contradictions in the private credit model. The capital likely comes from different vehicles, but the optics for Technology Income Corp investors — told they cannot access their money while the management company deploys billions elsewhere — are destructive for trust.

This strengthens the ARES/OWL pair trade. OWL’s 68% equity decline, 14.65% short interest, Moody’s negative outlook, and misrepresented software exposure are now compounded by capital allocation decisions that appear tone-deaf to the redemption crisis. AVOID maintained at maximum conviction.

Developing Themes

Earnings Season Validates Structural Positions

RTX beat (defense), GE Aerospace beat (commercial engines), UNH beat by widest margin in 5 years (healthcare), Halliburton beat (energy, though Middle East impaired). Each confirms existing portfolio tilts: defense OVERWEIGHT (dual-theater demand + Pentagon 2027 budget detail this week), healthcare defensive (UNH guidance raise validates managed care pricing power), energy OVERWEIGHT (structural supply deficit), OFS BEARISH (HAL’s Middle East operations impaired despite overall beat).

The Nasdaq’s 13-day winning streak ending is consistent with positioning risk: the streak was driven by TSMC/ASML earnings and peace thesis positioning. With the ceasefire collapsing, the tech-heavy index faces the unwinding of both catalysts.

Consumer Spending: Tax Refund Tailwind Fading

March retail sales at 6.59% YoY were explicitly supported by larger-than-usual tax refunds. Goldman Sachs is now warning of “challenging months ahead” for US consumers. This aligns with record-low Michigan sentiment (47.6), CNBC’s confirmation of entertainment/dining pullback, and the IEA 2-year timeline that keeps gas above $4. The tariff refund portal opening for Walmart/Target is a one-time item that does not change the structural trajectory. Consumer discretionary AVOID maintained for the 8th+ consecutive signal.

M&A Recovery Supports Exchange and Advisory Revenue

Multiple large transactions (QXO/$17B TopBuild, Lilly/$7B Kelonia, USA Rare Earth/$2.8B Serra Verde, several regional bank deals) signal that corporate boards are looking through the conflict to execute strategic moves. This directly benefits ICE (listing + clearing + data), CME (derivatives around deal activity), and investment banks (GS, MS). The M&A recovery operates independently of the geopolitical cycle and provides a revenue floor for financial infrastructure firms.

Continuing Themes

Iran conflict: 0-for-8 on diplomatic signals. Ceasefire near expiration. Trump says extension “highly unlikely.” US boarding operations continuing. Oil above $95. IEA 2-year recovery timeline. No framework agreement. All structural energy/defense/fertilizer/insurance positions maintained.

Credit cascade: HYG OI P/C at 4.94 (7th consecutive increase from 4.89). Private credit CDS live. March 31 NAV marks entering pipeline. Peak catalyst density in next 2-3 weeks. BX AVOID, OWL AVOID, ARES/OWL pair MAX.

Fed policy: Unanimous hold at 3.64%. Warsh inflation-first. Tillis blocking confirmation. Rate cut 3-5%, hike 35-45%.

AI infrastructure: No material new data today. Earnings season testing the cycle. GE Aerospace commercial engine strength validates power demand thesis for GEV.

What to Watch

Beneath the surface of today’s equity vol normalization, the options market is flashing divergent signals that demand attention. HYG’s put/call open interest ratio has now risen for seven consecutive sessions to 4.94 with an extreme 20.1% put skew at the 1-week tenor — the strongest sustained credit hedging signal of the entire conflict. Meanwhile, SPY near-term IV collapsed back to 13.7%, completing the 4th full vol normalization cycle — and all prior three reversed. IWM remains stubbornly in backwardation at 23.2% with a 1.79 put/call ratio, confirming that institutions are hedging economic damage in small caps even as they trade large-cap momentum. The window for cheap large-cap protection may be short, and the credit-equity divergence that has defined this crisis widened further today. Full options positioning analysis, portfolio playbook, and risk scenario framework below for subscribers.

This publication is for informational and educational purposes only and does not constitute financial, investment, or trading advice. The analysis, opinions, and commentary presented here should not be interpreted as a recommendation to buy, sell, or hold any security. Always conduct your own research and consult a qualified financial advisor before making investment decisions. Past performance does not guarantee future results.