AI's Memory Layer Cracks as Higher-for-Longer Regime Collides With the Chip Trade

Apollo gates its flagship retail credit fund — the deepest liability-side signal yet — while a $17B federal nuclear program treats the power layer as quasi-strategic.

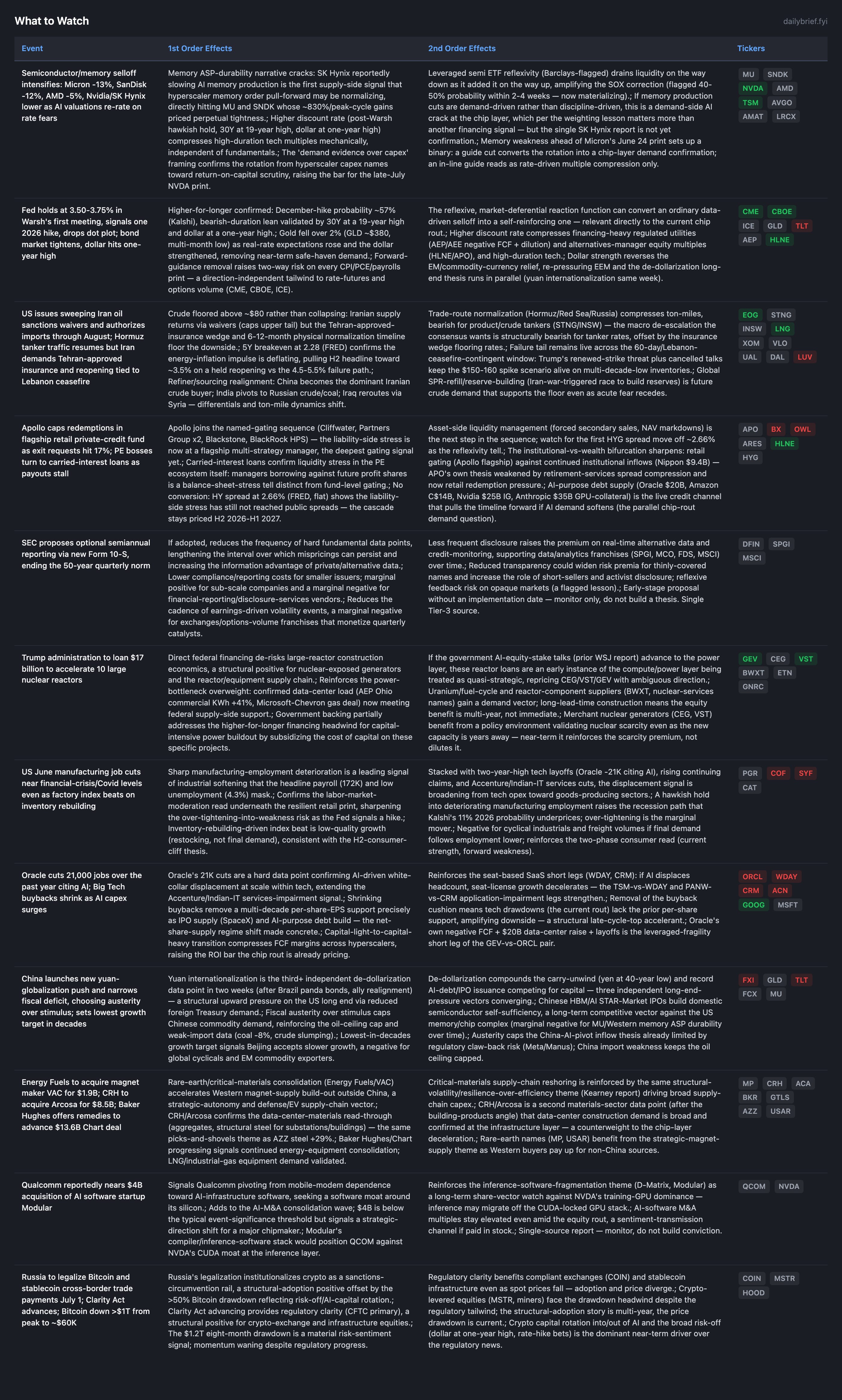

The two month-long binaries resolved last week, and this batch is the consequence playing out across markets, with one genuinely new development: the AI/semiconductor trade is correcting hard, and the proximate cause is the collision of the higher-discount-rate regime (Warsh hawkish hold, 30Y at a 19-year high, dollar at a one-year high) with the chip layer’s first supply-side memory signal. Micron fell ~13%, SanDisk ~12%, and the Nasdaq is down ~5% in June as Wall Street shifted from rewarding AI capex to demanding evidence of returns. This is the semiconductor correction the world model flagged at 40-50% probability within 2-4 weeks, now materializing on schedule. The question that matters is whether SK Hynix slowing AI memory production is rate-driven multiple compression (the dominant read) or the first demand-side crack at the chip layer. The June 24 Micron print is the near-term arbiter; the late-July NVDA print is the decisive one.

Two other developments add information. Apollo capped redemptions in its flagship retail private-credit fund at 17% requests, the deepest gating signal yet and the first at a flagship multi-strategy manager, with PE bosses borrowing against carry confirming ecosystem liquidity stress; HY spreads at 2.66% (FRED) still show no conversion, so the cascade stays priced H2 2026-H1 2027 with Fed stress tests June 24 the next discrete input. And the $17B federal nuclear-reactor loan program is the clearest sign yet that the compute/power layer is being treated as quasi-strategic, reinforcing the power-bottleneck overweight against the chip-layer deceleration. Underneath, the de-dollarization cluster added a fourth data point (yuan internationalization) and US June manufacturing job cuts hit near-crisis levels, sharpening the over-tightening-into-weakness risk.

The Semiconductor Correction Arrives — Memory Leads, and the Demand Question Is Open

The chip rout is the new information. Micron -13%, SanDisk -12%, AMD -5%, with Nvidia and SK Hynix lower, dragging the Nasdaq down ~2% for a second day and ~5% on the month (CNBC, FT, MarketWatch, IBD, Yahoo — multi-source Tier 1-2). Two forces are operating simultaneously, and separating them is the analytical task.

The first is mechanical and dominant: the post-Warsh higher discount rate (30Y at a 19-year high, dollar at a one-year high, December-hike probability ~57% on Kalshi) compresses high-duration tech multiples regardless of fundamentals, and the reflexive market-deferential reaction function can turn an ordinary data-driven selloff self-reinforcing — exactly the second-order risk flagged after the FOMC. The shrinking-buyback backdrop (Oracle, Big Tech capex consuming cash) removes the per-share support that cushioned prior tech drawdowns, so this correction has less of a floor than 2023-2024 episodes.

The second force is the one to weight carefully: SK Hynix is reportedly slowing AI memory production. Per the standing lesson to weight demand-side AI signals above financing-side, if this is a demand-driven cut rather than supply discipline, it is the first chip-layer demand crack, which would matter more than another financing signal. But it is a single report, and the cleaner read is that memory ran ~830% over twelve months on a perpetual-tightness narrative that priced no normalization — a commodity-pricing event mean-reverting, not necessarily a demand collapse. The all-three-supplier HBM4 qualification already capped the monopoly narrative. The June 24 Micron print resolves the near-term binary: a guide cut converts the rotation into chip-layer demand confirmation; an in-line guide reads as rate-driven multiple compression. I am holding MU two-sided (world model HOLD 5.3/10) into that print rather than chasing the selloff, and holding NVDA’s BUY (7.1/10, ~16.5x next-year, $96.7B FCF) on its 3+ data-point thesis rather than flipping it on a single rotation day — the late-July print is its arbiter.

The honest counterweight remains infrastructure-layer breadth: the $17B nuclear program, CRH/Arcosa data-center materials, confirmed AEP load. The chip layer flashed; the power and materials layers did not.

Apollo Gates Its Flagship Retail Credit Fund — The Deepest Gating Signal Yet

Apollo capped withdrawals from its main retail private-credit fund after redemption requests hit 17%, meeting less than a third of demand (FT/CNBC, corroborated). This extends the named-gating sequence (Cliffwater, Partners Group x2, Blackstone, BlackRock HPS) to a flagship multi-strategy manager, the deepest liability-side signal in the cascade so far. Separately, FT reports PE executives borrowing against future carry as distributions stall — a balance-sheet-stress tell distinct from fund-level gating, confirming liquidity stress in the ecosystem itself.

The sequence still has not converted: HY spread at 2.66% (FRED, flat), no public-spread widening, the cascade priced H2 2026-H1 2027. The mechanism to watch is the next step — asset-side liquidity management (forced secondary sales, NAV markdowns) — and the first HYG spread move off 2.66% as the reflexivity tell. HYG OI P/C at 3.75 with a contango term structure continues to price H2 stress against near-term calm. The institutional-vs-wealth bifurcation sharpens: retail gating at Apollo’s flagship against continued institutional inflows (Nippon $9.4B). This weakens APO’s own thesis (now HOLD 6.0/10, retirement-services spread compression plus retail redemption pressure) but keeps APO/ARES preferred over the redemption-exposed BX/OWL. HLNE’s recurring committed-capital fee base (75%+) is structurally insulated from exactly this evergreen-redemption risk, so the gating wave validates the mispriced-recurring-fee long (BUY 6.95/10). Fed stress-test results June 24 are the near-term discrete bank-credit input.

The $17B Federal Nuclear Program — The Power Layer Goes Quasi-Strategic

The Trump administration will loan $17B to accelerate 10 large reactors across five two-reactor projects (CNBC, Tier 2). Federal financing de-risks large-reactor construction economics and partially offsets the higher-for-longer financing headwind on capital-intensive power buildout by subsidizing the cost of capital on these projects. This reinforces the power-bottleneck overweight (GEV, CEG, VST) against the chip-layer deceleration: confirmed data-center load now meeting supply-side federal support. It is also an early instance of the compute/power layer being treated as quasi-strategic, consistent with the prior WSJ government-AI-equity-stake report — if that advances to the power layer, it reprices CEG/VST/GEV with ambiguous direction. The new capacity is years out, so near-term it validates the nuclear-scarcity premium (reinforcing the CEG-vs-FSLR and GEV-vs-ORCL pairs) rather than diluting it; the equity benefit to the reactor supply chain (BWXT) is multi-year.

What to Watch

Developing Themes

Iran/Oil: Floored-Oil Regime Confirmed, Failure Tail Now Lebanon-Contingent

The transit-fee/floored-oil regime is confirmed as the operative baseline. The US issued sweeping sanctions waivers and authorized Iranian oil imports through August (caps the upper tail) while Iran tied full Hormuz reopening to the Lebanon ceasefire holding and demanded Tehran-approved transit insurance (floors the downside); oil settled down >3% but Brent held above ~$80. Analysts estimate 6-12 months to fully restore Hormuz flows, confirming the weeks-to-months normalization timeline. The 5Y breakeven at 2.28 (FRED) confirms the deflating energy impulse pulling H2 headline toward ~3.5%. The failure tail is now explicitly Lebanon-ceasefire-contingent plus Trump’s renewed-strike threat — Oil rebounded 2% intraday on the threat, showing the tail is live. Route realignment is concrete: China the dominant Iranian buyer, India to Russian crude/coal, Iraq rerouting via Syria. STNG/INSW stay two-sided for the structural ton-mile-vs-insurance-wedge reason. Airlines bank the fuel relief (Reuters) rather than passing it through, supporting UAL/DAL margins; LUV the weak leg.

Net-Share-Supply and AI-Capital-Intensity: Oracle’s 21K Layoffs Make It Concrete

Oracle’s 21,000 AI-attributed layoffs and shrinking Big Tech buybacks (Bloomberg) make the capital-light-to-capital-heavy transition concrete. The displacement signal now spans services (Accenture/Indian IT), enterprise software (Oracle), and manufacturing (June factory cuts near crisis levels) — a multi-source labor-displacement pattern, not a single sector. This strengthens the seat-based SaaS short legs (WDAY, CRM) since AI-displaced headcount decelerates seat-license growth, and confirms ORCL as the leveraged-fragility short leg of GEV-vs-ORCL (negative FCF + $20B raise + layoffs). The shrinking buyback removes the per-share cushion underneath the current rout.

De-Dollarization: Fourth Data Point in Two Weeks

China’s yuan-internationalization push plus fiscal austerity (deficit narrowed first time in two years, lowest-decades 4.5-5% growth target) adds a fourth independent de-dollarization data point. This is a structural upward pressure on the US long end (reduced foreign Treasury demand) compounding the carry-unwind (yen at 40-year low) and record AI-debt/IPO issuance — three long-end-pressure vectors converging, reinforcing bearish duration and the structural gold bid despite gold’s near-term rate/dollar-driven pullback to ~$380. Austerity also caps Chinese commodity demand and the oil ceiling.

Continuing Themes

Private credit: No conversion (HY 2.66%, FRED); Apollo gating deepens the liability-side signal; June 24 stress tests the discrete input. Hold APO/ARES over BX/OWL; HLNE the mispriced-recurring-fee long.

Consumer: Two-phase read intact. May retail +0.9% (FRED +6.9% YoY) and existing home sales +130K are current-condition strength; mortgage rates ~6.5% keeping housing subdued through 2027 (Reuters poll), Dave & Buster’s EBITDA miss, and the manufacturing job cuts are forward-cliff tells. PGR over COF, extending to SYF/RDN. Consumer Discretionary BUY-prohibited.

Europe: Deutsche Bank’s US-over-European credit preference and Starmer’s resignation (UK political/fiscal risk) reinforce the bearish lean; VGK flat-to-relief I continue to read as premature given ECB-hike-into-recession.

Defense/power/healthcare-M&A overweights intact: the nuclear program reinforces power; multi-front conflict sustains defense; Eli Lilly/Centessa UK clearance continues the patent-cliff bid (supports LLY).

Crypto: Bitcoin ~$60K, down >$1.2T from peak on risk-off/AI rotation; Russia legalization and Clarity Act structural positives against waning momentum. No portfolio-relevant change.

The cross-market options structure flipped back into broad backwardation this batch, and the durable signals tell a sharper story than the headline tape: QQQ’s -3.2% 12-month skew sitting on a 33.2% near-term front end, IWM’s 2.36 put OI and steepest -3.4% skew on the small-cap cliff, HYG’s contango (4.5% near vs 7.4% far) with a 3.75 OI P/C and the deepest -5.9% skew in the macro set — the named-gating-before-spread-widening pattern intact even as Apollo gates. The premium section maps how to hold high-conviction infrastructure through the chip correction without resolving the demand question prematurely, where the EEM front-end re-stress (53.1% near, +17.5% put skew) reflects the dollar/Iran two-sided repricing, and which of the seven risk scenarios — from a confirmed chip-layer demand crack at the June 24 Micron print to a stress-test-triggered Apollo conversion — carry the highest leverage. Full options positioning analysis, portfolio playbook, and risk scenario framework below for subscribers.

This publication is for informational and educational purposes only and does not constitute financial, investment, or trading advice. The analysis, opinions, and commentary presented here should not be interpreted as a recommendation to buy, sell, or hold any security. Always conduct your own research and consult a qualified financial advisor before making investment decisions. Past performance does not guarantee future results.